Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow much do you need to save for a good retirement?

People work all their lives to be able to retire comfortably, so when you come to hand in your work pass and say goodbye to your desk you want to make sure you’ve saved enough to enjoy retirement.

Some people worry that they have left their pension saving too late, and so bury their heads in the sand. But even latecomers can build up a decent size pot to live off in retirement if they follow a few golden rules.

THREE GOLDEN RULES:

Make use of free money from your employer

Make sure you use all the employer contributions you’re offered. Many companies will pay a certain amount into your pot depending on how much you put in; for example, they may match your contribution up to 5%. This means if you’re only paying in 3% of your salary you’re missing out on an extra 2% from your employer.

Check if you need to claim back your tax relief

You’ll get automatic tax relief at 20% from the Government, but if you’re a higher or additional-rate taxpayer (meaning you pay 40% or 45% tax) you might need to claim back some extra money, depending on how your scheme is set up.

If you contribute to your pension through salary sacrifice you won’t need to do anything, but if you pay into your own SIPP you’ll likely need to claim back the extra money through your annual tax return.

Annoyingly for some, you’ll end up getting that tax back as a rebate, and so will need to then pay that into your pension if you want it added to your pot.

Check what you’re invested in

Most people pay their money into their pension but don’t ever look at what they’re invested in.

Research from 2017 by the Pensions Policy Institute found that 94% of people were in their pension provider’s default fund.

To maximise your returns and take control of your cash you need to log in to your company pension system and check where you money is being allocated. That way you can pick your investments and adjust them according to your stage of life, risk level and views of the investment outlook.

HOW MUCH DO YOU NEED TO SAVE TO BUILD A PENSION POT?

There is a limit on how much you can save into your pension each year and over your lifetime and still get the Government’s pension tax relief.

For most people the limit each year is £40,000 or up to 100% of their income in the year, depending on which is smaller.

There is an overall limit of £1.03m, which is the maximum you can save in your pension over your lifetime without facing a tax charge, although this is increasing in April this year to £1.055m. This valuation is determined when you come to use your pension pot, either to take money out or buy an annuity, or when you reach the age of 75.

Obviously most people don’t reach a pension pot of more than £1m. A 25-year-old starting out with their pension savings would need to put away £1,000 a month to reach their lifetime allowance by the age of 55, assuming basic-rate tax relief and annual growth of 5% after any charges have been taken off.

If you assume that they save until the age of 65 – so 40 years of pension savings – they would have £1.9m if they contributed £12,000 every year.

SAVING £200 A MONTH INTO A PENSION WOULD BE A GREAT START FOR A 25-YEAR-OLD

For many 25-year-olds it’s not realistic to put away £1,000 a month. Instead, if we assume they start with £200 a month until they reach the age of 35, and then increase it to £400 a month until the age of 50 before increasing it to £600 a month until the age of 65, they would have a pot worth almost £737,000.

If that same 25-year-old started with £500 a month until they reach the age of 35, and then increased the contribution to £750 a month until the age of 50, before ramping it up again to £1,000 a month for the final 15 years of their employment, they would have a pot worth £1.3m – far in excess of the lifetime allowance.

Our examples involve starting early, paying in consistently and not taking any career breaks – which is not realistic for most individuals.

Many people will end up with breaks in their pension savings, such as when they move jobs, take a career break or move to being self-employed. However, it’s worth noting that the figures in our earlier examples don’t include any employer contributions – meaning anything your company pays into your pension is on top of these calculations.

STARTING A PENSION IN YOUR THIRTIES OR FORTIES

Let’s assume someone isn’t such an early starter and instead only starts a pension when they are 35 years old, assuming the same basic-rate tax relief and 5% a year investment growth.

If they paid in £500 a month until they reach the age of 45, and then pay in £750 a month until they reach the age of 60, before ramping up to £1,000 a month for the final five years before retirement, they will have just over £675,000 in their pension pot at age 65 – a very respectable amount.

The big difference with saving earlier is that you have far more time for the money you put away in the early years to benefit from investment growth and from the magic of compounding – which effectively gives you returns on top of your returns.

If you wait until the age of 40 before you open your pension, and put £500 a month in until you turn 50 and then up it to £750 a month until you reach 65, you’ll have a pot worth almost £461,000 by retirement, assuming basic-rate tax relief and 5% annual growth.

YOUR TAX BAND MATTERS

Higher and additional-rate taxpayers will find they can hit a larger pension pot quicker as they’ll benefit from a larger slug of Government tax relief. While basic-rate taxpayers get a 20% boost to their money, higher-rate payers get a 40% boost and additional-rate payers a 45% boost.

In the same example of someone starting a pension at 35 and paying in the same monthly amounts as above, if they were a higher-rate taxpayer they’d see that £675,000 pot at age 65 become £1.06m. This is because their pot has effectively got a 20% additional boost each year.

There are two ways you can access this additional tax relief: either your company uses a salary sacrifice for you contributions, meaning your pension payment comes out before tax is charged, or you can reclaim the additional tax relief through your annual tax return.

If you do the latter you’ll need to pay that tax rebate into your pension pot for your figures to tally with the above calculations.

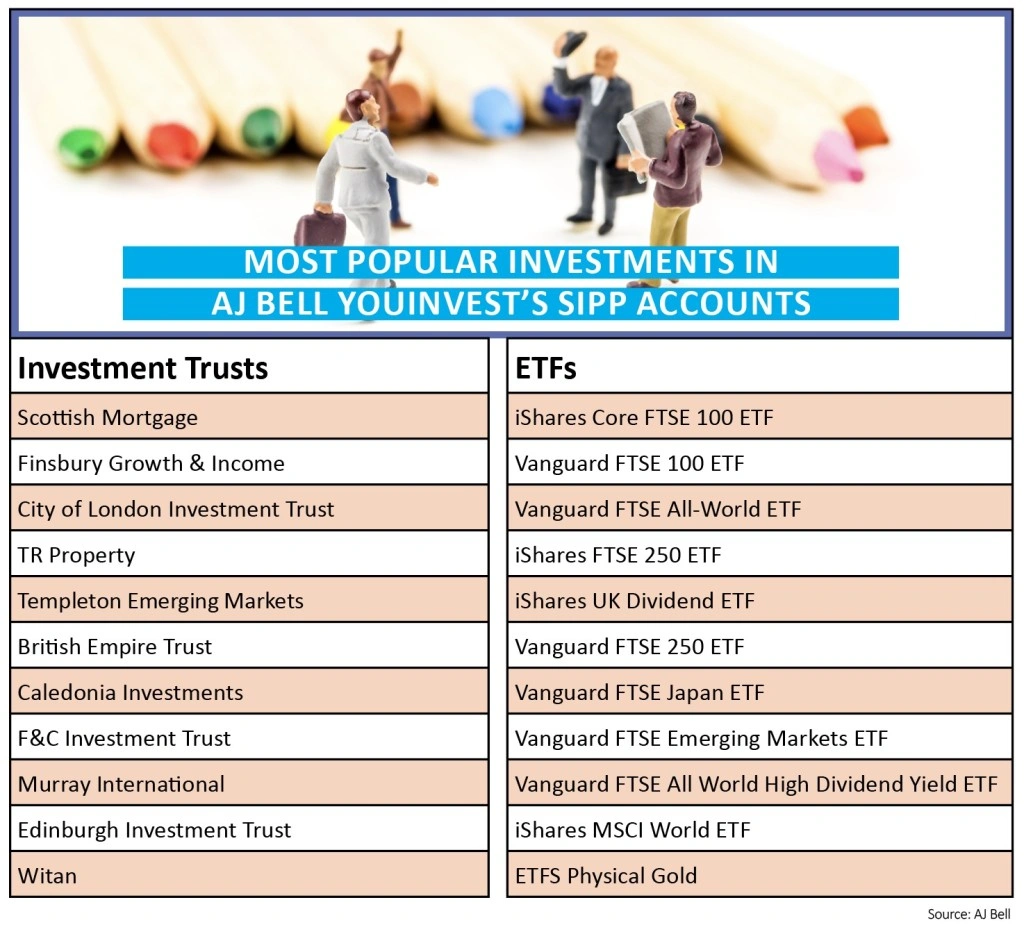

WHAT DO PEOPLE INVEST IN?

The most popular funds in AJ Bell Youinvest’s self-invested personal pensions (SIPPs) are a spread across global stock market funds and a few more specialist areas.

Popular funds such as Fundsmith Equity (B41YBW7) and Lindsell Train Global Equity (B3NS4D2) feature heavily in customer SIPP accounts. Also popular are Vanguard’s LifeStrategy funds, which are multi-asset funds that invest across a range of different asset classes and countries, with each fund having a different amount in the stock market.

For funds more focused on specific areas stalwart funds such as Stewart Investment Asia Pacific Leaders (3387476) and Liontrust Special Situations (B57H4F1) feature in many portfolios.

The most popular investment trusts are also globally-focused including Scottish Mortgage (SMT). And SIPP customers have been drawn to blue chip shares including Royal Dutch Shell (RDSB).

HOW SHOULD YOUR INVESTMENT STRATEGY CHANGE AS YOU NEAR RETIREMENT?

Previously most people had to use their pension pot to buy an annuity – which is an insurance contract that secures you a set income for life. However, new rules in 2015 meant that people were no longer obliged to buy an annuity and pensions were more flexible. They could keep the money invested and draw an income off it every year, or take a lump sum as and when they needed the money.

This meant that the previous investment strategy for pensions was turned on its head.

For those building up to buy an annuity at age 65, for example, historically most would gradually dial down the risk of their pension pot as they neared this date. They would gradually move from a portfolio heavily focused on shares to one more focused on bonds and cash.

The intention was that by moving out of stock market investments, which can be more volatile, those nearing retirement would avoid a large stock market fall wiping out a large chunk of their pension pot just as they were coming to retire.

By moving into bonds and cash you were less likely to see this volatility and so you weren’t at the mercy of large market movements.

LIFESTYLING YOUR PORTFOLIO

This approach led to the launch of a number of so-called ‘target date’ funds. These pinpoint the year that you plan to retire and automatically dial down the risk level of your pension pot as you come nearer to retirement.

Typically these funds switch from higher risk investments, such as emerging market stocks, into developed country’s stock markets. Then they sell stock market investments for bonds, cash and maybe gold. Taking this approach is still sensible if you plan to buy an annuity with your pension pot.

However, now many people keep their money invested and move into drawdown, they don’t necessarily need to reduce the risk to such an extent in their pension portfolio.

STAYING INVESTED IN RETIREMENT

If you’re planning to draw an income off your pension pot throughout your retirement, it could be left invested for another 20 or even 30 years. This means you need your pot to continue growing, and so you’ll likely want to keep it invested in stock markets and higher risk assets.

However, because you’re focused on drawing an income off your pot you may want to switch your investments into ones focused on generating yield, rather than just on capital growth.

For some funds this might simply be a case of switching from the ‘accumulation’ share class into the ‘income’ share class, which will automatically pay out any income rather than reinvesting it. Otherwise you might need to reassess what you’re invested in and focus on income-generating stocks and funds.

EIGHT PENSION RULES

1. If you’re a UK resident under the age of 75, you can contribute to your pension as much as you earn and you will receive tax relief on your contributions.

2. Even if you don’t earn any money in a year you can contribute £3,600, including tax relief, each year. This means children can have pensions too.

3. Higher and top-rate taxpayers can claim back the additional tax they have paid through their tax return.

4. A pension annual allowance applies. For most people this is £40,000 but if you have income over £150,000 your annual allowance is tapered down from £40,000. Once you access your pension your annual allowance may drop to £4,000.

5. If your total pension contributions, including any contributions your employer makes, exceed your annual allowance you will be subject to a tax charge, known as the annual allowance charge.

6. The lifetime allowance for 2018/19 is £1,030,000. When you access your pension, you ‘crystallise’ a portion of it – the amount you crystallise is deducted from your remaining lifetime allowance. If you reach age 75 and haven’t accessed all of your pension, the amount you are yet to access will be tested against your remaining lifetime allowance. If it’s more than £1,030,000, you will face the lifetime allowance charge. The charge is 55% if you take the excess as a lump sum or 25% if you take it as income.

7. You can use all or part of your pot to buy a lifetime annuity, which is a type of insurance contract that will pay an income until the day you die. You choose whether the level of payment will stay the same, rise with inflation, or drop at a later point in time, and you can also have an annuity that will pay your spouse an income after you die if you wish.

8. Drawdown is where your pension remains invested while you take an income from it. With flexi-access drawdown you are able to take as much income as you want, so you can choose to take payments monthly, quarterly, bi-annually or annually, or you can take a one-off payment.

DISCLAIMER:

AJ Bell is referenced in this article as being one of the most popular holdings among AJ Bell Youinvest’s SIPP customers. AJ Bell is the owner and publisher of Shares. Laura Suter and Daniel Coatsworth (who wrote and edited this article, respectively) own shares in AJ Bell.

Laura Suter also has a personal investment in Fundsmith Equity, Vanguard Life Strategy, Scottish Mortgage, Caledonia, Lloyds and Vanguard FTSE 250 ETF and Daniel Coatsworth has a personal investment in Fundsmith Equity referenced in this article.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.