Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTed Baker shares are just too cheap to ignore

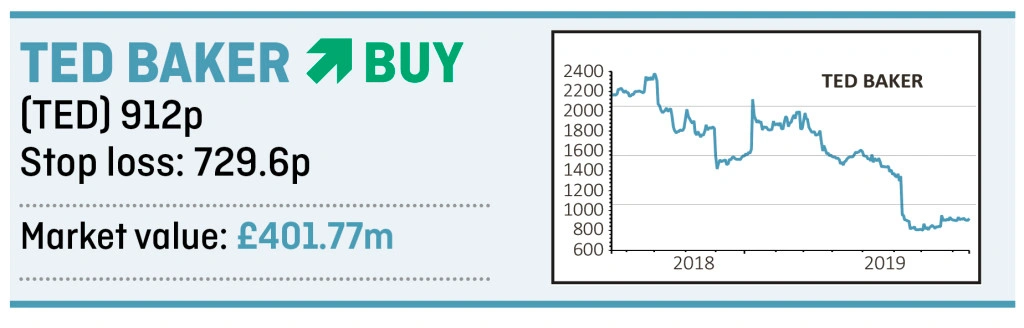

We think you should buy lately-unloved global lifestyle brand Ted Baker (TED) at 912p.

This isn’t a trade for the faint of heart as the current valuation is discounting that already-downgraded profit estimates may yet be missed, but Shares still has faith in the strength of the Ted Baker brand and its global growth potential.

WHY TED’S DOWNTRODDEN

Shares in Ted Baker have tumbled 62% from their one-year peak of £23.78 on a flurry of earnings downgrades.

Recent trading disappointments reflect a toxic combination of consumer uncertainty, heightened promotional activity across global markets, bad weather in North America, adverse currency moves and womenswear product issues.

Sentiment towards the stock was also hit by the resignation (4 Mar) of founder and chief executive officer (CEO) Ray Kelvin following a probe into ‘hugging’ claims (strenuously denied by Kelvin) made by some employees.

TED LOOKS TEMPTING

Ted Baker has issued two profit warnings since February and because such setbacks tend to come in threes, recovery investors should brace themselves for further volatility as the retailer could be forced to cough up another earnings alert.

Yet the quintessentially British clothing label remains an outstanding brand and Ted Baker is still a high-quality, well-invested business with a growing e-commerce operation and considerable scope for growth in overseas markets.

Moreover, given the current bombed-out valuation, the shirts, suits and fragrances designer appears vulnerable to an approach which ‘could come from a number of different sources’ according to Liberum Capital.

Ray Kelvin was recently rumoured to be considering a bid with private equity backing in order to take the retailer off the stock market. Any takeover bid would surely need to be pitched at a substantial premium to current levels to win over shareholders, notwithstanding Kelvin’s 35% stake.

NEXT LEVEL OPPORTUNITY

And in an exciting development, Ted Baker has signed (16 Aug) a new product licence agreement with Next (NXT) — replacing an existing deal with Debenhams – in order to accelerate the expansion of its childrenswear collections.

Partnering with Next brings Ted Baker access to the clothing giant’s global sourcing and distribution capabilities. Over time, this deal should drive incremental growth for Ted Baker’s high margin licensing division, which chips in over 30% of group earnings before interest and tax (EBIT).

For the year to January 2020, Liberum, whose £12.80 price target implies 40% potential upside, forecasts an adjusted pre-tax profit drop to £50.3m (2019: £63m) ahead of recovery to £53.2m and £56.3m for 2021 and 2022 respectively.

Based on this year’s earnings per share forecast of 88.1p (2019: 114.1p) and 45.3p (2019: Ted Baker looks too cheap on a budget-looking prospective earnings multiple of 10.4 with a yield approaching 5%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.