Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy aren’t challenger banks living up to their billing?

Following the financial crisis more than a decade ago and the public bailout of Lloyds (LLOY) and Royal Bank of Scotland (RBS), the UK banking market was opened up to a new wave of companies who it was hoped would genuinely challenge the established players.

Without ‘legacy issues’ such as mis-selling scandals, and without networks of high street branches weighing on their costs, the idea was that these fresh-faced ‘challengers’ would represent a new, modern way of banking.

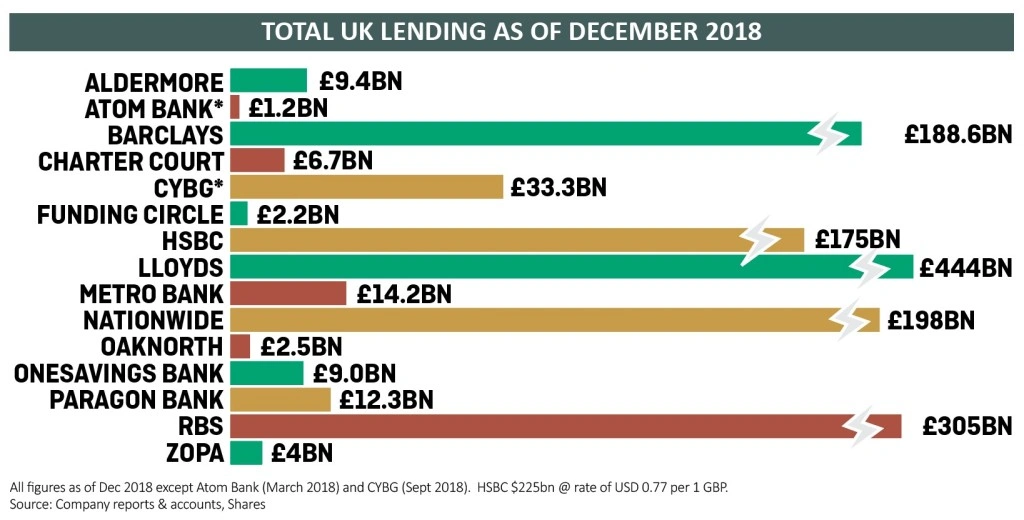

Yet 10 years on from the crisis and the launch of Aldermore, the first ‘challenger bank’, the high street lenders still dominate personal and business banking.

As Phillip Monks, founder and chief executive of Aldermore, observes: ‘If you look at the whole challenger bank experiment, the aim was to create diversification. That hasn’t been achieved.’

NEW KIDS ON THE BLOCK

Most of the 75 challenger banks operating in the UK today are genuinely new businesses, set up in the past decade with freshly-minted licences and most aiming to grab a piece of the lucrative retail banking market.

As well as offering better rates on savings and mortgages, meaning they often topped the best-buy tables, start-ups like Atom, Monzo, Revolut, Shawbrook and Starling had whizzy technology and offered

a better, more personalised service with low fees and no confusing jargon.

Best of all, customers could do all their banking online or on their mobile phone without ever needing to go into a bank branch again.

A FEW OLD FACES GOT IN ON THE ACT

Not all of the challengers were new faces: Virgin Money had been around since the mid-1990s while the Co-operative Bank can trace its roots to 1872 and TSB’s roots go back as far as the early 1800s.

Yet for all their long pedigree and supposed ‘ethical’ credentials, none of these more established players have made much of an impact.

Virgin Money fell quietly into the arms of traditional lender CYBG (CYBG) last October, while Co-operative Bank had a £1.5bn ‘hole’ in its accounts due to loan losses acquired through the merger with Britannia Building Society. The bank struck a £700m rescue deal last year with a group of US hedge funds.

TSB, which used to be part of Lloyds, last year left millions of customers without access to their finances after a series of meltdowns with its new IT system. This led to a Financial Conduct Authority (FCA) investigation and the resignation of chief executive Paul Pester last September.

HYBRID MODEL LOOKED LIKE A RUNNER

Metro Bank (MTRO), formed in 2010, combined the low-cost approach of the ‘challengers’ with the branch network of

the old guard.

Everything seemed to be going well until earlier this year chief executive Craig Donaldson revealed that Metro had mis-classified some of its buy-to-let and commercial property loans and had under-provisioned for them, necessitating a £900m increase in reserves.

Worse, it later transpired that it was the Bank of England which spotted the mistake and not Metro itself, raising doubts about its accounting and leaving investors wondering whether they and the authorities had been misled.

LIMITED SUCCESS IN SPECIALIST LENDING

Some of the start-up banks have carved a niche for themselves providing loans to consumers and small businesses who are considered too risky by the big banks because they have low credit scores or unpredictable incomes.

This type of lending requires more in-depth analysis and carries a higher rate of interest to compensate for the increased risk. Higher rates on lending and often lower costs mean margins can be good.

Others have focused purely on business banking and have targeted the hundreds of thousands of small firms which the big banks either service poorly or overlook completely.

Oaknorth lends to small businesses which need capital to grow or to fund management buy-outs or takeovers. It has lent more than £2.5bn since it launched in 2015 and the latest accounts show that Oaknorth made three times as much profit last year as it did the year before.

Backed by Softbank and other private investors, Oaknorth was valued at $2.8bn in its latest funding round and therefore has fintech ‘unicorn’ status.

Funding Circle (FCH), which is an alternative lender rather than a challenger bank, increased its loans under management by 55% last year to £3.15bn and lent more money to small and medium enterprises (SMEs) last year than all the high street banks combined according to Bank of England data.

However it is yet to turn a profit as it continues to invest heavily in marketing, technology and people in order to grow.

SCALE IS KEY TO GROWING MARKET SHARE

In theory once the challengers have won a slice of the market, be it in personal or business banking, they can start to eat into some of the other businesses dominated by the high street lenders.

Sadly success in one sub-set of the market is no substitute for scale, which is what most of the challengers lack.

Just this month OneSavings Bank (OSB) – one of the most profitable start-ups – announced it was merging with another

very profitable start-up, Charter Court Financial (CCFS).

The main reason for the two banks getting together was to create a specialist lender ‘with greater scale and resources’ to go after more growth opportunities.

OFF TO THE RACES OR GOING TO THE DOGS?

According to consultancy Accenture the challenger banks have so far taken 14% of the UK’s banking revenue, so the rest of the sector needs to take the competitive threat seriously.

However those who compare the challengers to companies with disruptive business models like Airbnb, Netflix or Uber ignore the fact that the latter operate on a global scale and not just in one market. They aren’t competing with each other for the same dollar of customers’ money.

They also ignore the fact that the big traditional banks have the resources – if not the skill-set or the savvy, yet – to adopt the challengers’ playbook and launch clever new products and services of their own which they can cross-subsidise through the rest of their business lines.

It was hoped that the £775m pay-out from the Banking Competition Remedies (BCR) fund, set up during the financial crisis and funded by RBS, would help transform the landscape.

However the first round of awards – to Metro, Starling and Tide – has already created controversy.

Metro Bank received its award roughly the same time as revealing a big miscalculation in its loan book. Starling has been in the spotlight over its long-standing relationship with BCR director Aidene Walsh, raising questions about a potential conflict of interest. And Tide doesn’t have a banking licence, instead relying on its partner ClearBank which was only recently granted one.

The second round of awards is expected to go to more traditional lenders with CYBG and Nationwide thought to be strong contenders.

HUDDLING TOGETHER FOR WARMTH

The challengers promised much but many will either need to throw greater resources at the market or find new ways to gain share.

There may be more mergers following the example of OneSavings Bank and Charter Court, but more likely there will be more collaboration on products.

Monzo seems to be taking this option and is partnering with other challengers such as Oaknorth to offer its customers access to new products like high-interest savings accounts.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.