Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineEverything you need to know about modern monetary theory

After the global growth scare of 2018 financial markets appear to be regaining their nerve and verve, at least if global equities are any guide, for three possible reasons.

First, US president Donald Trump continues to dangle the prospect of a trade agreement with China.

Second, the prospect of tighter monetary policy and less liquidity is receding fast. The US Federal Reserve appears to be backing away from further interest rate increases in 2019 and even hinting that it may stop shrinking its balance sheet by the end of this year.

Meanwhile the European Central Bank is publicly debating the merits of further cheap funding for banks, the Bank of England is still studiously inactive and the Bank of Japan continues to keep headline interest rates anchored below zero.

Third, the political shift toward ending austerity is gathering pace. Italy, Spain and France are all edging toward more expansive spending policies, in the wake of public demands for action on growth and jobs, for example, but America is leading the way, with its debate over what is now known as modern monetary theory.

Investors may start to hear a lot more about modern monetary theory, especially as the race for the Democratic Party nomination and then the White House itself heats up in 2020. Now therefore seems like a good time to do some research on what it is and what it could mean for portfolios.

Demand-side policy

Modern monetary theory throws out the supply-side economic orthodoxy ushered in by the Thatcher and Reagan administrations some 40 years ago in the UK, whereby lower taxes and less regulation were seen as spurs to increased supply, more jobs, lower prices and faster growth.

Instead, modern monetary theory focuses on demand-side economics, increasing employment, at least partly through Government spending, to boost aggregate demand that creates further jobs and the virtuous circle of a multiplier effect.

The gathering mantra within the Democratic Party in the US is that the biggest barriers to growth are unnecessary worry about deficits and the Federal Reserve’s control of the supply of dollars.

Adherents to modern monetary theory argue that deficits do not matter, because interest rates are low and that if there is a problem, America’s independent central bank can simply create more dollars to cover the interest payments and debt repayments that would result from the issuance of more debt.

The borrowing can then be used to invest in infrastructure and offer enhanced welfare payments and social support.

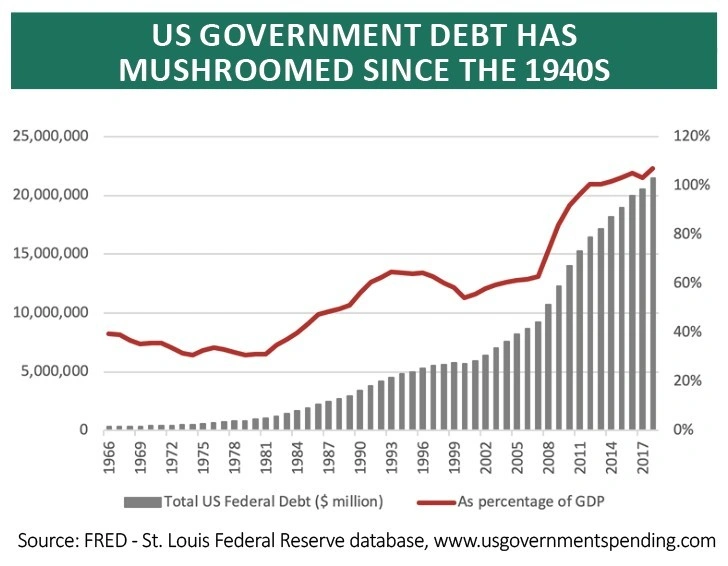

At a time when we are 10 years into what still seems like a fragile recovery, wage growth remains weak and concern over public services is running high, this will look like good politics and good economics to many. Even Warren Buffett, a man who pays no heed to macroeconomics at all when it comes to his investment portfolio, dismisses concern over spiralling government deficits in his latest shareholder letter on behalf of Berkshire Hathaway, pointing out how a 400-fold surge in the US national debt since 1942 has done little to dent American growth, the progress of the S&P 500 or appetite for the dollar.

The case against

Not everyone will buy into this view. Sceptics will counter by arguing that if money printing solved everything then everyone would be at it – and the experiences of those who have tried it, from John Law in eighteenth-century France to Rudolf Havenstein and the Reichsbank in 1920s Germany to Robert Mugabe’s Zimbabwe this century have shown that there is no such thing as a free lunch, paid for by newly-printed cash.

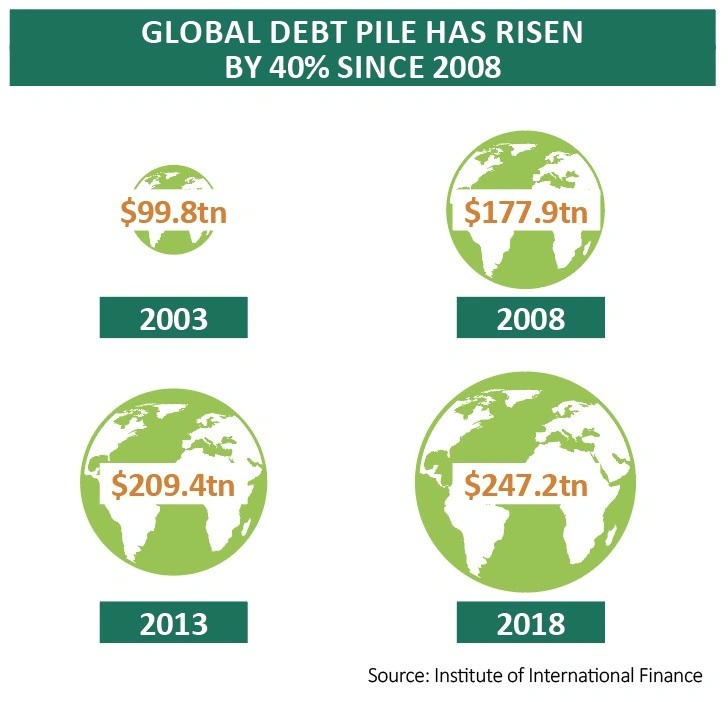

In addition, many will argue that the surge in global debt even since the global financial crisis in 2018 means the recovery has been tepid and the risk of a fresh collapse increased, with artificially-low interest rates providing a necessary prop.

Adherents of modern monetary theory and its critics both know there is one big impediment – inflation. Print enough cash and faith in a currency will eventually ebb and then plunge, as Zimbabwe found out, forcing the production of ever-greater amounts of cash. Modern monetary theory supporters say they will get the balance right. Sceptics will express concern.

Portfolio options

Where investors sit in this debate is up to them. But they will need to at least think about it, especially if the Democratic Party starts to go down this path and looks like it might unseat President Trump in November 2020.

But whether modern monetary theory prevails politically, the move toward less fiscal austerity and keeping monetary policy looser for longer seems set for now.

This may be why equities and gold are currently doing well, although the bond market seems unconcerned, judging by how yields are refusing to go higher.

This may reflect the ongoing influence of central banks’ policies, lingering growth worries and also the fact that the Democrats are far from certain to win next year, as if to remind investors of the need for a balanced portfolio that covers a spread of assets so it can hopefully cope with different possible economic outcomes, ranging from growth and inflation to recession and deflation.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.