Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

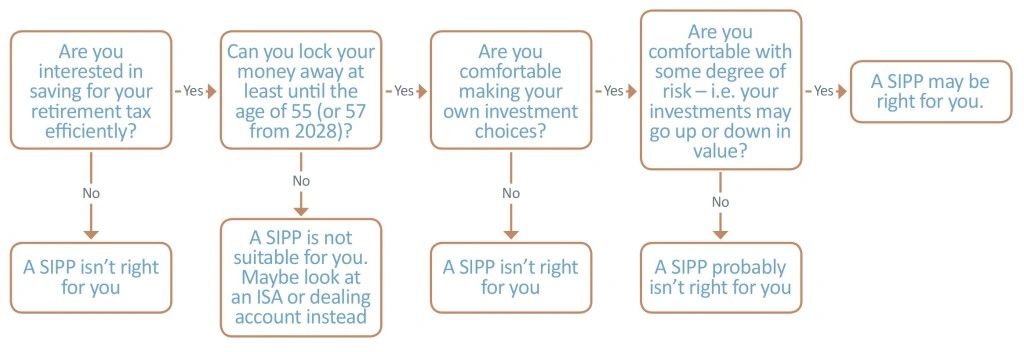

magazineHow do SIPPs work and are they right for me?

A self-invested personal pension (SIPP) is an effective low-cost way for DIY investors to save for retirement – but they are not the right choice for everyone.

SIPPs became more popular in 2015 when new rules made pensions more flexible to manage. At this point, savers were no longer to obliged to buy an annuity with their pension pot when they reached retirement. Instead, individuals are now able to continue to invest and manage their own money even after they stop working.

Investors have more freedom with SIPPs such as being able to choose their own investments from across the market like their favourite funds or investments trusts. Quite often someone taking out a pension scheme with one of the big pension providers will only have access to a limited range of funds run by the pension companies themselves.

Tom Selby, senior analyst at AJ Bell, says: ‘The combination of upfront tax relief and 25% tax-free withdrawals from age 55 are probably the two biggest draws of a SIPP for most people. For a basic-rate taxpayer, an £80 pension contribution will automatically become £100 in their SIPP.’

THE BENEFITS OF A SIPP

SIPPs have a great number of benefits, not least their low cost, which is often a fraction of what big legacy pension schemes charge or what you might pay if you invest through an adviser.

With AJ Bell Youinvest, for example, there is no fee for setting up an account and investors are charged 0.25% a year of the value of their assets up to £250,000.

HOW DO I CHOOSE A SIPP?

Which provider you choose will depend on the amount of assets you have and how often you trade.

Some fund supermarkets charge a flat annual fee for having an account while others charge a percentage of assets, which tapers down depending on how much you have invested.

Usually, if you set up a regular investment plan – meaning you arrange a direct debit to contribute a certain amount to the SIPP each month – there is no minimum amount required by a provider to set up a SIPP. If you are setting up the account with a single lump sum, you will typically need at least £1,000 to invest.

Many providers will also accept transfers in if you already have pension savings elsewhere. It is important to check these factors with a provider before you open an account.

HOW MUCH CAN YOU SAVE INTO A SIPP?

Another major attraction of SIPPs is that they allow you to start saving early. Parents and grandparents, for example, can open a SIPP for a child from the moment they are born.

Money saved into a child’s pension receives tax relief just as adult pension contributions too, making them an incredibly tax efficient way for relatives to save. Parents can save up to £2,880 a year into a Junior SIPP, which is topped up to £3,600 through tax relief.

Up to £40,000 a year can be put into an adult pension, according to rules for the 2018/19 tax year. This is subject to tax relief, so basic rate taxpayers can contribute £32,000 and higher rate taxpayers £24,000 to achieve the maximum annual contribution.

Although the amount you can pay into a pension is limited by your earnings, any UK resident under the age of 75 can put at least £3,600 into their SIPP each year, whether they’re working or not. This would be a contribution of £2,880 with tax relief at 20%, bringing the total contribution to £3,600 a year.

Selby adds: ‘SIPPs are also increasingly used as inheritance tax planning vehicles by savvy investors. Savers who die before age 75 can pass on their entire fund tax-free to their beneficiaries. After age 75 the money is taxed in the same way as income, but only when it is withdrawn from the account.’

CAN I HAVE A SIPP AND A WORKPLACE PENSION?

Because SIPPs are personal pension plans they are unlikely to benefit from workplace pension contributions.

This means they may be a sensible choice for a self-employed worker but potentially not for someone who would otherwise be missing out on valuable contributions from their employer.

You are allowed to have both types of account, but often it is better to prioritise a workplace scheme if you can only afford to contribute to one, so that you don’t miss out on your employer’s contributions.

Under auto-enrolment, all employers must automatically put workers into a pension scheme with 2% of an employee’s qualifying earnings paid in by the employer and 3% by the employee.

These contribution levels will rise to a minimum of 3% and 5% respectively in April 2019. For this reason, a SIPP is often used as a top-up to a workplace scheme or as a vehicle to allow you to take an income in retirement in a flexible way.

You can also transfer existing pensions into a SIPP but make sure you consider whether you’re giving up any guarantees under your current scheme.

WHEN CAN I WITHDRAW MONEY FROM A SIPP?

Money saved into a SIPP cannot be accessed until you reach age 55 but you can continue paying into an account until age 75.

The flexibility of a SIPP means that you can invest the money in a wide range of assets and also withdraw the money in a number of ways. But this freedom may also be a drawback for those who are less confident in managing their money.

Selby says: ‘If you are using a SIPP to take an income through drawdown, for example, you need to manage your withdrawals and investment strategy to ensure you don’t run out of money before you die.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.