Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThrogmorton manager explains process for emerging companies fund

Investors will be familiar with the phrase ‘past performance cannot be relied upon as a guide to future performance’. These words, or something very similar, have become the investment industry’s ubiquitous risk warning. They are designed to make clear to investors that no matter how good an investment has been in the past, there are no guarantees that it will continue to perform in the future.

This makes identifying stocks capable of generating attractive returns for years to come all the more important, especially for newer investors with limited returns already banked.

BlackRock fund manager Dan Whitestone does this by seeking out ‘emerging companies’, stocks that are at an early stage in their life cycle and/or those expected to enjoy significant growth into the future.

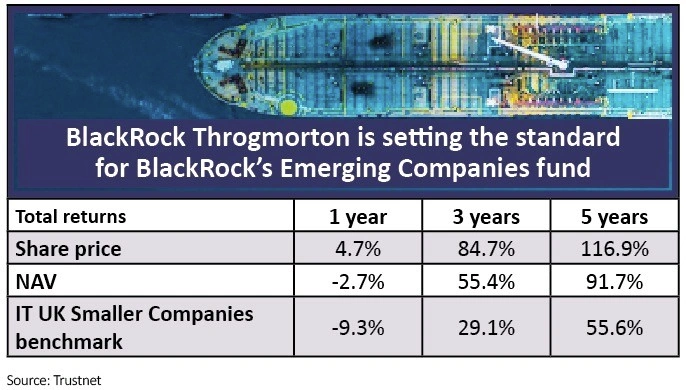

BENCHMARKING THE MANAGER

Whitestone is best known among retail investors as the manager of BlackRock Throgmorton Trust (THRG), the £420m smaller company investment trust that has returned 116.9% over the past five years, more than twice its benchmark.

He now also calls the shots for the £312m BlackRock UK Emerging Companies Absolute Returns Fund (BDRMQN4), which operates a very similar investment ethos.

It’s a style that may also chime with investors of the popular Scottish Mortgage Trust (SMT).

The ‘emerging companies’ strategy effectively concentrates on unearthing companies with good management, robust finances with strong market positions that are exposed to industry change and which are capable of capitalising on long-term secular trends that triumph over macro or economic cycles.

‘Forget growth versus value, forget quantitative easing or tightening, deflation, forget it all,’ Whitestone says. ‘Industry change is happening like it or not, and faster than ever.’

Whitestone looks for high quality differentiated companies. These are typically capital-light companies whose products are not purely competing on price but provide real solutions to customers’ problems in industries with structural growth drivers. These companies will also be debt-light and cash generative, so surplus funds can be redeployed into future growth.

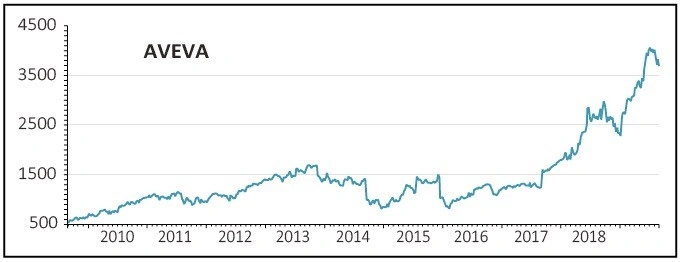

Engineering software provider Aveva (AVV) is a good example and one that Whitestone clearly admires. ‘Everyone agrees it is a good a company,’ he says. Aveva’s share price has rallied 53% so far in 2019 giving the company an enterprise value worth £5.78bn and a spot in the FTSE 100.

The March 2021 fiscal year price-to-earnings multiple stands at 47.6 which is too eye-watering for many. Yet AVEVA has never been cheap on traditional metrics.

COST VERSUS OPPORTUNITY

‘The market struggles to price big, structural growth businesses,’ argues Whitestone.

Aveva is bringing disruptive technology to an engineering industry that has been very slow to embrace digitisation.

Digital twins, for example, allow industry engineers to design massive and expansive projects – such as buildings, power plants, oil rigs, planes and ships – in virtual form, where they can be completely tested for faults and weaknesses or improvements identified before a brick, steel girder or cement foundation has been laid. This is hugely cost effective and embeds design creativity.

But Aveva is also helping itself, looking for internal process and operational improvements that can enhance profit margins. Building up its recurring revenue streams by offering software access as a service (monthly subscriptions) is bolstering earnings reliability and quality.

Whitestone’s BlackRock UK Emerging Companies Absolute Returns Fund has 1.8% of assets in Aveva, a stake worth more than £5.6m at today’s prices, but there are other stocks where the fund has an even greater stake.

The fund’s London Stock Exchange (LSE) stake, its largest, is worth almost £9m while Rentokil Initial (RTO), SSP (SSPG) and temporary power equipment supplier Ashtead (AHT) are other holdings all larger than Aveva, as is its £8.4m holding in US software giant Microsoft.

The BlackRock UK Emerging Companies Absolute Returns Fund has scope to invest up to 30% of asset into companies outside the UK. But this is an absolute returns fund which means it will use financial instruments to go short where the team see an opportunity.

While Whitestone refuses to reveal the fund’s open short positions one could suggest that accountancy, payroll and enterprise software firm Sage (SGE) has the hallmarks of a potential candidate because of the way cloud computing is shaking up its bookkeeping industry.

Sage has spent years trying to adapt to the cloud without damaging its traditional and profitable licence model in the face of intensifying competition from long-standing rivals like Quickbooks-owner Intuit. It has also faced a mini deluge of ‘born in the cloud’ start-ups like Kashflow and Xero, the latter of which is in the BlackRock fund.

BlackRock itself rates the fund as a five out of seven higher risk ranking, which suggests it is not for widows and orphans and would only suit those with a fairly long-term investment horizon.

But like most absolute return funds, investor costs can be chunky. Ongoing charges stand at 1.41% but there is also a hefty-looking 20% performance fee to factor in.

The BlackRock UK Emerging Companies Absolute Returns Fund only launched in October 2018 so has little performance track record to judge it by, but given the style similarities, it makes the BlackRock Throgmorton’s returns record a useful guide.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.