Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCan expensive shares ever offer good value?

As investors we’re regularly told to buy low and sell high in terms of valuation. This line of thought often leaves people feeling nervous about buying shares on higher ratings, especially when market exuberance is in short supply.

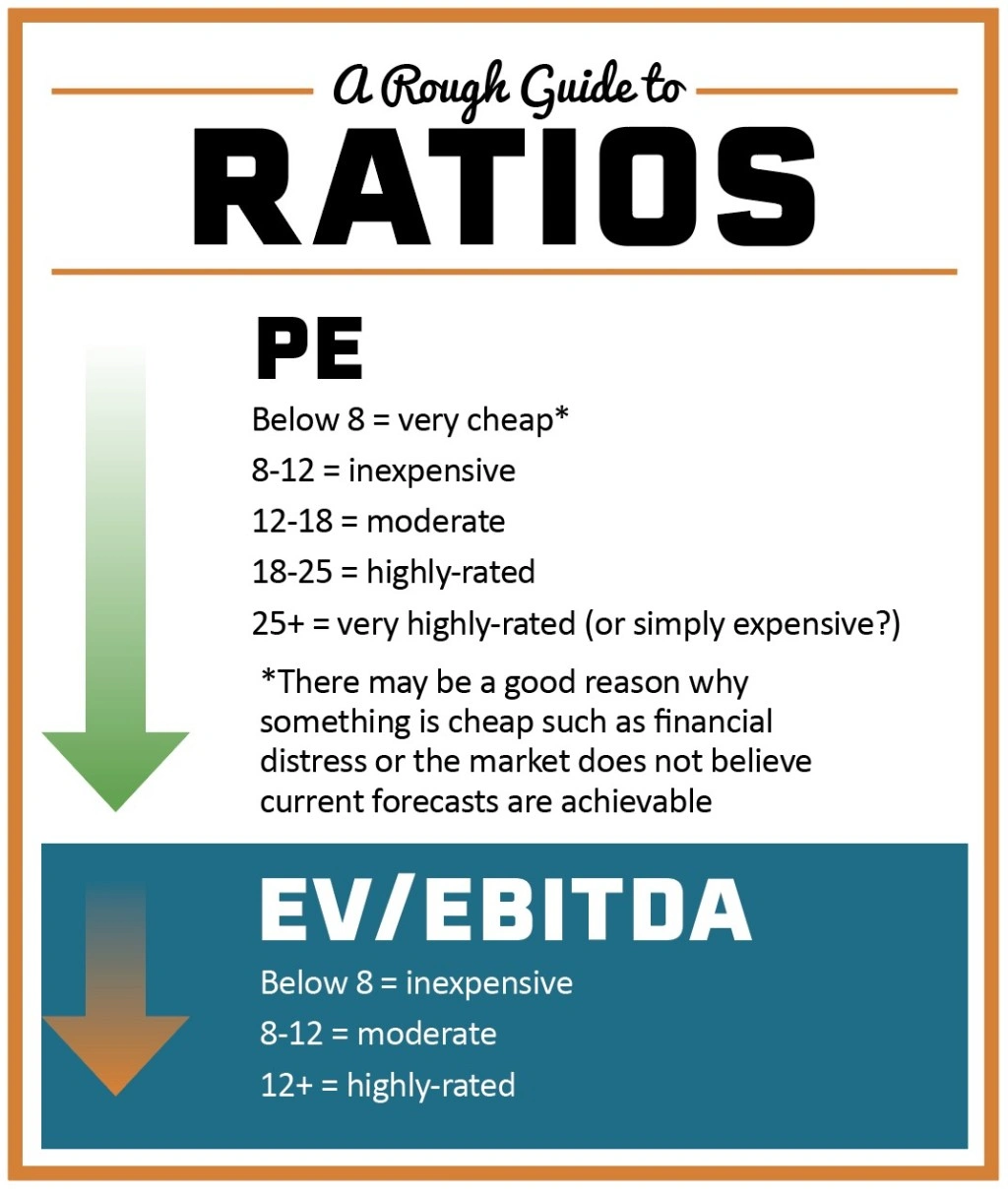

For many investors, buying stocks on a price-to-earnings (PE) multiple in the high teens would be enough to cause a sweat. Paying more than 20 or 30-times might even prompt observers to question if the investor was delirious.

There is solid reasoning behind the buy low/sell high way of thinking. Logic suggests there should be more upside potential from shares on lower PE ratios because as a company’s trading performance improves, the stock can enjoy the double-whammy of rising forecasts and an increased stock rating.

For example, a share priced at 100p and which is expected to produce 10p earnings per share would trade on a PE ratio of 10.

Let’s assume business is going well, prompting analysts to increase their earnings forecast to 11p and the market is happy to pay a higher PE ratio of 11-times for the stock because of the stronger earnings outlook. That means the shares would trade at 121p which equates to a 21% increase on a 10% rise in earnings forecasts and stock rating.

THE RISKS OF OWNING STOCKS ON A HIGH PE

Doing the maths on a higher-rated stock, you can see how they can be punished to a much greater extent than the level of earnings downgrades.

We will now use the example of a stock trading at 500p. It is expected to earn 20p per share and it is trading on a high PE ratio of 25-times.

The company goes through a tough patch which leads earnings per share forecasts to be downgraded by 10% to 18p. Importantly, the market is no longer prepared to pay a premium rating for the stock so it would be feasible to suggest the PE drops to 17-times.

If we multiply 18 by 17 we get a share price of 306p, which equates to a 39% share price decline on a 10% cut to earnings.

TAKING A LONG-TERM VIEW

You may conclude from this example that buying stocks on a high PE ratio is a bad thing. That isn’t necessarily the correct answer.

A lot of investors are happy to pay a high rating for a stock if it has a good track record of solid earnings growth and/or it has a very attractive outlook in terms of potential for market share gains or accelerated earnings growth.

Some stocks can consistently trade on high valuations because they are premium businesses. As with all investments you need to look at them on a case-by-case basis.

‘For us, what matters is the growth of future cash flows on a probability-adjusted basis,’ says James Budden, director of marketing and distribution at fund management firm Baillie Gifford, the brains behind the popular Scottish Mortgage Investment Trust (SMT).

‘Put another way it is all about valuing the potential size of the opportunity rather than focusing on earnings relative to the value of a company or its peers at one moment in time.’

This approach goes some way to explain why some of the most expensive-looking stocks on a PE basis are among the best performers.

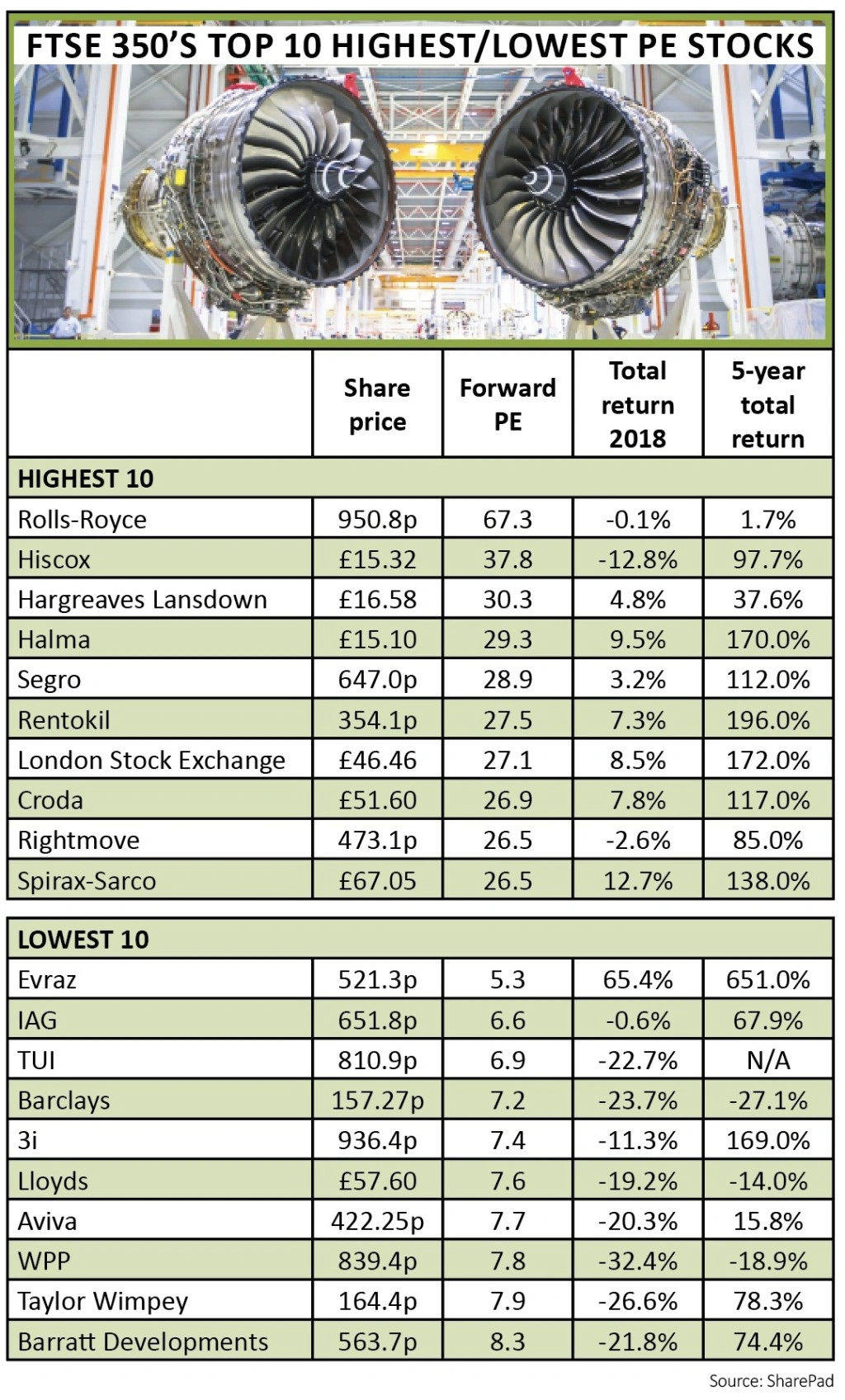

Companies such health and safety kit manufacturer Halma (HLMA), credit checking agency Experian (EXPN), science equipment maker Renishaw (RSW) and property portal Rightmove (RMV) have a combined average total return record of more than 126% over the past five years.

High PEs are often a natural consequence of companies capable of keeping on growing over the longer-term, says David Stevenson, co-manager of TB Amati UK Smaller Companies Fund (B2NG4R3), who adds that premium share price ratings can imply a quality business.

‘For example, five years ago Halma was trading on a PE of about 19-times – it’s now about 30.’ The stock has delivered total returns of 170% since 2014.

A ‘PRIME’ EXAMPLE

Online shopping giant Amazon is perhaps the ‘prime’ example of a stock that has historically traded on a high earnings multiple and whose share price kept going higher.

The share price stood at about $50 in 2003 when the retailer was just starting to make a profit. That implied a mind-boggling PE ratio of approximately 130.

It would have put the stock on many investors’ bargepole list for valuation reasons. That would have been a mistake in hindsight.

Amazon’s earnings have gone from $5.26bn revenue and $40m net income in 2003 to $232.9bn revenue and $10bn net income in 2018.

The stock currently changes hands at $1,614. Amazon exceeded $2,000 per share last year, becoming only the second trillion dollar company in history (Apple got their first).

The emergence of structural growth drivers and disruptive business models using the internet create huge opportunities for asset-light businesses, ones that people will pay more for, according to Stevenson.

Structural growth refers to dynamic industries that do not rely on traditional economic cycles, things like online shopping, cyber security, cloud applications, data analysis, healthcare, and the regulation and compliance that modern industry requires.

The real value is in compounding total returns over years, concludes Stevenson.

How PE can reflect growth and share price returns

Let’s run some imaginary numbers. Meet Racey plc and Steady plc, hypothetical businesses whose share prices are both 100p. Racey trades on a PE of 25. It is expected to grow earnings at around 15% a year over the next five years. Steady’s stock comes with a fair expectation of 7% annual earnings growth and changes hands on a PE of 15.

Run the numbers, presuming the PEs remain the same, and the relative share price performances would be very different.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- BHP, Royal Bank of Scotland, Reckitt Benckiser and other news

- Retail sales figures return to form in January

- Eyes on March update as dividend doubts beset SSE

- Global dividends expected to grow by 5.1% in 2019

- Is HSBC’s 6% yield enough compensation for disappointing results?

- Is the US about to deliver a growth shock?