Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow to prepare for more rate cuts and stimulus

The return of volatility to financial markets, as safe haven assets soar and risk assets wobble, is a timely reminder that it is far too early for central banks to declare victory in their attempts to boost global growth, stoke inflation and stave off deflation.

Investors’ dash to buy (Western) Government bonds, the yen, gold and the dollar and fight shy of equities reflects gathering concerns over growth and debt.

In the face of such worries, America’s Trump administration is already clamouring for more interest rate cuts and talking of a new tax cuts for good measure (in what some could see as an admission that the December 2017 tax package provided a short-term sugar rush but no more than that).

The European Central Bank is still taking about lower interest rates and a return to quantitative easing and the Bank of England’s plans to hike borrowing costs are seemingly on hold.

Such policy ponderings are giving share prices some support but ultimately, they show that neither governments nor central banks are sure of what the ultimate outcome of a decade’s worth of unorthodox monetary policy (and in some cases fiscal stimulus) could be.

Any one of inflation, stagflation or deflation could yet be the outcome.

Four-pot plan

This leaves investors in a quandary. The yield curve could be right, and a defensive posture may be required, leaning on perceived haven assets such as bonds, gold or even cash.

The yield curve could be wrong. Growth may continue, central banks may panic and overdo additional stimulus, leading to inflation, especially if China and America settle their trade tiff (even if that seems unlikely for now). In this case, bonds and cash could be bad places to be and equities a better option, if history is any guide.

We could get the worst of both worlds, with limited growth and rising inflation, taking us back to the 1970s when gold was the best performing asset and cash, bonds and stocks all struggled, especially in real terms.

Each possible outcome requires a different tactical portfolio response. As such it may be worth researching how to a portfolio designed to weather a range of economic and financial market outcomes, to protect wealth as well as try to create it.

A few years ago, market strategist Dylan Grice devised a portfolio with the aim of doing just that, when he was at French investment bank Société Générale. This column has analysed his ideas before and it may now be appropriate to do so again.

Inspired by the apparently indestructible nature of the cockroach, Grice looked at how to build an investment portfolio that would be just as durable as the doughty insect. He argued a pot split into four even parts between cash, high-quality bonds, income-generating equities and gold would have done the trick.

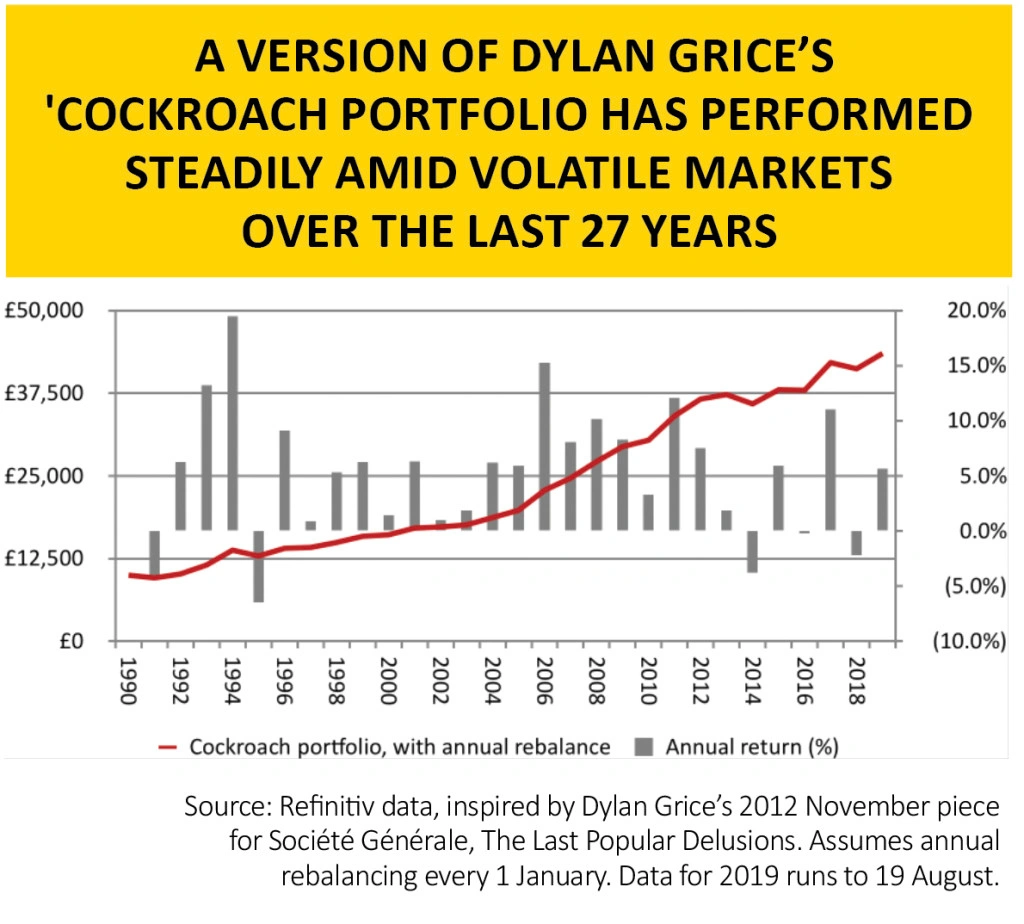

This column has revisited this concept and tried to recreate the cockroach portfolio, starting with a £10,000 pot. To keep it simple, the equity income portion is represented by the Invesco Perpetual High Income (3303148) fund, which has a good pedigree and a long-enough history. The 10-year Gilt is used for bonds, the spot gold price has been used in sterling terms, while the fourth element is covered by the Royal London Cash Plus fund. The portfolio is then rebalanced each year on 1 January to return to the four-way even split.

The results over the past year are perfectly respectable: a 4.6% return (before any dealing costs, levies or taxes) with minimal volatility. If investing is all about going to bed and being able to sleep soundly then this may be one way to achieve a little peace of mind.

Test of time

However, a year is hardly an adequate test for any portfolio. The next test is therefore to go back to 1991, again splitting a hypothetical £10,000 pot equally across the four portfolio constituents. This time the cash element is represented by the Bank of England base rate and the portfolio is rebalanced each year on 1 January.

The result, again before dealing costs, fees or taxes, is a pot worth £43,504 for a 5.2% compound annual return, a figure which nicely beats inflation. Intriguingly the rebalancing seems to help. Without it, the portfolio comes to £41,168.

Better still, perhaps, from the perspective of investors is the limited volatility of returns. The rebalanced portfolio shows just five down years although three have come since 2014, which offers a reminder that the past is no guarantee for the future. A low-growth, low-interest-rate, QE-riddled world is even testing the powers of the cockroach.

The ‘cockroach’ strategy will not suit everyone’s goals, target returns, time horizons and risk appetites.

Yet the emotionless discipline of the rebalanced four-pot approach may give some investors pause for thought, especially as the historic returns have shown low volatility and we may be about to witness a fresh round of unorthodox central bank action, even after a decade of such policies are yet to prove they can have the desired effect.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.