Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

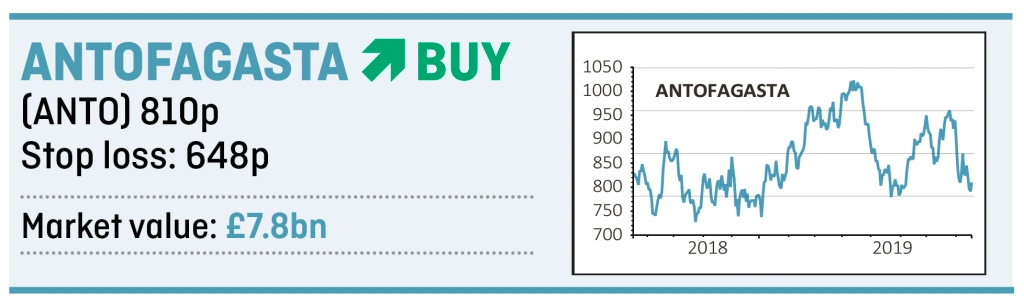

magazineBuy copper giant Antofagasta before sentiment improves

Want to buy a best-in-class company while market sentiment is poor? Now’s your chance with Chilean copper miner Antofagasta (ANTO).

A 20% share price fall since April is partially down to the price of copper recently slipping to levels not seen since the last global recession.

The shares have been dragged down by fellow copper miner KAZ Minerals (KAZ) recently cutting its dividend and saying the short term outlook for copper is weak due to US China trade tensions and a slowdown in the Chinese economy.

But KAZ believes the long term outlook for copper ‘remains robust’, and virtually all analysts covering the sector agree the fundamentals for copper remain strong, with significant long term structural growth forecast for both its demand and price.

Therefore, we think the current dip in Antofagasta’s share price, and its prospective 2.7% dividend yield, means now could be an attractive buying opportunity to gain access to the long term copper market.

Admittedly all mining stocks are higher risk investments as commodity prices can be unpredictable and mining operations volatile. Therefore this is not a stock for the faint-hearted.

Antofagasta is the biggest pure-play copper miner on the London Stock Exchange, and operates in what is seen as a low-risk jurisdiction with all of its mines in Chile.

Considered by analysts at investment bank Jefferies as the lowest risk play on the copper price, the firm has avoided some of the operational issues which have dogged other miners.

Its latest quarterly production report was in line with expectations, and showed an operationally strong business with copper production rising 5.3% to 198,600 tonnes as a result of higher production from all of its mines.

For the first six months of the year, production was up 22.2% because it was able to process more copper at a better grade at most of its operations.

It also managed to reduce its costs, producing copper at $1.62 per pound in the second quarter of this year and $1.66 per pound overall in the first half, 4.7% lower than the first quarter and 13.5% lower than in the first half of last year.

This is down to the productivity programme Antofagasta introduced in 2015, though it’s worth noting the figures were also helped by a weaker Chilean peso.

While the price of copper may not improve significantly by the end of this year, analysts remain bullish on Antofagasta with investment bank BMO saying it looks ‘extremely well placed for the second half of the year’.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.