Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

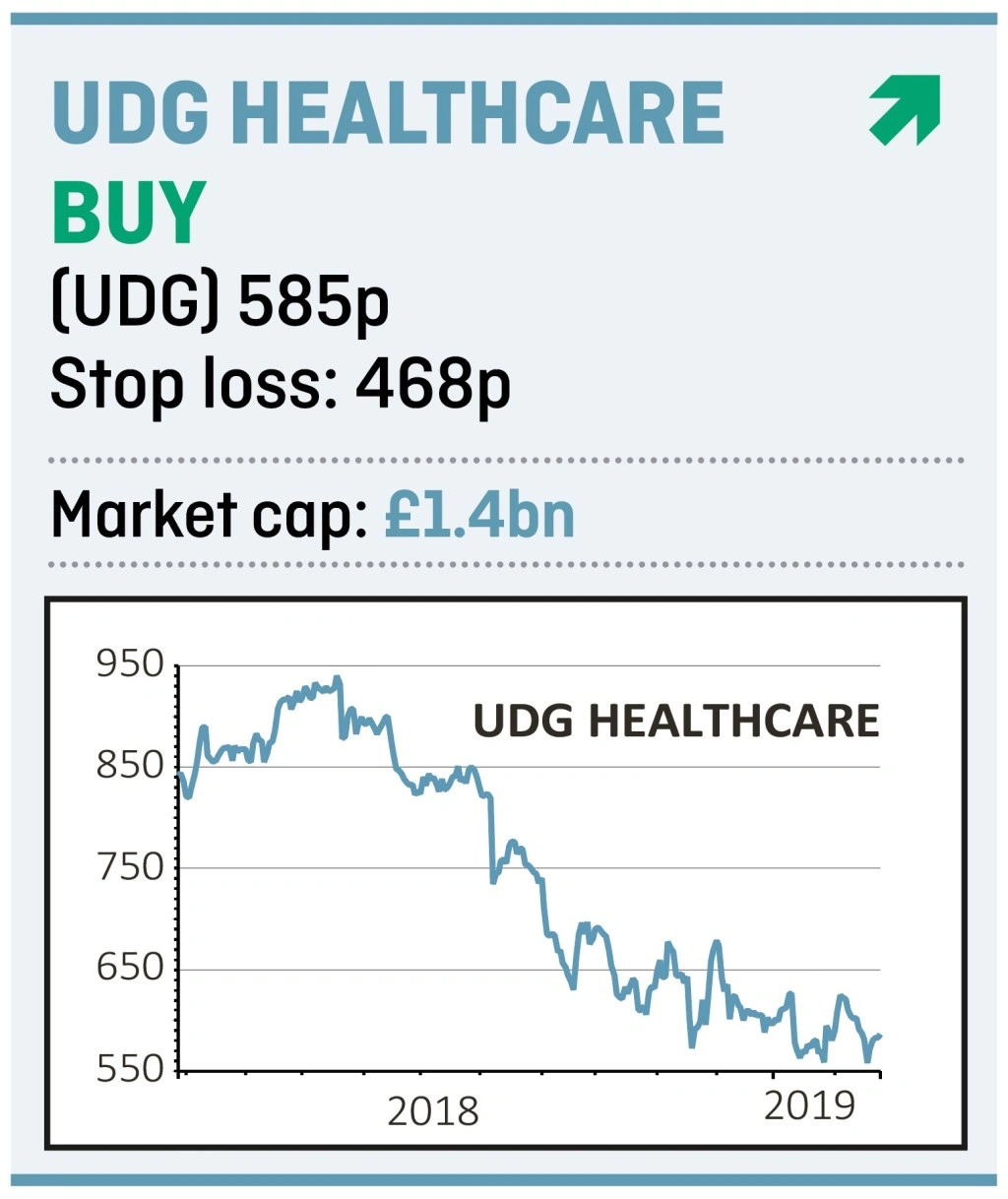

magazineSnap up services group UDG before the market spots recovery signs

The market has been too pessimistic towards drug services group UDG Healthcare (UDG), giving you an opportunity to pick up shares in a decent business while the market is disinterested.

The share price was hammered last year following earnings downgrades linked to part of its business which accounts for less than a quarter of group profit.

A trading update in January implies the affected business – called Ashfield Commercial and Clinical (C&C) – has not only stabilised but also sooner than analysts had expected.

The rest of the business is generally doing fine, including a stellar performance in its first quarter from Sharp which provides clinical trial management and contract packaging to the pharmaceutical and life science industries.

While Sharp has struggled in Europe due to lower activity levels from clients, demand should improve as the European Union has brought in new serialisation rules to prevent the sale of counterfeit medicines.

Liberum analyst Graham Doyle argues UDG’s share price has been unfairly punished by downgrades, flagging its shares have plummeted by 40% since June despite earnings downgrades of approximately 8%.

Doyle says management have been ‘extra cautious’ due to the impact of downgrades on the share price.

The firm’s decision to sell pharmaceutical products distributor Aquilant to H2 Equity last year for up to €23m is positive as it means the company can focus on the higher margin Ashfield and Sharp divisions.

UDG is enjoying a strong start to its financial year as pre-tax profit in the quarter to 31 December is expected to be ‘well ahead’ compared to the same period last year thanks to good underlying growth, partially aided by M&A.

In 2018, UDG acquired communications agency Create NYC and consulting business SmartAnalyst for up to $82.4m to help shift Ashfield’s capabilities towards higher value services.

Pre-tax profit at UDG is forecast to rise from £105.4m in the year to 30 September 2018 to £139.2m in 2019 and £152.9m in 2020.

The shares should be treated as higher-risk until there is further evidence that C&C’s trading improvement can be sustained.

That said, we are encouraged by several directors regularly buying shares since last summer.

While the company pays a small dividend – currently yielding 2.3% based on 2019’s forecasts – investors should expect the bulk of their returns to come from an increase in the value of their shares.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.