Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSeven great growth stocks for your ISA

The clock is ticking towards the end of the tax year on 5 April which means investors should take advantage of any unused ISA allowance now. Everyone is allowed to invest up to £20,000 a year across the range of ISAs and you don’t have to pay any tax on capital gains and income on investments held within the ISA.

You should take advantage of any unused allowance to transfer across investments held in a dealing account as currently you would incur tax on capital gains above the £11,700 allowance, and income above the £2,000 annual dividend allowance.

An alternative is to invest any spare cash in the markets via an ISA to make future returns as efficient as possible without losing anything to the taxman.

This article looks at a selection of large and small cap growth companies which are ideal for holding in an ISA. All seven stocks are forecast by analysts to keep growing pre-tax profit for the foreseeable future.

These aren’t risk-free investments and some of the valuations aren’t cheap. However, we do rate all seven stocks as good ‘buys’ in the current environment and believe they will deliver tasty returns over the coming years.

B&M European Value Retail (BME) 372.7p

Multi-price discounter B&M European Value Retail (BME) is a self-funded growth company offering a compelling play on trends towards value and convenience. The highly cash generative company pays a progressive dividend and offers scope for special distributions too.

On course for its 14th consecutive year of profit growth, B&M is a resilient, high quality structural winner that should grow in economic weather fair or foul.

And while it is a physical store retailer, B&M’s lease portfolio with an average of four years outstanding gives it welcome flexibility.

B&M benefits from higher average transaction values in the good times and rising footfall and volumes in the bad. The company is participating in two of the three key trends re-shaping modern retailing: the rapid expansion of the value sector and the rise of convenience.

It has yet to participate in online retailing as its bargain wares don’t really lend themselves to online transacting.

The bulk of B&M’s revenues are derived from frequent-visit customers, who flock to B&M to top up on food or fast moving consumer goods essentials, or to purchase competitively priced seasonal, garden and homeware products.

Following a wobble at the back end of 2018 – reflecting concerns over slowing like-for-like sales amid unhelpful weather and a tougher backcloth in Germany – B&M’s share price has rallied and we think the rebound can continue.

UK like-for-like sales softened by 1.6% in the third quarter to 29 December, with B&M’s performance held back by a tough November, but this also reflected a strong prior year comparable of 3.9% growth, while overall group sales grew by a solid 12.1% in the quarter.

Encouragingly, gross margin expanded in the third quarter thanks to strong inventory control and B&M said positive sales momentum had continued into January.

The retailer’s discount convenience chain Heron Foods continues to trade strongly, and B&M not only boasts a platform for growth in Germany through its Jawoll chain – it has also made in-roads into France via the recent acquisition of the Babou store chain.

Analysts expect B&M will report £247m pre-tax profit when it reports results for the year to March 2019 (2018: £221m). This figure is expected to hit £277m next year and £311m the year after.

Carnival (CCL) £37.97

After a turbulent 12 months for the share price, cruise operator Carnival (CCL) is looking attractively valued ahead of a period of anticipated solid growth and as such the company is an excellent candidate for inclusion in an ISA portfolio.

The company, which is dual-listed in the US and UK, has a portfolio of brands including Carnival Cruise Line, the most popular cruise line in North America. It is comfortably the industry leader with upwards of 100 vessels and a market share somewhere close to 50% based on the number of passengers.

The company has been seen as a beneficiary of an ageing population – as cruise holidays tend to be popular with older holidaymakers – and the rapidly expanding Chinese cruise market.

The shares came under pressure in 2018 as rising oil prices and the stronger dollar drove up fuel costs. This headwind abated somewhat in the final quarter of the year, but by the start of 2019 Shore Capital noted the market was discounting a 6% to 8% decline in net revenue yields.

This metric reflects how much the company makes per available passenger cruise day on each ship, and to put Shore’s observation in context it fell 9% following the global financial crisis. The net revenue yield increased 3.7% in the November 2018 financial year although more modest growth of 1% is expected in 2019.

The company’s investment in fleet replenishment is expected to result in cost savings and a higher rate of capacity growth, making it less reliant on growth in the revenue yield to drive earnings higher.

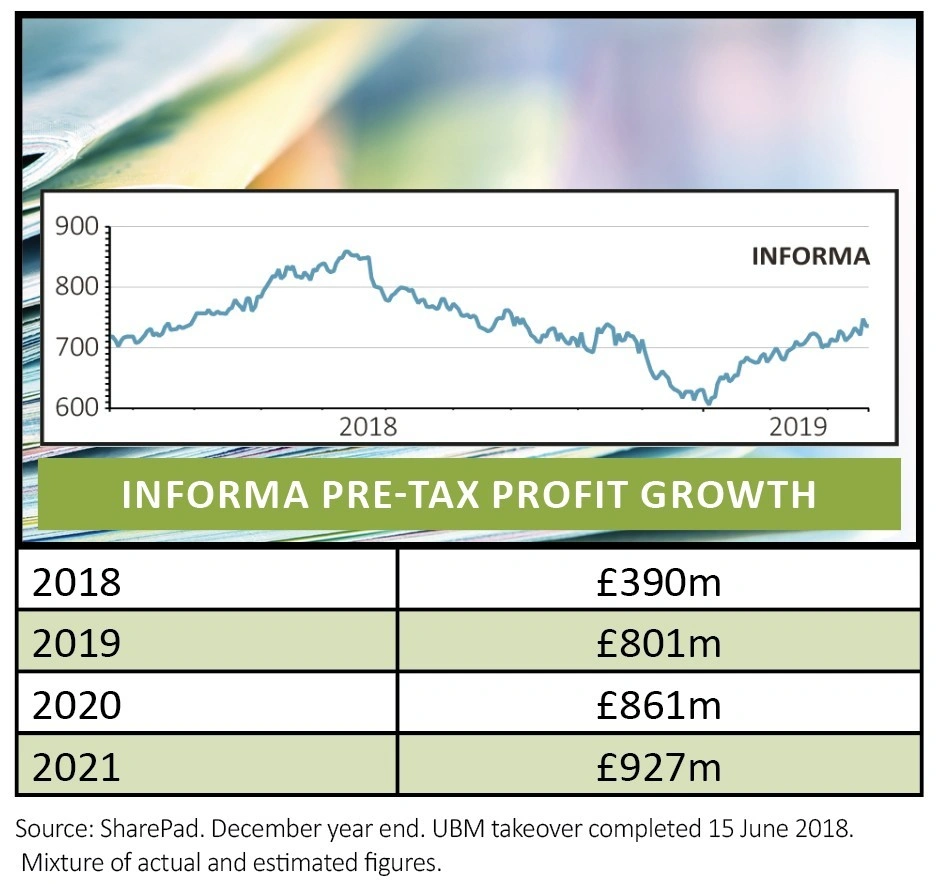

Informa (INF) 736.6p

Diversified media firm Informa (INF) offers solid growth at an attractive valuation. The ongoing integration of UBM, bought last year, should provide a catalyst for the share price in both the short and long-term as the benefits become apparent to the market.

Informa’s most enduring brand is Lloyd’s List, now a digital-only product covering the shipping industry which has been in existence in some form since 1734.

The company has invested in recent years to build a global operation with a focus on specialist business-to-business markets and with a growing proportion of recurring revenue. The company believes more than 65% of its future revenue is ‘visible and predictable’.

Informa Markets – a combination of Informa’s events arm and the exhibition assets picked up from UBM – is the company’s largest division at around 50% of revenue. This is an attractive area of business because it is typically cash generative, has solid visibility with plenty of repeat revenue and, for the leading events in the company’s portfolio, material barriers to entry.

There is also an opportunity to grow by taking established and successful events into new territories.

It is positioned to benefit from growing demand for its data analytics expertise, reflected in increased sales of digital subscription products.

London Stock Exchange (LSE) £46.27

Analysts expect London Stock Exchange (LSE) to deliver very attractive earnings growth over the coming years. However you do have to pay a premium rating for such quality – its shares trade on 23.2 times forecast earnings for 2019.

Berenberg’s Chris Turner says the company has completely changed its business model since 2007, relying less on traditional volume-driven activities and concentrating more on being an information services business and also a clearing house for OTC (over-the-counter) derivatives.

‘This new model exposes London Stock Exchange to some of the strongest structural trends in the finance industry: ETF penetration, OTC clearing, greater risk management and quant investing,’ he explains.

Underlying pre-tax profit is forecast to grow from £865m in 2018 to £1bn in 2019 and £1.12bn in 2020 according to the analyst consensus forecast.

There is scope for London Stock Exchange’s margins to improve as the cost of clearing a trade or selling an additional index licence is close to zero, so nearly all extra revenue should turn into profit.

OTC clearing and the FTSE Russell index business generate half of the group’s revenue. Turner believes they will generate two thirds of group revenue growth over the next three years.

The FTSE Russell business, in particular, is very important to future earnings growth. Most of its revenues are generated from recurring subscriptions to the division’s benchmarks such as the FTSE 100 or Russell 2000.

‘This division is benefiting from the secular increase in the application of quantitative techniques across the asset management industry,’ says Turner.

‘Traditional managers are using far more sophisticated, often bespoke, benchmarks and performance decomposition tools to analyse performance and monitor risks.

‘At the same time, traditional passive products continue to grow, expanding into less mainstream strategies and incorporating more sophisticated (“smart beta”) approaches,’ adds the analyst.

Investors owning this stock shouldn’t expect huge dividends despite the business being highly cash-generative. London Stock Exchange is more likely to use spare cash for acquisitions.

On the flipside, it is worth noting the company has, on average, received a takeover approach from third parties every 2.5 years since it was listed in 2000.

Alpha FX (AFX:AIM) 670p

Shares in foreign exchange specialist Alpha FX (AFX:AIM) have more than tripled since it joined the stock market in April 2017 as earnings have repeatedly beaten estimates.

In its last trading update in December, the firm raised guidance again thanks to strong growth in its core business and in its newly-established institutional business.

Alpha’s core business is providing foreign exchange services to medium-sized UK and overseas firms who need to convert currency for buying and selling goods and services overseas, repatriating profits or expatriating payroll.

The UK corporate foreign exchange market is dominated by the high street banks and is estimated by analysts at Liberum to be worth £445bn per year.

Alpha’s UK clients include retailers such as ASOS (ASC:AIM) and Halfords (HFD) which buy goods in euros or other currencies and sell them to UK customers in pounds.

Other Alpha customers include energy companies whose products are bought and sold on world markets primarily in US dollars.

It also provides hedging programmes to help companies calculate how much foreign currency they need to buy and how far ahead they need to buy it to manage their cash flows and liabilities.

A big selling point for Alpha is its online platform which allows clients to manage their currency exposure on an almost bespoke basis. This has driven up customer numbers and meant customer retention is strong.

The platform comes as standard with no upfront cost or annual maintenance fee and more clients are moving their treasury and currency management functions onto Alpha’s system to save money.

During 2017 the number of customers increased by 39% to 310 and last year the number increased by 55% to 482 as Alpha expanded its offering to funds and institutions.

Along with the increase in customer numbers, the average revenue per client is increasing. In the last two years this has risen 28% from £38,000 to £48,700 per client and this year that number is likely to be above £50,000 per client.

The institutional investor and funds market is potentially huge given the amount of currency dealing involved in managing global investment pools.

Chief executive Morgan Tillbrook says Alpha is ‘barely scratching the surface’ of the firm’s potential given how large its target markets are and how small its turnover is currently.

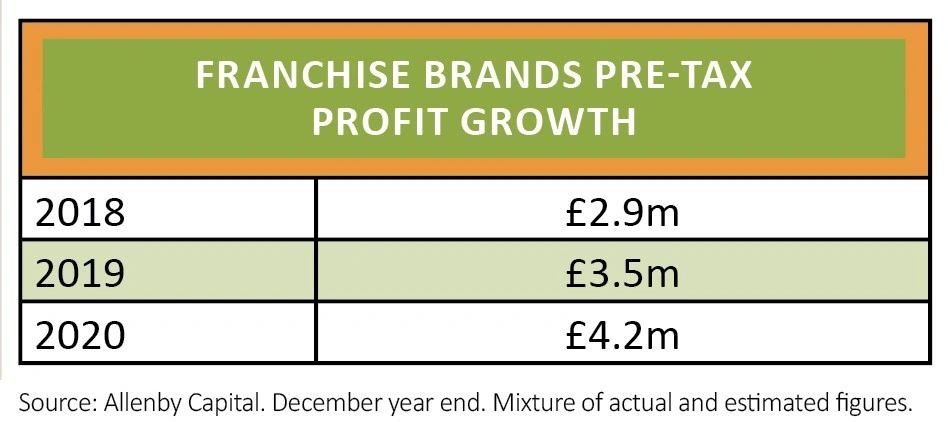

Franchise Brands (FRAN:AIM) 74.5p

The £58m company is run by Stephen Hemsley, best known as the chairman (and former chief executive) of Domino’s Pizza (DOM) and someone who certainly knows how to get the most from the franchise business model.

Franchise Brands is growing profit and dividends fast and forecasts suggests this trend will continue for the foreseeable future.

Allenby Capital expects pre-tax profit to rise from £2.9m in 2018 to £3.5m in 2019 and £4.2m in 2020. The dividend increased by 34% in 2018 to 0.67p and is expected to hit 0.91p in 2019 and 1.12p in 2020.

The company has four main franchise businesses: drainage services group Metro Rod, vehicle repair specialist ChipsAway, cleaning service Ovenclean and dog walking service Barking Mad. The latter two aren’t crucial to the investment case as they only contribute a small amount to group earnings. Buying its shares is really about taking a view on the former two names.

Group fee income grew by 41% to £17.9m in 2018 with management service fee income up 32% to £10.9m. Net debt fell from £6.3m to £5m in the year. Hemsley believes all borrowings will be paid off ‘in a couple of years’.

Metro Rod was acquired in April 2017 and is expanding through various means. For example, Hemsley says franchisees are now being encouraged to find more of their own work and they are already having success on a local basis with social housing landlords, for example, as well as national contracts.

Franchise Brands has pushed more aspects of work to the franchisee as part of a wider scheme to lower the management service fee to help franchisees and make itself more competitive. It will still do all the billing work and collect money on their behalf, therefore keeping control of the cash flow.

Metro Rod has a 4% share of the drainage market and it hopes to grab more market share by a mixture of having more focused franchisees and expanding the range of its services. Franchise Brands also has a small franchise operation called Metro Plumb.

ChipsAway is shifting from being a van-based operation where the franchisee pays a monthly fee to running physical centres in order to undertake larger repairs and where the franchisee pays 10% of their turnover as a management service fee.

SimplyBiz (SBIZ:AIM) 206.04p

Since listing on the stock market just under a year ago, compliance and business services firm SimplyBiz (SBIZ:AIM) has performed strongly in terms of financial results but the shares have only recently sparked into life.

SimplyBiz is the UK’s leading provider of compliance and other business services to independent financial advisers (IFAs) and financial institutions and is growing its sales rapidly due to a combination of higher customer numbers and an expanding product range.

Following the pension freedom reforms of 2015 and with the increasing need for professional advice on investing, mortgages, tax and estate planning, IFAs are filling the gap left by the big banks who pulled out of advising customers in the wake of mis-selling scandals such as PPI.

The core Intermediary Services division works with more than 3,700 financial advisers, mortgage advisers and consumer credit firms which are authorised and regulated by the Financial Conduct Authority (FCA) through a membership model.

Revenue for the year to December 2018 was up by 15% to £50.7m thanks to an 8% increase in membership numbers while operating profit rose by 20% to £11.4m thanks to the operational leverage of more volume going through its technology platform.

As regulation increases, SimplyBiz can sell additional services to its existing member firms as well as taking on new firms. Last year ‘additional services income’ was up 7% to £4.5m thanks to GDPR (new data laws) and other new rules and this year there is more regulation coming.

Investment in technology is one of the key differentiators in business these days and those that invest are tending to take greater market share.

In March last year SimplyBiz launched an online investment advice support platform called Centra which is designed to be a ‘one-stop-shop’ for financial planners giving access to product research, comparisons, ratings and suitability tools. In just nine months 2,300 of its 3,700 member firms signed up.

A second income stream is reselling its industry-leading back-office software to its members and last year software licence income was up almost 25%.

As SimplyBiz developed the Centra platform it formed a close working relationship with Defaqto, the ratings and technology group with the largest database of financial products in Europe, and this month it bought Defaqto.

Not only is Defaqto highly cash-generative but it has almost 100% repeat revenues so earnings visibility is excellent. By selling Defaqto’s products alongside its own SimplyBiz expects the deal to add to earnings within 12 months.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.