Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSix reasons to be excited about Cineworld’s shares

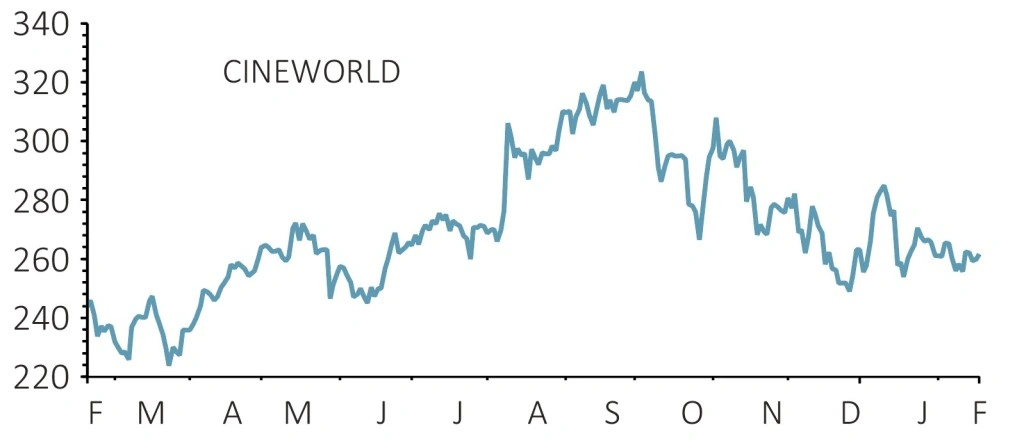

Cineworld (CINE) 260.6p

Loss to date: 1.4%

Original entry point: Buy at 264.4p, 3 May 2018

Shares in Cineworld (CINE) are currently sitting just below the point at which we said to buy last May. This is frustrating as the business has issued plenty of good news including a reassuring trading update last month.

Investment bank Berenberg says there are six reasons why the shares deserve another look. These are: a refurbishment programme helping to make sites more attractive; synergies from buying Regal Entertainment in the US; hopes that high levels of debt will be rapidly paid down; a strong movie slate in 2019; ongoing growth in the cinema market; and a cheap valuation.

Cineworld currently trades on 7.4 times 2019’s forecast EV/EBITDA (enterprise value-to-earnings before interest, tax, depreciation and amortisation), which is the lower end of its historical range according to Berenberg.

The shares are cheap because the market is primarily worried about the excessive borrowing levels – net debt was forecast to be $3.79bn at the end of 2018, more than four times EBITDA.

Ongoing reduction in debt will theoretically make the equity worth more, thereby driving a re-rating in the share price.

SHARES SAYS: This is a great business yet the investment case remains high-risk due to the elevated debt levels. Anyone comfortable with the risks should buy the shares as a long-term holding.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- BHP, Royal Bank of Scotland, Reckitt Benckiser and other news

- Retail sales figures return to form in January

- Eyes on March update as dividend doubts beset SSE

- Global dividends expected to grow by 5.1% in 2019

- Is HSBC’s 6% yield enough compensation for disappointing results?

- Is the US about to deliver a growth shock?