Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineGreene King’s £4.6bn bid is ‘too cheap’ say analysts

Several analysts suggest the 850p per share takeover offer for pubs group Greene King (GNK) is too low. Investors already holding the stock should sit tight and await a higher offer, either from the current suitor or a counterbid.

Hong Kong-based property developer and investor CK Asset is offering £4.6bn for the business including its large debt pile. The offer is pitched at a 25% premium to net asset value and 9.5 times trailing EBITDA (earnings before interest, tax, depreciation and amortisation).

EI Group (EIG) recently received a takeover bid from Stonegate for the equivalent of 11.4 times trailing EBITDA and Punch Taverns was acquired in 2017 by Heineken and Patron Capital on a 10-times multiple. Canaccord Genuity analyst Nigel Parson says Greene King’s offer really needs to be on a similar level to these other pub companies.

Greg Johnson, analyst at stockbroker Shore Capital, says 950p would be a more attractive takeover price for Greene King in order to secure shareholder approval.

Parson implies a counterbid could be possible, potentially from an overseas brewer wishing to enter the UK market. He says the most obvious bidder is Molson Coors, whose brands include Carling, Cobra and Doom Bar.

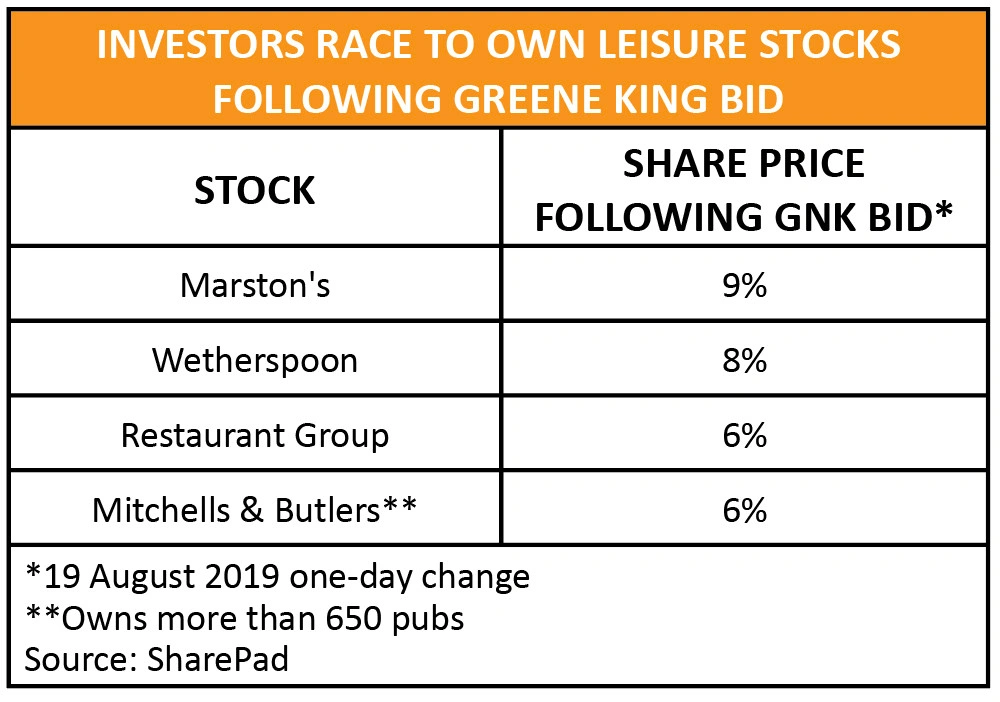

Investors flocked to other UK-listed pub companies following the Greene King news, speculating they too could be takeover targets. Marston’s (MARS) – which is a running Shares Great Idea – was the biggest riser, jumping 9%.

The Marston’s pub estate is valued at 95p per share, equal to 10 times EBITDA. Marston’s also has a beer business which Johnson at Shore Capital believes could be worth a further 60p to 80p per share (9 to 12 times EBITDA). Its shares currently trade at 117.1p.

Pub companies are seen as attractive targets for overseas buyers because the current weakness in sterling makes them cheaper for a foreign company to buy and many also benefit from large asset-backing. For example, Greene King says 81% of its estate is either freehold or long leasehold.

In a similar fashion, Premier Inn hotel owner Whitbread (WTB) is seen as a takeover target due to its 60% freehold property exposure. Fuller Smith & Turner (FSTA) earlier this year sold its brewing business to Japan’s Asahi for £250m.

Should a higher offer fail to emerge for Greene King, investors may be interested to note that investment bank UBS doesn’t believe CK Asset will have any trouble paying for the acquisition. It says the suitor has HK$59.5bn (£6.26bn) cash and is expecting HK$23bn (£2.4bn) soon from residential property sales.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.