Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy are investment trusts ditching performance fees and is it a smart move?

Should fund managers really need any extra incentive to deliver for investors given they are already being paid a fee to do their job?

Until recently it was commonplace for the managers of investment trusts to receive a performance fee on top of their management fee if they exceeded a specified level of return.

Increasingly, this structure is being abandoned by trusts, though around a third of equity-focused investment trusts still use performance fees according to stockbroker Numis.

We now explore why they are slowly being phased out and whether there is a danger this move will drive talent out of the investment

trust space.

WHAT ARE PERFORMANCE FEES?

All investment trusts and actively-managed funds charge a fee to pay the professionals whose job it is to manage the portfolio. Typically, this will be expressed as a percentage of the trust’s total net asset value (NAV).

Some funds will operate a tiered fee structure where they charge a certain amount up to a threshold of net assets and then less on assets over this threshold to share with investors the benefits from economies of scale.

The difference with some investment trusts is that they will also impose a performance fee on top, assuming the manager beats certain targets. This might include delivering a defined level of absolute return or doing better than a particular benchmark.

Winterflood Securities’ investment trust team observe: ‘Performance fees have long been a differentiator of investment trusts as it is difficult historically to apply such fee arrangements on open-ended funds (unit trusts and Oeics).

‘However, performance fees remain controversial with some investors, while others point to the additional complexities they can

bring to the investment trust structure.’

A performance fee means it can be difficult to make like-for-like comparisons on fees with different types of funds investing in similar areas such as open-ended funds or exchange-traded funds.

AN ACCELERATING TREND

The asset management space is highly competitive and the trend towards getting rid of performance fees reflects a wider drive on the part of trusts and their boards to reduce charges and boost their attractiveness to investors.

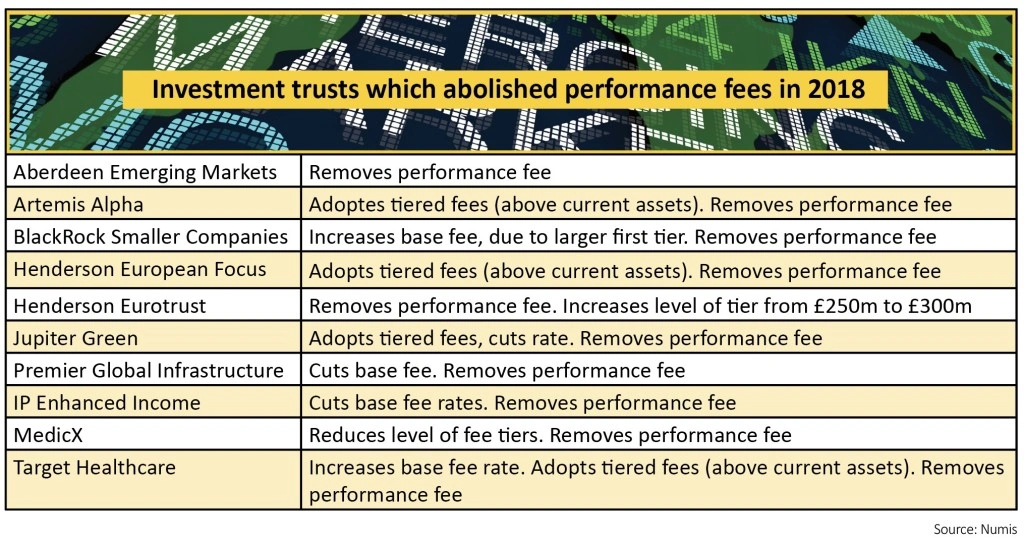

Figures from Numis show 27 investment trusts made changes to their performance fees in 2018 with 10 abandoning them altogether compared with five in 2017. In total, 56 investment trusts have removed performance fees since 2012.

Some of the names ditching performance fees entirely had not paid them for several years anyway.

This applies to Aberdeen Emerging Markets (AEMC) and Target Healthcare (THRL). The latter has subsequently increased its base fees – something BlackRock Smaller Companies (BRSC) has done as well.

Where trusts have opted for evolution rather than revolution by tweaking their performance fees there have been different approaches.

In some cases, the rate has simply been reduced, as seen with Martin Currie Global (MNP) and German residential property investor Phoenix Spree Deutschland (PSDL).

Others have introduced variable fees, which means the amount fund managers get paid depends on the extent to which they have beaten the benchmark (with an upper or lower limit).

This is similar to the way some estate agents operate with their fee in percentage terms dependent on the price (or return they achieve) when selling your property.

For example, Manchester & London (MNL), rather than charging 0.5% per year as it did previously, will charge either 0.25% or 0.75% depending on whether it has beaten its benchmark over the previous three years.

PAID PURELY ON PERFORMANCE

Managers of three investment trusts are only paid in performance fees. Numis argues Woodford Patient Capital’s (WPCT) fee structure is ‘highly favourable’

to shareholders as it requires the trust to deliver returns of more than 10% per year before making any charges.

Of the other two – Aurora (ARR) and Ashoka India Equity (AIE) – the stockbroker believes the former’s fee structure is potentially generous given the contrast between a focused portfolio of between 15 and 20 stocks and a very broad benchmark in the FTSE All-Share.

WHAT ARE THE DOWNSIDES?

While it is easy to see the arguments for ditching performance fees, namely the need to make trusts a simpler proposition and more shareholder friendly, there are potential downsides.

Winterflood says: ‘We have growing concerns that the relentless pressure on fees is leading to bad outcomes.’

It cites the example of loan fund Invesco Perpetual Enhanced Income (IPE) where a dispute linked to corporate governance and fees saw fund manager Invesco Perpetual resign in April 2018.

Invesco then returned in June 2018 with reduced management fees and the abolition of its performance fee – with the price of its climb-down apparently being the departure of chairman Donald Adamson.

‘While we would acknowledge that boards have a duty to look after the interests of investors, of which negotiating fees is an important element, we believe that consideration should be made as to the wider picture and how a fund’s investment manager is incentivised.

‘In our opinion, performance should be the key consideration rather than fostering a motivation to gather assets.’

THE EXCEPTIONS TO THE RULE

Not every trust is following the trend as William Heathcoat Amory, head of investment trust research at Kepler, observes: ‘Jupiter European Opportunities (JEO) has a performance fee, which was triggered during the 2018 financial year, equivalent to c1.4% of net asset value (the maximum performance-related payout is 5% of NAV).

‘The board had a review of the arrangements, and in contrast to many other trusts, decided to keep the performance fee, which some agreed with, but was met with dismay by others.

‘We believe that it is net of fees performance that counts, and Alexander Darwall has proved himself time and time again an exceptional manager. As such, we believe he deserves an exceptional fee.’

This focus on performance net of fees is a key point. Research from tracker fund specialist Vanguard suggests if you paid zero fees and

invested £100,000 then assuming 6% growth over a 25-year period you would end up with £430,000. If you paid 2% every year in costs, you’d only end up with £260,000.

However, as Heathcoat Amory observes, there is a case for paying up if you are getting a premium performance. He also notes that in many cases the presence of a performance fee is balanced out by a lower base fee. Should this not be the case then he says it is fair to demand change.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- BHP, Royal Bank of Scotland, Reckitt Benckiser and other news

- Retail sales figures return to form in January

- Eyes on March update as dividend doubts beset SSE

- Global dividends expected to grow by 5.1% in 2019

- Is HSBC’s 6% yield enough compensation for disappointing results?

- Is the US about to deliver a growth shock?