Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineKnow your fund: what’s inside Scottish Mortgage?

It has nothing to do with home loans and invests across the globe, Scottish Mortgage Investment Trust (SMT) is not one of those ‘does what it says on the tin’ funds.

Yet the FTSE 100 trust is widely thought of as manager Baillie Gifford’s flagship and it has grown to become one of the most popular investment trusts with do-it-yourself investors up and down the UK.

First, let’s put a popular misconception to bed. Scottish Mortgage is NOT a FANG fund or technology trust, FANG being an acronym for Facebook, Amazon, Netflix and Google-parent Alphabet. The underlying ethos of the trust is to identify and invest in the best growth companies the world has to offer, and hold on to them, at five years and often far longer.

We are talking about companies capable of out-sized returns over the long-term through industry disruption or socio-economic and demographic development.

The speed of widespread technological change and China’s emergence as a world economic superpower are two of its core themes, while transforming industries such as online shopping, healthcare and financial services are represented in the portfolio.

Amazon is a great example. Scottish Mortgage first bought into the online sales colossus in 2005 at around the $30 and $40 level. fourteen years later Amazon trades at $1,776, a staggering 50-fold or so return. Yet joint managers James Anderson and Tom Slater are as excited about Amazon’s prospects and returns potential as ever, particularly around areas like new market opportunities like healthcare, overseas expansion (India) and cloud computing (Amazon Web Serives).

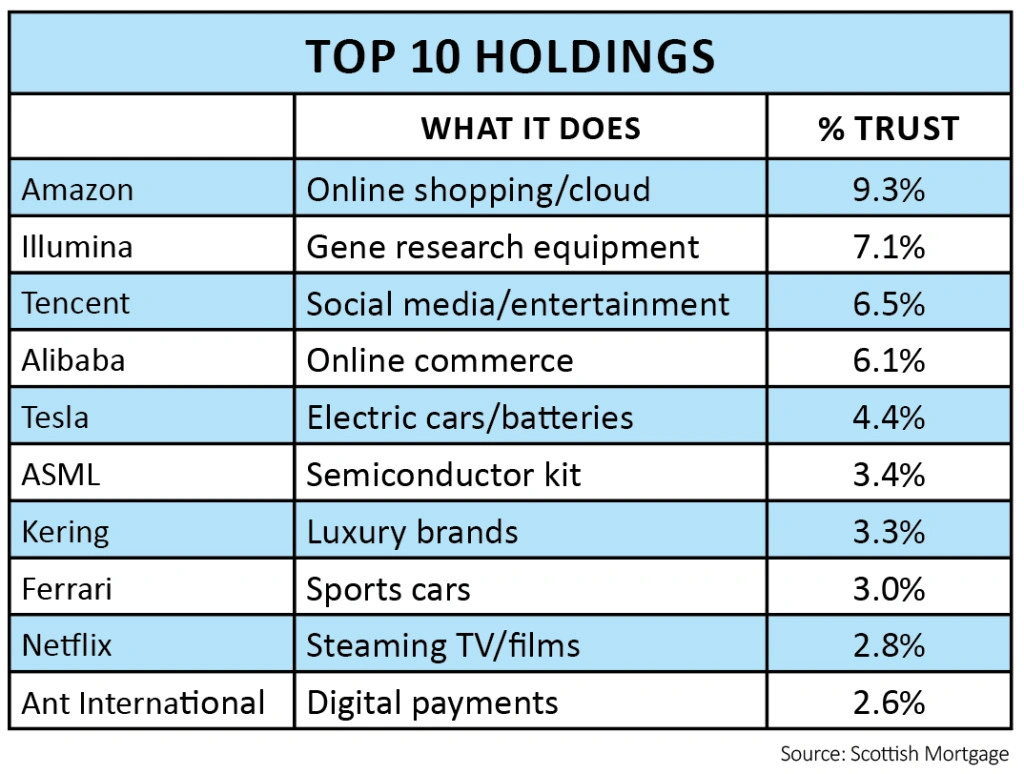

Amazon is now Scottish Mortgage’s largest single holding, worth 9.3% of its £8.85bn assets.

It is the potential for massive returns such as this that make Scottish Mortgage put less emphasis on purchase price valuation, more on the capacity to compound super-normal growth over years.

WHAT ARE THE OTHER BIG STAKES

Most readers will be familiar with names like streaming TV service Netflix, Google-parent Alphabet and sports car maker Ferrari, all in the top 15 holdings as of 31 March. But there are plenty of exciting growth stories that you probably know less about.

For example, Scottish Mortgage is a heavy backer of China’s Amazon lookalike called Alibaba (6.1%), and Tencent (6.5%), the Chinese social media and entertainment platform.

It also owns hefty stakes in Illumina in the US (7.1%), which is building advanced equipment to unlock the power of genetic science for all of us, and ASML, the Dutch semiconductor equipment manufacturer used in making the most complex microchips.

There are marmite stocks too. Not all investors would want to own Facebook, for example, almost continually caught up in privacy controversies. Elon Musk’s stubbornly loss-making electric cars firm Tesla has at least as many foes and fans, while ride-sharing app Lyft is also on the trust’s books.

It is also worth noting that Scottish Mortgage is more invested in privately-owned companies than ever regardless of the recent Neil Woodford liquidity issues.

About £1.4bn of the trust’s assets are in 37 unlisted companies led by payments business Ant Financial, spun-out of Alibaba, and Elon Musk’s SpaceX, which runs many Nasa missions and developed the first re-useable rocket.

Interestingly, Scottish Mortgage’s own analysis earlier this year pointed to a 419% returned on unlisted investments over the previous eight years, bettering publicly listed stocks. Big hits that have since gone public include Alibaba, music streaming business Spotify that floated last year at $30bn, and Lyft.

The trust remains convinced of its ‘venture capital’ talents and that scope for up to 25% of the trust to be unlisted gives it the freedom to tap early some of the most exciting growth companies at an early stage.

HIGH GROWTH, LOW COST STRATEGY

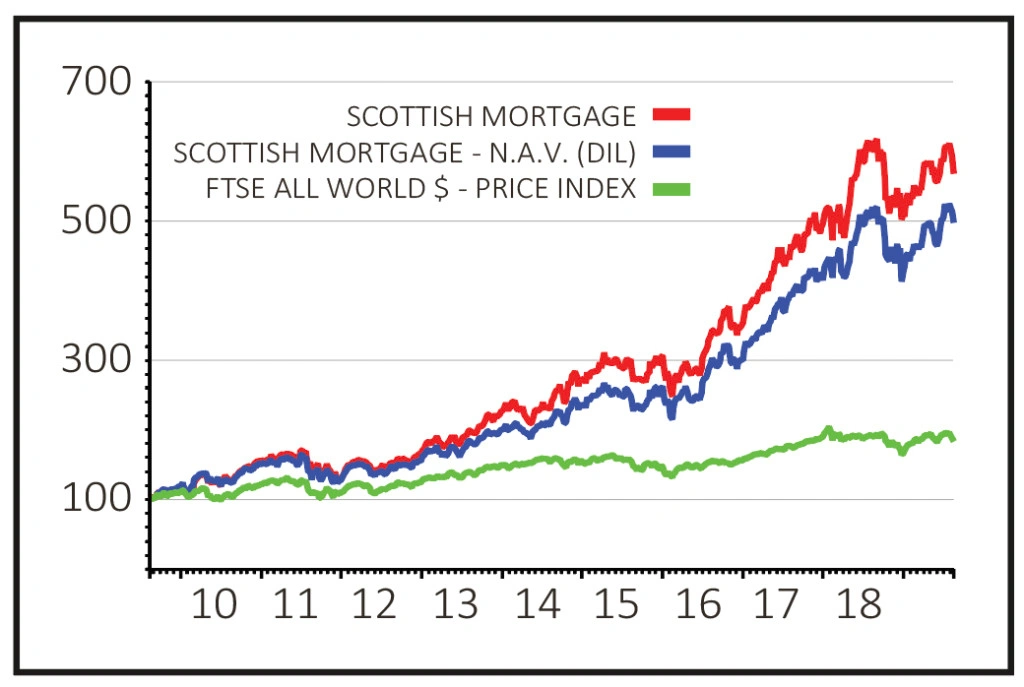

The bottom line is, investors will judge the success of Scottish Mortgage by how the share price performs, and that is surely the secret to the trust’s immense popularity. Last year to 31 March 2019 Scottish Mortgage made an underlying 14.6% total return on net assets, underpinning a 16.5% total return for shareholders, beating the 10.7% gain from the FTSE All-World index, its benchmark.

That may look like a pretty decent performance but it is irrelevant, says the trust’s top brass. ‘I urge readers to pay little heed to them [the annual performance figures] such is strength of its pledge to the long-term. Scottish Mortgage wants to be judged on five-year rolling performance, its true measure.

It is knock-out. To 31 July 2019 net assets have gained 164.6% and the share price 176.8%, on a total returns basis. That’s closing in on twice as good as its benchmark’s 93.8%. Illustratively, the performance gap widens much further over 10 years, with NAV and share price up 518.9% and 629.2% versus 245.1%.

Only Lindsell Train (LTI) has done better of all the trusts listed on the Association of Investment Companies’ Global sector.

Scottish Mortgage wants its investors to share in its thinking and observations and provides a plenty of data, insight and information on its Baillie Gifford-backed website, which Shares recommends following even if you don’t buy the shares.

Costs are also reasonable, with an ongoing management charge if 0.37%. ‘This gives this strategy an exceptional cost advantage relative to peers,’ according to Morningstar analysis versus global large cap growth equity averages.

SHARES SAYS

A clear long-term growth strategy aimed at uncovering super-normal returns, the style lends itself to short-term volatility. But this really is a buy and forget type investment, one that has proven itself tie and again. A long-run favourite of ours and it remains so.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.