Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineValue retailer The Works fails to excite as shares flop 30% since IPO

Shares in retailer TheWorks.co.uk (WRKS) have fallen by 30% since it joined the stock market last summer at 160p, caught up in general negative market sentiment towards everything linked to

the high street.

While it hasn’t been the best start to life as a quoted company, there is a feeling that investors haven’t really given it the time of the day and don’t fully understand what it does and how it could grow. This

article gets under the bonnet of the latter two points.

WHAT DOES IT DO?

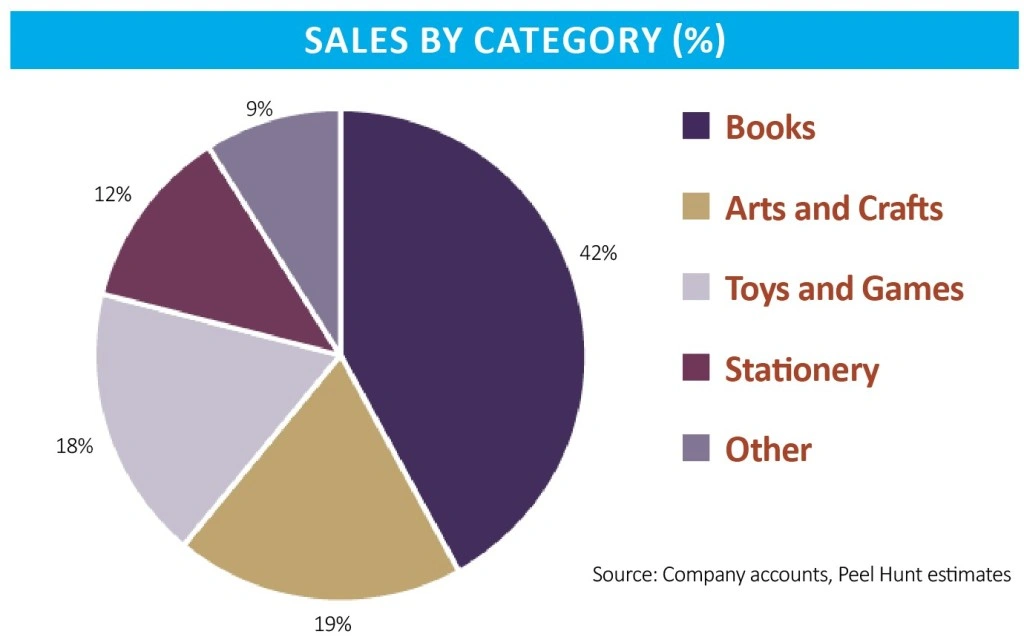

The Works is a multi-channel value retailer of gifts, arts, crafts, toys, books and stationery. This gives its stores a treasure trove feel; hence the strapline in stores is ‘What will you discover?’.

Books is the biggest category, but the company is also winning market share in toys, games and stationery. Management insists The Works is seen as a ‘specialist by the discounters and as a discounter by the specialists’.

Broker Peel Hunt explains: ‘The company plies its trade in four growth areas of the market, which have a total size of about £8bn. Currently, The Works has a minor share in each of the markets, which in many respects is a good thing in that it drifts under the radar of some of the key competitors, and this has allowed it to build a franchise without raising the alarm.’

Going to market with ultra-competitive prices and eye-catching promotions, The Works has a broad customer base, scores a higher value-for-money rating with shoppers than the likes of B&M European Value Retail (BME) or even Amazon and now has over 1.5m active loyalty card users.

WHAT ARE THE GROWTH DRIVERS?

The Works trades from 484 stores and is adding 50 new outlets per year with the ultimate goal of having 1,000 stores. Given the well-documented headwinds blowing through the entire industry, the retail property sector is very much a buyers’ market which means The Works can expand on more favourable terms than periods past.

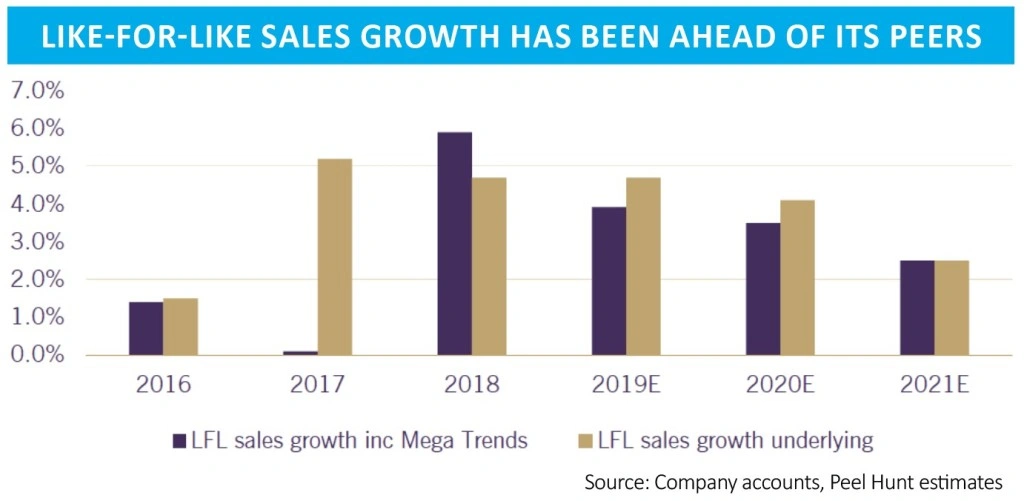

In-store like-for-like sales are in sector-beating rates of growth and are often boosted by the latest craze in the school playground – known in the trade as ‘mega trends’. Recent years have seen a clamour for loom bands, fidget spinners and squishy toys and this is being augmented by online growth, currently speaking for about 10% of turnover.

Admittedly, brand awareness could be better but it is definitely building. ‘The amount of shoppers that are aware of the existence of The Works has increased dramatically in the last six years,’ says Peel Hunt.

‘This, to a degree, is to be expected given how aggressive the store roll-out has been: there are simply more high streets and retail parks that include The Works now.

‘It is also interesting that 80% of the online shoppers that use its website are not customers of the bricks and mortar chain, and we believe that as time goes on and the relevance of the website continues to grow, overall awareness of the brand will continue to grow.’

WHAT ARE THE KEY RISKS?

Significant seasonality is one issue to consider with the retailer currently making all of its profit in the second half of the financial year.

Results for the six months to 28 October 2018 revealed an adjusted pre-tax loss of £4.4m, the same as a year earlier despite revenue up 15% to £91.5m with 3.8% like-for-like sales growth. Rising costs were to blame for failing to narrow pre-tax losses.

Unusually for a purveyor of low ticket items, The Works operates a transactional website, although teething problems with the switch to a new distributor will see online earnings before interest and tax fall in the current financial year.

Competition in the retail sector is ever-fierce and the company locks horns to varying degrees with names ranging from Amazon and B&M to Poundland, Smyths Toys, WH Smith (SMWH), Paperchase and Hobbycraft.

Any renewed sterling weakness would act as a headwind, since The Works sources a significant portion of product in US dollars while operating margins are skinny – Peel Hunt forecasts 3.7% operating return on sales for the current financial year rising to 3.8% for 2020 – and rising wage costs are unhelpful.

Margins could potentially improve over time if sales densities increase and management drives through efficiencies and rent reductions.

HOW MUCH MONEY COULD IT MAKE?

Peel Hunt forecasts a jump in adjusted pre-tax profit to £7.4m 2018: £4.3m) for the year to April 2019, ahead of £9.3m in 2020 and £11.5m in 2021.

The shares trade on a price-to-earnings ratio of 9.9 based on next year’s earnings per share forecast of 11.7p and the current share price of 111p. It is expected to pay 4.8p in dividends next financial year, implying a 4.3% prospective yield.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.