Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineElectric energy plays

Meeting global energy demand will be a key challenge in the decades ahead but it should also create opportunities for investors.

In this article we will discuss how you could benefit from some of the long-term trends in the power generation market through both funds and individual stocks.

Global energy demand will rise by at least 30% until 2040, according to investment bank UBS.

The need to produce more energy must also be balanced against the need to address climate change concerns with Glencore (GLEN) recently announcing plans to cap coal production amid pressure from shareholders regarding environmental, social and governance (ESG) issues.

UBS suggests an energy strategy employing a mix of renewable and non-renewable sources will be required, adding: ‘We believe there are investment opportunities across the entire energy sector.

‘We recommend that long-term energy investors consider providers of all energy sources (oil, natural gas, wind, solar) as well as companies that are advancing technologies for a more efficient and diverse energy future.’

Taking inspiration from this approach, and recognising that a lot of traditional energy funds are over-exposed to a utilities sector facing significant structural challenges, we have highlighted prospective investments which span a variety of different elements of the energy market.

MAJOR THEMES

There are several big themes at play in the energy sector at present. The urbanisation process in major emerging markets India and China, and to a lesser extent Africa, is driving energy demand as more households join the grid and as power is required to heat and cool buildings, and for construction, manufacturing and transportation.

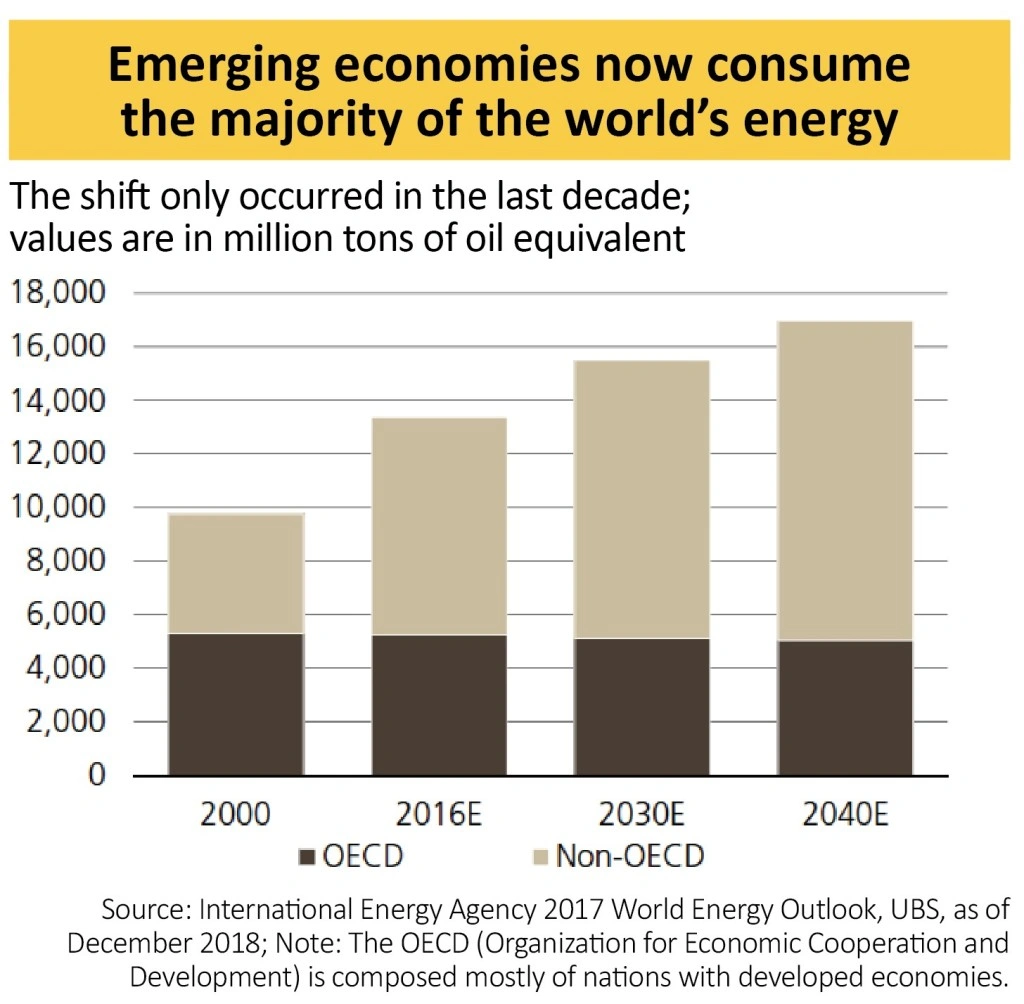

Emerging economics have already overtaken demand from developed countries in the last decade thanks in large part to rapid growth in China.

A big chunk of this extra energy requirement is expected to be met by renewables, though there will be a challenge in delivering the required infrastructure.

Energy consultant Wood Mackenzie recently cast doubt over India achieving its target of 100-gigawatt solar electricity capacity by 2022.

The transformation in how vehicles are powered is another key trend. The electrification of cars, trains and other forms of transport is reducing demand for petrol (and its feedstock crude oil). It is also increasing consumption of electricity as well materials such as nickel, cobalt and lithium that are used in the batteries which power electric vehicles.

UBS believes fuel efficiency in petrol and diesel cars is likely to make a larger contribution to moderating demand for petrol. Its forecasts suggest fuel efficiency gains could reduce oil demand by 17m barrels of oil per day (bopd) by 2040 compared with a 2.5m bopd impact from growth in electric vehicles.

The need for support from global governments

The International Energy Agency estimates that of the rough-$2tn required investment in energy each year to meet future energy demand, approximately 70% will be derived from governments or dictated by regulatory requirements.

This is a risk for investors in the energy sector to consider given the lack of enthusiasm from the Trump administration in the US for cleaner energy solutions.

Electrification

Electrification across key end uses, particularly in areas like buildings and transport, will lead to a doubling of electricity demand by 2050, forecasts US research firm McKinsey.

Several major car manufacturers are committed to phasing out petrol and diesel models and replacing them with electric vehicle alternatives amid pressure from global governments to reduce carbon emissions.

One potential obstacle to more widespread adoption of electric vehicles is the availability of the metals used to produce their batteries.

Bank of America Merrill Lynch says: ‘Electric vehicle batteries require a lot of metals, including nickel, lithium and cobalt. In particular, cobalt is where we believe the key risk lies due to the huge supply concentration in Congo, which produces 62% of the world’s output. The DRC just underwent a tumultuous election season.

‘Although the transfer of power has been peaceful so far, the country has a long history of civilian unrest and corruption. Any major disruption to cobalt today would likely curb electric vehicle proliferation in the early 2020s, in turn supporting long dated crude oil prices.

‘Car producers may gradually substitute from cobalt to nickel over the next two decades. In turn, this shift may lead to soaring demand for nickel, creating another supply squeeze as mine expansion plans are limited.’

RENEWABLE ENERGY EXPANSION

McKinsey expects a big expansion in renewables to be central in accommodating the extra demand for electricity. It forecasts that solar and wind will become cheaper than fossil fuels in most parts of the world within the next decade.

The idea that China and India will be enthusiastic adopters of renewable energy might not tally with the impression of smog-choked and pollution-filled cities we sometimes have in the West. Yet while coal still accounts for a big chunk of power generation in both countries, China is already the leading country in terms of electricity production from renewable energy sources.

James Smith, manager of Premier Global Infrastructure Trust (PGIT), says: ‘I am excited by the opportunities available in Asia. As a European, it is clear to see the direction of travel including more renewable energy, cleaner disposal of waste, more sophisticated and efficient ports, as well as better, more numerous and safer roads.’

HOW TO INVEST IN THIS THEME

Shares has consistently championed car testing specialist AB Dynamics (ABDP:AIM), which has gone up by more than 18-fold in value since joining the stock market in 2013. We see potential for further gains with its services in big demand from an automotive industry undergoing a period of significant change including the transition to electric vehicles.

The best performing renewables investment trust, based on total returns over five years, is Greencoat UK Wind (UKW). It exclusively invests in operating onshore and offshore UK wind farms. Like the rest of its peer group, whose uncorrelated returns are in demand with investors, Greencoat trades at a material premium (12.4%) to net asset value at the current 136.4p price.

That looks too high to justify at present, so wait for the premium to reduce before considering an investment. For now, a better alternative might be iShares Global Clean Energy (INRG) which for an ongoing charge of 0.65% offers exposure to a collection of 30 global stocks active in the clean energy space including operators of wind and solar assets and providers of ancillary services.

Gas

According to McKinsey gas will be the only fossil fuel to grow its share of global energy demand until 2035. It believes this will be principally driven by industrial demand, particularly as China looks to wean itself off coal.

McKinsey’s analysis suggests gas demand growth from China will be greater than the next 10 largest growth countries combined and will represent nearly 50% of demand growth over the next 15 years or so.

Technologies such as gas-to-liquids (GTL), liquefied natural gas (LNG) and compressed natural gas (CNG) have made gas more transportable and versatile.

Gas has traditionally been used to heat and light homes and businesses, as well as to power industries. Other markets are opening up, including the use of LNG as an alternative to diesel and heavy fuel oil in transport.

The main pricing benchmark for natural gas in the US is Henry Hub. It has come under pressure in recent years thanks to the major new source of supply provided by the successful exploitation of shale gas. However, the price could gain some support going forward as the US ramps up its exports of gas.

Historically it could only serve a local market where supplies were plentiful. Opening up its sales distribution to other countries could, in theory, make the gas price stronger as there would be a wider field of buyers.

The first US exports of LNG were made in February 2016 and according to the US Energy Information Administration the US LNG export capacity is expected to increase from 4.9bn cubic feet per day (bcfpd) at the end of 2018 to 8.9 bcfpd by the end of 2019 as new export terminals come online. This would give the US the third largest capacity globally after Australia and Qatar.

An increase in LNG exports could help rebalance supply and demand and drive the Henry Hub benchmark higher – it already hit a four-and-a-half year high in November 2018 of $4.93 per million British thermal units (mmBtu), though the price has subsequently settled lower.

HOW TO INVEST IN THIS THEME

Integrated oil and gas firm Royal Dutch Shell (RDSB) has made natural gas a key plank of its long-term strategy. A big part of the rationale for the £47bn acquisition of BG Group in 2015 was the latter company’s leading position in LNG.

In October 2018 Shell sanctioned a $12bn investment in a Canadian LNG project citing the fact that the world’s appetite for LNG had exceeded expectations and made the project viable. Patient investors who believe this big bet on natural gas can pay off would currently enjoy a dividend yield of 5.9% at the current share price of £24.20. We think Shell deserves a place in a diversified portfolio.

More direct access to natural gas prices is possible through exchange-traded product (ETP) ETFS Natural Gas (NGSP). For an ongoing charge of 0.49% the ETP tracks the Bloomberg Natural Gas Subindex which is designed to reflect movements in the price of natural gas futures contracts.

Energy efficiency

Significant improvements in energy efficiency in buildings and transportation infrastructure will be an important part of confronting the global energy challenge. Without these UBS believes the increase in demand could be twice its projected level of 30% out to 2040.

Smarter buildings will have to be designed and built with elements such as smart meters, better insulation and LED lights, more fuel-efficient cars and higher efficiency new appliances such as fridge-freezers and washing machines.

In December 2018 SDCL Energy Efficiency Income Trust (SEIT) was floated in London by specialist asset manager SDCL raising £100m to invest in several energy efficiency projects. It is looking to achieve a total return of between 7% and 8% per year.

While investors may want to see more of a track record before investing in the trust, which currently trades at a 3.1% premium to net asset value at 101p, examining the areas it is focusing on offers some useful insights into where improvements in energy efficiency are being targeted.

Included among its projects are the installation of LED lighting in Spanish banking group Santander’s UK offices and branches, and CCHP (combined cooling, heat and power) equipment at St Bartholomew hospital in London and a Citibank data centre.

CCHP units reduce organisations’ reliance on the national grid and they combine power generation, heating and cooling systems – effectively putting the waste heat from generating electricity to good use.

SDCL Chief executive Jonathan Maxwell told Shares ahead of the float that energy efficiency vehicles would be part of a third wave of infrastructure-linked investments following larger broad-based infrastructure plays like HICL (HICL) and funds which invest

in renewable energy assets.

HOW TO INVEST IN THIS THEME

Irish building materials firm Kingspan (KGP) was founded more than 50 years ago as a small engineering and contracting business. Its recent strategy has focused heavily on the energy efficiency theme.

Kingspan is a global leader in high performance insulation and so-called ‘building envelope’ solutions. The building envelope refers to the walls, floor, roof, windows and doors which form the physical separation between the interior and exterior of a building.

For example, it provided raised access flooring and insulation products on Microsoft’s Dublin-based headquarters which opened in February 2018.

Kingspan’s profit growth has averaged almost 30% per year in the last five years, says stockbroker Davy, and this stellar growth has been reflected by a total return for investors of 197% over that period.

At €38.94 the shares trade on more than 18 times Berenberg’s forecast earnings per share for 2019 but we think this premium valuation, broadly in line with the recent average, is justified with the company returning to expansion mode after focusing on the integration of some material acquisitions.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.