Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBeat the bank: how to get a better return on your cash

We’re a nation of cash savers, with Brits putting more than 72% of their ISA money in cash last year, rather than investing it.

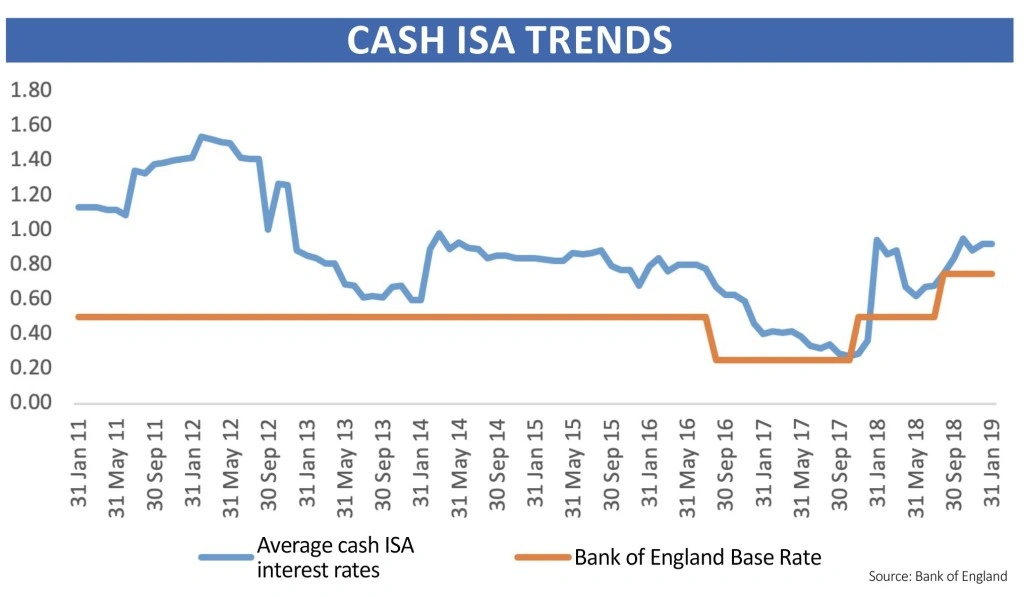

However, with interest rates having hit record lows over the past decade these savers are earning miserly returns on their pots. The Bank of England’s base rate is currently 0.75% and the average cash ISA rate is 0.92% – far lower than the current rate of inflation, which sits at around 2%.

It is important to have a good chunk of cash put to one side to cover any emergency issues such as a broken boiler, a broken-down car or as support if you lose your job. Therefore finding the best return on your cash is equally as important as the hard work many people put into researching the best shares or funds for long-term investing.

This article will run through the available options and also show you how to beat the banks’ low savings rates with a range of lower-risk investment options.

WHERE CAN I GET THE MOST BANG FOR MY BUCK?

The best deal you can get from a mainstream lender on an instant access variable rate cash ISA is 1.45% from Virgin Money, and you can transfer in an existing cash ISA.

You’re only allowed to make two withdrawals a year, so it’s not suited to someone who is likely to need regular access to the money. The account can also only be opened online. Someone who is able to save the full £20,000 ISA allowance will earn £290 in interest in a year.

If you want to go into a branch to open an account the best rate you’ll get is 1.41% from Yorkshire Building Society, which has branches around the UK. You can transfer other ISAs into this account but you can only make one withdrawal a year – making it even more limited than the Virgin account.

Elsewhere, Al Rayan Bank will pay 1.36% and has branches in a number of big cities around the UK. However, this bank is run to Islamic law and so this is an expected rate of return rather than a guaranteed interest rate.

The top cash ISA rate you’ll get with a high street bank is 0.9% with Metro Bank, which you can open online or in branch, or you can get 0.6% with Barclays, Santander, TSB and Halifax – which is £120 on £20,000 of savings.

A lot of existing customers of these banks will assume they’re on this rate, but most won’t be. Many of these deals run for a year and then the interest rate plummets to rock-bottom levels, which is why much of our cash is dwindling in accounts paying next to nothing.

For example, HSBC pays just 0.55% as its standard interest rate, while Lloyds pays 0.35% and NatWest pays just 0.2%.

You can lock your money in to earn a bit of extra cash. The top rate you’ll get is 2.3% with Coventry Building Society as long as you’re willing to tie your cash up until the end of November 2023 – so almost five years. A two-year fixed rate with Coventry will get you 1.9%.

NON-ISA ACCOUNTS COULD HAVE BETTER RATES

The introduction of the personal savings allowance has dented the popularity of ISAs. The allowance gives an annual tax-free amount for any interest earned on savings: £1,000 for basic-rate taxpayers or £500 for higher-rate taxpayers. It means that many people are now keeping their money in non-ISA accounts that pay more.

If you’re willing to do this you don’t get that much more on an instant-access savings account – the best is 1.55% with ICICI Bank. But where you can really earn money is with high-interest current accounts.

These often have restrictions on them, whereby a certain amount has to be paid in each month and you have to set up a certain number of direct debits, but if you can be bothered with the small increase in hassle when setting them up, you can earn far more.

For example, both TSB and Nationwide pay 5% interest on their current accounts. With TSB you have to pay in £500 a month and you only earn that interest on up to £1,500. With Nationwide you get the interest on up to £2,500 but you need to pay in £1,000 a month.

FURTHER WAYS TO EARN MORE

Another option is regular savings accounts. These will pay high rates of interest but often only on limited sums, meaning you’ll need to set up quite a few if you have a large sum to put away. They also often require you to set up a current account with the provider too, which increases the hassle factor.

First Direct is currently offering 5% on monthly savings of between £25 and £300. You need to open a First Direct current account, but new customers who switch get £125 joining bonus, which makes it more worth your while. The rules are pretty strict though, and if you miss a monthly deposit the account will be closed and you’ll only earn 0.05% interest.

As there are lots of these accounts available you may wish to open a number of them. As long as you meet the minimum monthly contributions you can earn higher interest rates on larger sums.

This requires a bit of leg-work initially – such as setting up direct debits and opening the accounts – but this effort can really pay off in the long term. Just don’t start the process if you know you don’t have the time or inclination to set it all up correctly and keep track of the money.

WHAT IF I WANT TO TAKE A BIT MORE RISK?

People willing to tie up their money for a few years and take a bit more risk than leaving their money in cash could get a higher return via bond funds.

Usually the rule with investing your cash is to have a minimum period of five years to lock the money away, but this rule could be relaxed a bit for the lower-risk end of the market.

You would use a stocks and shares ISA to make the investment.

One option is short-dated bonds. These are bonds that have less than five years left until they mature, meaning you should get the coupon (the interest payment) for the remaining time until the bond is redeemed and then you get repaid the value of the bond too. Certain funds specialise in this area, says Ryan Hughes, a fund manager at AJ Bell.

‘These funds are sensible, low-risk, cheap and a step up from cash. They’re a good option for those wanting to go up the risk scale, but who want fairly stable and reliable returns,’ he says. ‘The beauty of them is that they also have low costs, partly because they are typically holding the bonds until they mature rather than selling them, so they cut down on transaction costs.’

THREE EXAMPLES OF LOWER-RISK BONDS

Axa Sterling Credit Short Duration Bond (B5L2N22) has an ongoing charges figure of 0.41% and a current yield of 1.42%. On average the bonds held in the fund have around 1.8 years until they mature. The global fund has achieved 1.48% annualised total returns over the past three years, which is the return after charges.

Another example is the Fidelity Short Dated Corporate Bond Fund (BDCG0G2), which has an ongoing charges figure of 0.38% and currently holds bonds with an average of 2.5 years until they mature. The fund has a yield of 4.1% and has achieved 1.42% annualised returns over the past two years (we don’t quote three-year data like the other examples because it hasn’t been going for that length of time).

For those willing take a bit more risk, Royal London Short Duration Global High Yield Fund (B9BQGL2) invests in slightly riskier bonds, but only holds bonds with two years or less until they mature. The fund has an ongoing charges figure of 0.6% and is yielding around 5.18% at the moment. It has achieved 2.49% annualised total return over the past three years.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- BHP, Royal Bank of Scotland, Reckitt Benckiser and other news

- Retail sales figures return to form in January

- Eyes on March update as dividend doubts beset SSE

- Global dividends expected to grow by 5.1% in 2019

- Is HSBC’s 6% yield enough compensation for disappointing results?

- Is the US about to deliver a growth shock?