Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineRenishaw takes a step back after Asia problems

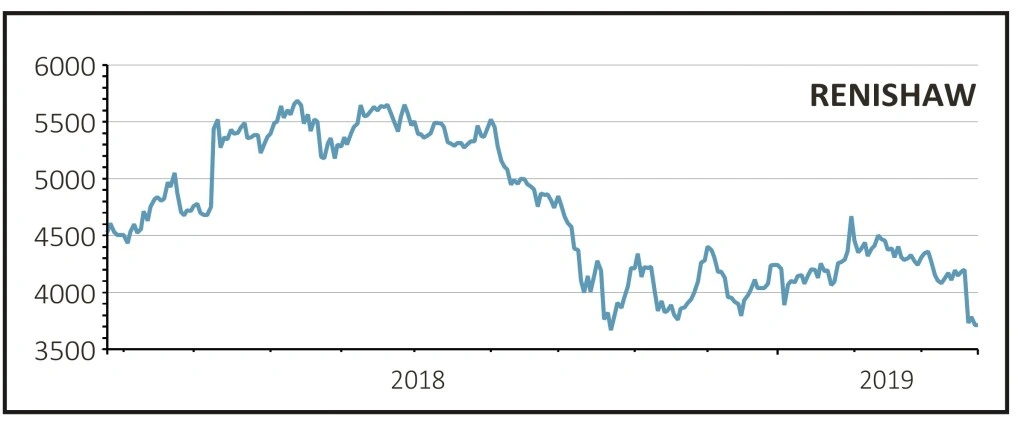

Renishaw (RSW) £37.10

Loss to date: 2.5%

Original entry point: Buy at £38.04, 20 December 2018

A profit warning from precision engineer Renishaw (RSW) has wiped out all our earlier gains, putting the trade a touch below our December entry point.

Asian weakness is to blame amid a slowdown in demand for its encoder products and from large end-user manufacturers of consumer electronic products.

The Far East accounts for 43% of group sales so the profit warning means Renishaw is now a much higher-risk stock to own.

We acknowledge there are headwinds but we hope this is simply a bump in the road for what remains a high quality business. Renishaw has been through such issues in the past and come out fighting and we expect the same again.

It is also worth noting that the business isn’t solely dependent on the consumer electronics sector as it has a growing business serving the healthcare sector including systems for the dental industry.

Chief executive William Ernest Lee invested nearly £38,000 of his own money in buying shares immediately after the profit warning, which sends a vote of confidence to the market in the company’s outlook.

SHARES SAYS: Renishaw’s shares are likely to be volatile until it can prove that issues in Asia aren’t getting any worse.

Its next scheduled announcement is a trading update on 14 May, coinciding with a big event at its headquarters for shareholders, analysts and brokers to better explain its business. We suggest you keep hold of the shares.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.