Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy investors need to start watching the race to the White House

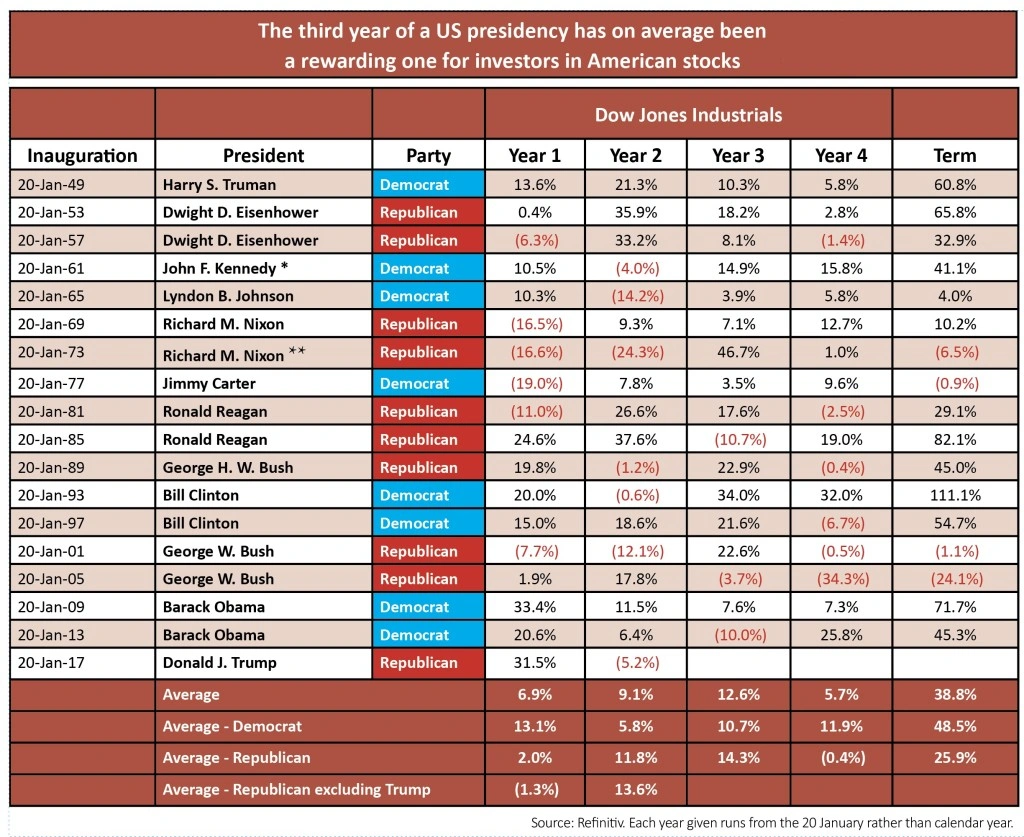

The race to the November 2020 presidential election and the keys to the White House on 20 January 2021 is well and truly on. Investors in US equities will be hoping that history is on their side, as the third year of a president’s term has, on average, been the best one for returns from American stocks.

Since 1945, the Dow Jones Industrials index has fallen just three times in the third year of 17 different presidential third terms, defined as running from the inauguration date of 20 January, and generated an average capital return of 12.6%.

It is hard to say quite why the third year of a presidency should be the best one from the perspective of stock markets.

It may simply be that the prior year’s mid-term elections fire the starting gun on the next race to the White House.

As such the incumbent President Donald Trump will be starting to think in terms of polls and voter-friendly policies and may therefore be inclined to run more growth-oriented initiatives.

And as someone who seems to partly measure the success of his presidency by how the US stock market does, Trump will be watching the major indices keenly.

He will also be keeping a close eye on the identity of his Democratic Party opponent, presuming that Trump decides to run and is given the opportunity to do so.

DEMOCRATIC DILEMMA

The nineteenth-century presidents Polk, Buchanan and Hayes chose not to run for a second term, while Tyler and Pierce failed to

win their party’s nomination having won an election and served for four years, so nothing is impossible.

Some Republicans are already pressing for Trump’s removal from the party ticket – to be decided at August 2020’s national convention – not least because special counsel Robert Mueller’s inquiry into allegations of Russian influence over the 2016 presidential election will reach its conclusion at some stage this year.

Despite hints from former senator Bob Corker and former governor (and twice-defeated party candidate) John Kasich that they may stand against Trump, the Democratic Party picture is much murkier than the Republican one.

Nine Democrats are already officially in the running for their party’s nomination, with surely many more to follow.

Since Hillary Clinton’s surprise 2016 defeat, the party has wrestled with whether to go further to the left or try to grab the centre ground in its bid to defeat Trump and the Republicans.

The current runners cover a wide spectrum, ranging from centrist Minnesotan Amy Klobuchar, to the established left-wingers Elizabeth Warren, Kamala Harris and Julian Castro.

The eventual winner will be declared at a yet-to-be-decided venue in July next year.

MONETARY POLICY ISSUES

As the race heats up, US equity and bond markets will start to pay more attention, especially as the Democrats and Republicans seem incapable of agreeing upon almost as much as nothing.

Like him or loathe him, Trump has influenced markets, at least in the short term, via his tax cuts, trade policy, pressure on firms to build capacity and hire in the US, and attempted healthcare reforms, to name just four areas.

Whether he can match the US Federal Reserve’s bang for its (trillions of) bucks can be debated.

It is barely three months since this column idly speculated what could persuade the US central bank to change its mind on tightening monetary policy and already chair Jay Powell seems to have put further rate rises on hold and raised the prospect of not just halting quantitative tightening but adding more quantitative easing, should circumstances demand it.

Financial markets now put an 83% chance on the Fed leaving headline borrowing costs unchanged at 2.5% for the rest of 2019 and believe there is a greater likelihood of a cut than an increase.

That about-turn is currently lifting stock and bond prices and the potential Democrat response to President Trump’s policies could prove just as influential.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- BHP, Royal Bank of Scotland, Reckitt Benckiser and other news

- Retail sales figures return to form in January

- Eyes on March update as dividend doubts beset SSE

- Global dividends expected to grow by 5.1% in 2019

- Is HSBC’s 6% yield enough compensation for disappointing results?

- Is the US about to deliver a growth shock?