Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy certain types of ETFs are riskier than you think

In 2018, only 6% of flows went to synthetic exchange-traded funds (ETFs) yet approximately £1 in every £5 invested in ETFs is in a synthetic product according to data from Lyxor ETF and Bloomberg.

Physical and synthetic replication are terms used to describe how ETFs manage to track a market.

Physically-backed products trade directly in the underlying stocks in an index to replicate the performance of a market, while synthetic ETFs employ a swap-based method of replication, buying derivatives contracts offered by brokers and investment banks which artificially provide the performance of a market.

In recent years providers have responded to investors’ preference for physical ETFs and investors should have several options for most mainstream indices which are physically-backed.

However, the figures from Lyxor and Bloomberg are a reminder that a sufficient chunk of the money invested in ETFs is still in synthetic products. As such, it is worth understanding which products sit in this category and why.

WHAT DO SYNTHETIC ETFS OFFER EXPOSURE TO?

Using a synthetic ETF may be the only solution for investors seeking exposure to harder-to-access parts of the market, less liquid benchmarks or certain commodities like oil.

Lyxor Northern Europe ETF strategy head Adam Laird says synthetic ETFs can help investors gain access to emerging markets, particularly India where physical replication isn’t an option due to restrictions on foreign ownership of domestic shares.

‘There are a few markets where synthetic really makes sense, though we’d say that these are generally only suitable for professionals who understand the structure,’ comments Laird.

‘In some instances, synthetic investments can be lower cost to run – dealing charges might be lower, tax treatment can be different or they can reduce turnover in a market where trading is costly,’ he explains.

WisdomTree UK Distribution director Pav Sharma adds that many commodities markets can only be accessed synthetically due to difficulties associated with physically buying and storing them.

THE PROS AND CONS OF SYNTHETIC ETFS

A major perceived advantage of synthetic ETFs is that they largely eliminate tracking error – the amount by which an ETF’s returns deviate from its benchmark index – as they are not exposed to the inefficiencies of the physical market.

However, complexity is a big drawback with synthetic ETFs and often there are physical alternatives that may offer the same exposure.

There is also counterparty risk. For example, an investment bank with an ETF swap agreement which gets into trouble could ultimately create a problem.

‘Since a synthetic ETF is usually swap-based and the swap is a credit obligation of a bank, if that bank were to default, it could lead to losses for the investor,’ says Sharma.

Synthetic products are typically covered by some kind of collateral to protect investors against the risk of the counterparty (the broker or bank which issues the contracts) going bust.

HOW MANY ASSETS ARE HELD IN UK-LISTED SYNTHETIC ETFS?

Approximately £51.2bn in assets are held across 248 UK-traded synthetic ETFs according to data from Lyxor.

As we mentioned before, these types of ETFs are more complicated and potentially only worth considering when the investment strategy is not possible via a physical ETF.

But there are plenty of options for any UK investor still comfortable owning synthetic ETFs.

WHICH UK-LISTED SYNTHETIC ETFS ARE THE LARGEST?

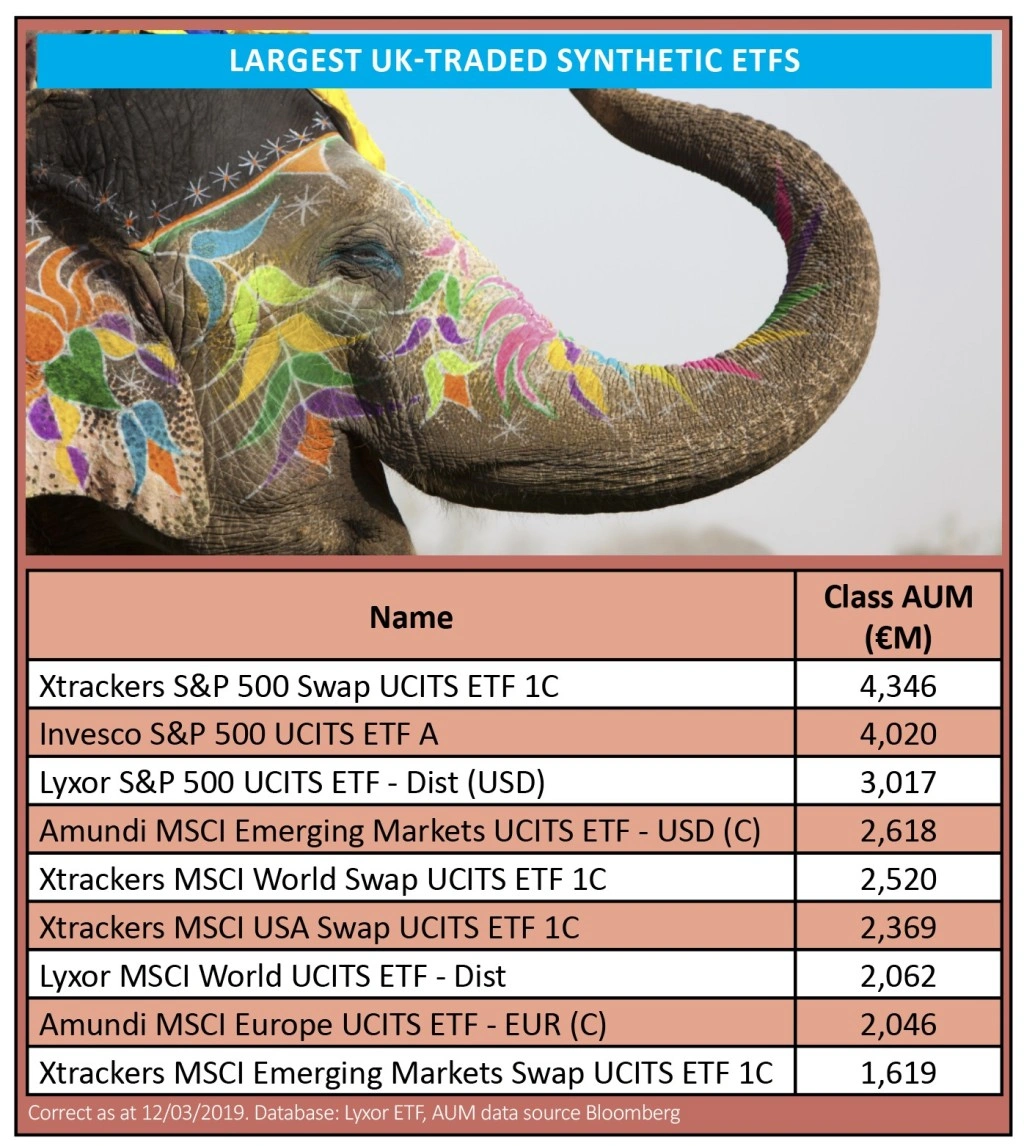

The S&P 500 is the focus for the three biggest UK-traded synthetic ETFs.

Xtrackers S&P 500 Swap UCITS ETF (XSPU) has approximately €4.3bn in assets under management, followed by Invesco S&P 500 UCITS ETF (SPXP) with €4bn and Lyxor S&P 500 UCITS ETF (LSPX) with around €3bn.

Also among the largest synthetic EFTs is Amundi MSCI Emerging Markets UCITS ETF (AU EM), which tracks the performance of the MSCI Emerging Markets Index.

In addition, investors can gain exposure to the US and Eurozone via Xtrackers MSCI World Swap UCITS ETF (XMWD), which reflects the performance of the MSCI Total Return Net World Index.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.