Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineA simple guide to pension tax rules

There is a myth that pensions always have to be complicated. In fact, 17% of AJ Bell Youinvest customers said understanding tax was the most complicated thing about retirement investing, while almost one in six said simplification of pension rules would encourage them to save more.

For the vast majority of people, the retirement savings rules are actually relatively simple although there are a few bear traps you need to watch.

This straightforward guide aims to equip you with the knowledge to navigate the pension tax landscape as things stand at the moment. These rules are always subject to the whims of Government and so are likely to change over time.

TAX RELIEF WHEN YOU PAY MONEY IN

One of the main benefits of saving in a pension is tax relief on the money you pay in. The simplest way is to think of it as a bonus in exchange for you locking away your funds until you reach age 55.

The amount of bonus you get depends on the tax band you fall under. If you’re a basic-rate taxpayer, you’re entitled to 20% tax relief – equivalent to a 25% bonus. So if you pay £80 into a pension, that will automatically be topped up to £100 through tax relief.

Because tax relief is granted at your ‘marginal rate’ – essentially making your contribution tax-free – higher-rate taxpayers are entitled to a further 20% tax relief, while additional-rate taxpayers can claim 25%. This means a higher-rate taxpayer’s £100 pension contribution would cost just £60, while for an additional-rate taxpayer it costs just £55.

However, don’t assume this will happen automatically – in most cases higher and additional-rate taxpayers will need to fill out a self-assessment return in order to claim their extra pension saving bonus.

If you don’t pay any income tax at all you are still entitled to basic-rate tax relief (i.e. 20%), although the total amount you can save in a pension each year is capped at £3,600.

If you’re a Scottish taxpayer, please note the amount of pension tax relief you are entitled to might be slightly different following the revision of income tax bands north of the border. You can find details of how this works here.

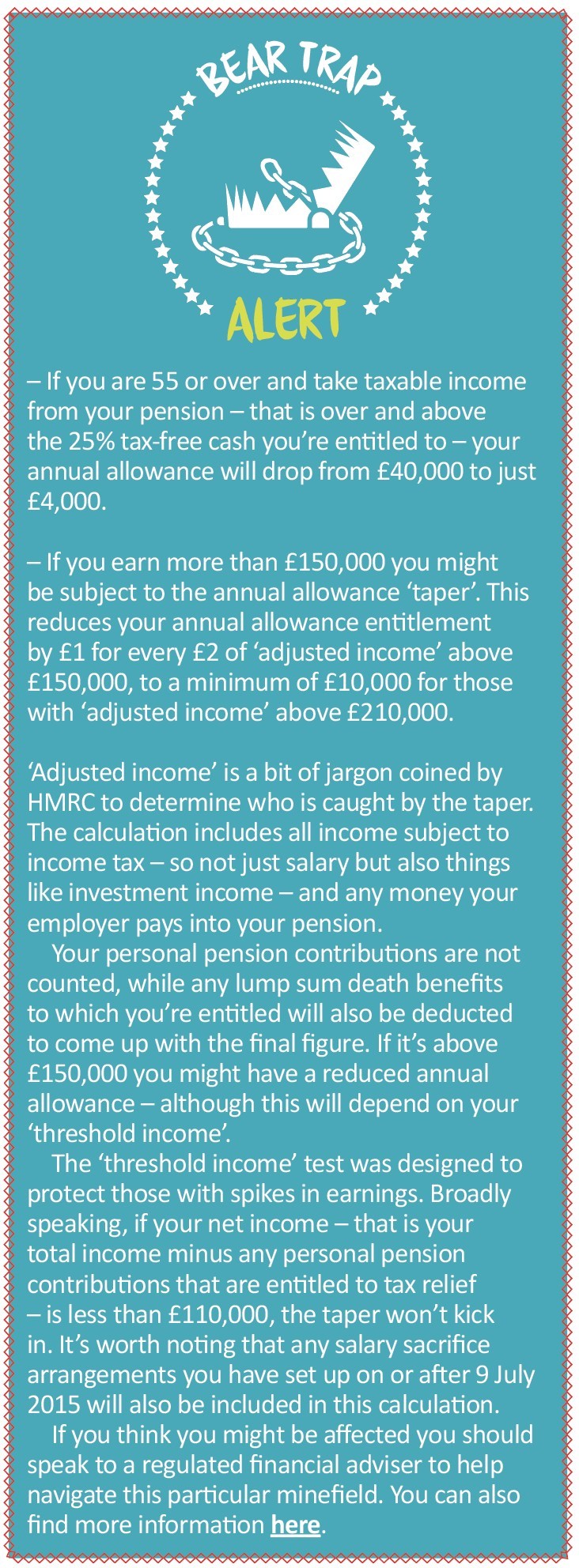

This brings us neatly onto pension savings allowances. There are two main allowances that apply to most people – the £40,000 annual allowance and the £1,030,000 lifetime allowance (due to rise to £1,055,000 from April 2019).

ANNUAL ALLOWANCE

The annual allowance is fairly straightforward. It’s inclusive of the tax relief that goes directly into your pension, meaning you can save £32,000 every year and have that topped up with £8,000 in tax relief (i.e. a 25% bonus).

The amount of money you can pay into a pension each year in order to continue to receive tax relief is also restricted to 100% of your earnings. For example, if you earned £20,000 in 2018/19 the most you could pay into a pension and receive tax relief is £20,000.

LIFETIME ALLOWANCE

The lifetime allowance does what it says on the tin, capping the amount of money you can save tax-free in a pension over your lifetime.

You use up your lifetime allowance when you ‘crystallise’ your benefits – this just means when you take it out of the pension or turn it into a retirement income. For example, if you take £25,000 tax-free and put £75,000 into drawdown, you will have used 9.70% of your £1,030,000 lifetime allowance.

In addition, a lifetime allowance ‘test’ is applied to your entire remaining fund at age 75.

There is a lifetime allowance tax charge if you use more than 100%. The level of the charge depends on whether the excess remains within the pension or is taken out. The former results in a 25% tax charge, while the latter creates a 55% penalty.

There are also numerous lifetime allowance ‘protections’ created by the Government to shield people from being unfairly penalised by historic cuts to the limit.

You can find more details on these protections and the rules governing them here.

TAKING MONEY OUT

When you come to withdraw money from your pension from age 55 you’ll get 25% tax-free. You can choose to take this all at once or receive chunks of money, with 25% of each chunk free of tax (this latter option is referred to in the jargon as ‘UFPLS’).

The remaining 75% of your fund is taxed in the same way as income, so it’s worth bearing this in mind when you decide how much you’re withdrawing.

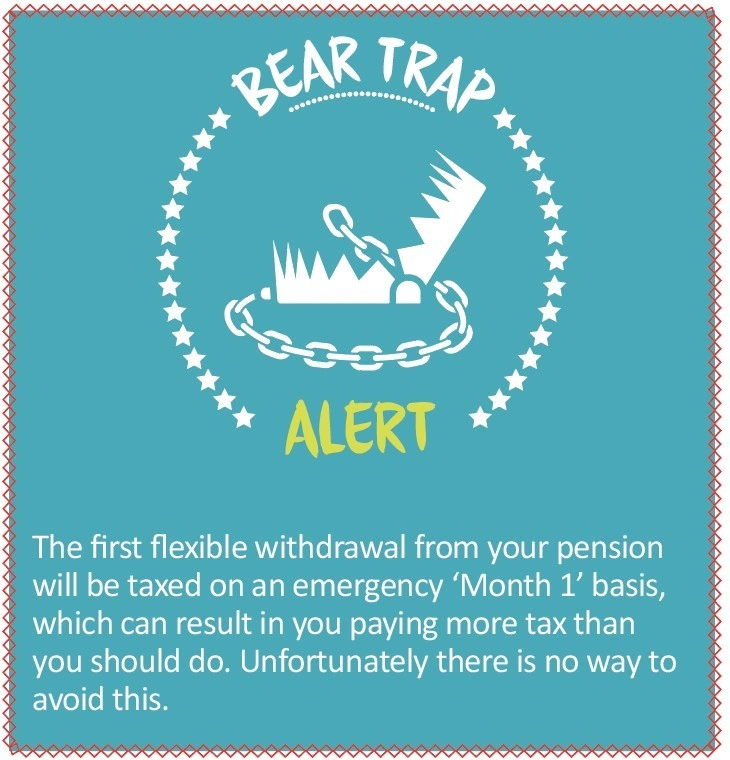

If you are taking a regular income through drawdown this shouldn’t be a problem as your tax will be reduced on subsequent payments to make up for it. However, if you take a single withdrawal then you’ll almost certainly be overtaxed and will need to fill out one of three official reclaim forms to get your money back within 30 days. You can find the relevant forms here.

Alternatively you can wait for HMRC to sort your tax position out for you, although there are no guarantees as to when this will happen.

TAX ON DEATH

Although death may be the final frontier, your pension can live on. Under rules introduced alongside the retirement freedoms in April 2015, anyone who dies before age 75 is able to pass on their pension tax-free.

If you die after age 75 your pension will be taxed in the same way as income – but only once it is withdrawn by the recipient. Any money they haven’t drawn can then be passed on in the same way, meaning wealth can be cascaded down the generations via pensions.

There are a couple of important things to consider. First, you need to make sure you nominate your beneficiary so the right person receives your pension after you die.

And second, the money needs to be transferred into your beneficiaries’ names (‘designated’ in the jargon) within two years of your death.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.