Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineGrainger boosts private rented exposure after breakthrough acquisition

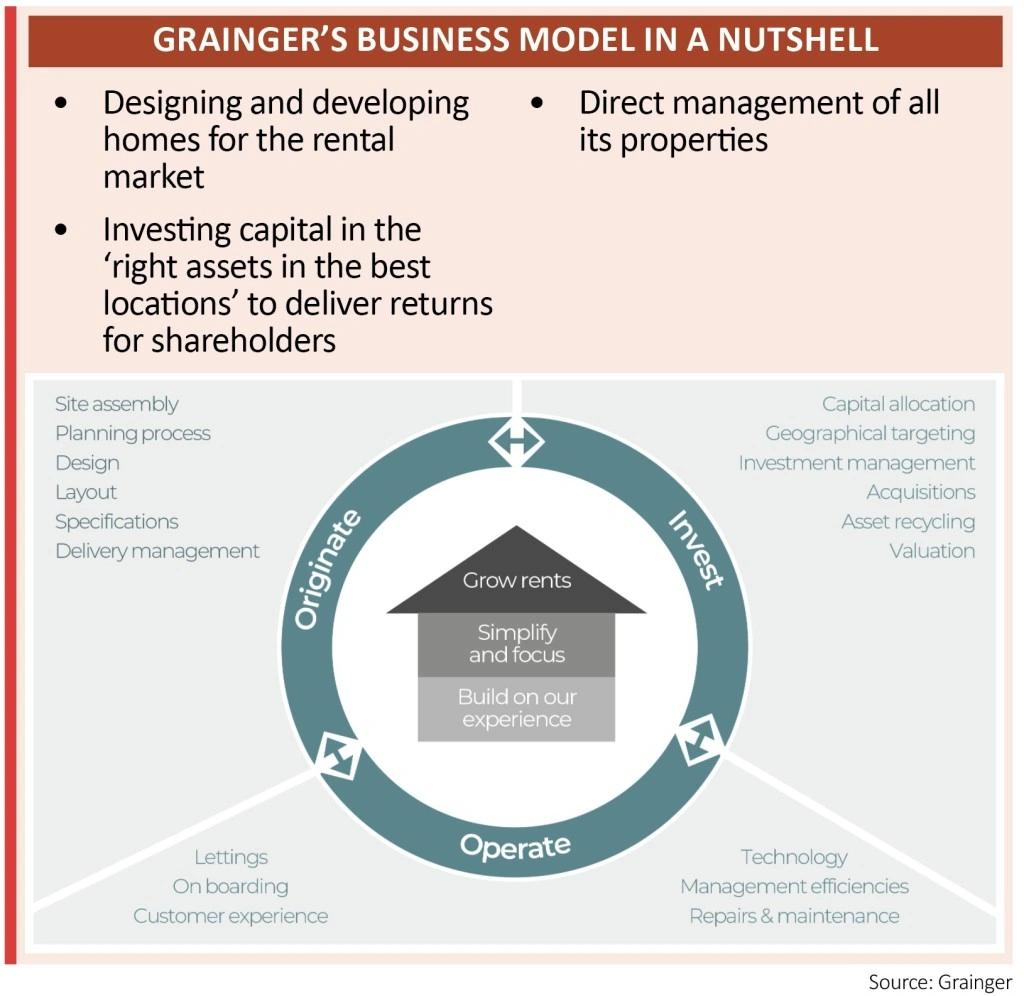

The £396m acquisition by professional residential landlord Grainger (GRI) of a portfolio of homes in London and the South East will accelerate its transition from an historic focus on regulated tenancies to the private rented sector.

It also brings forward the company’s likely conversion to real estate investment trust (REIT) status.

WHAT IS IT BUYING?

Funded by a £346.7m rights issue at 178p, Grainger is taking full ownership of a portfolio of 1,700 homes, which it had previously been managing for its joint venture partner APG. Before this deal APG owned 75% with Grainger having 25%. The assets are expected to generate annual rental income of £32.5m.

The acquisition grows the value of Grainger’s private rented sector pipeline to £1.37bn from a previous target of £850m by 2020.

The private rented sector retains strong fundamentals as property expert Savills commented in its 2018 outlook. ‘Despite extra funding for Help to Buy, demand for private rented properties will continue to increase,’ it said. ‘Together with the ongoing undersupply of affordable housing, this should underpin rental demand across a range of income groups.’

Put simply, demand for housing is outstripping supply and fewer people are able to get on the property ladder.

The number of households in this sector is expected to increase from 4.7m to 7.2m by 2025 according to Grainger, citing a number of sources. This is also a highly fragmented market with 98% of all landlords in the UK owning less than 10 properties.

Average weekly rent in the acquired portfolio (known as GRIP) is 8% lower in London and 24% lower in the South East than the market average, supporting an occupancy rate of 95% and rental growth of 3% for the year to 30 June 2018.

AN ‘EXCEPTIONAL’ OPPORTUNITY

Chief executive Helen Gordon tells Shares: ‘It is rare or even exceptional you get to buy something you have been managing for more than five years and where you know all the wrinkles.

‘We have been working on this deal for over a year, having previously done all the heavy lifting of growing the portfolio and watching APG get 75% of the benefits.’

This may explain the willingness to acquire the assets at a 4.9% gross yield which is lower than the yield on the existing portfolio which stockbroker Peel Hunt puts at between 5% and 6%.

Gordon adds that the transaction ‘completely reverses the shape and nature of the business’ which is a key target for the management team who took the helm in early 2016. Exposure to the private rented sector will increase to almost 60% from under 50% according to Peel Hunt.

Grainger hopes to realise cost efficiencies from its expanded portfolio with a target of reducing the ‘gross to net rental leakage’, or how much of its rental income is lost to costs, from 32% to 26% across the group as a whole.

Its previous weighting towards regulated tenancies prevented the group from becoming a REIT – a move Mike Prew, real estate expert at investment bank Jefferies, says could now be brought forward from 2025 or 2026, to 2022 or 2023.

REIT status comes with tax advantages and would see a greater proportion of rental income paid out as dividends to shareholders.

WHAT IS THE COMPANY’S BACKGROUND?

Grainger was established in Newcastle in 1912 to manage assets in the regulated tenant market. Lettings which began before January 1989 typically fall into this category, so these are historic assets with ageing tenants for the most part.

Ultimately this is a sector where companies would buy a residential property at a discount and then receive below-market levels of rent (linked to inflation) from the tenant, who then lived in the property for the rest of their life.

Once a property is returned to the company it is sold at market prices, thereby unlocking the capital value. Grainger calls this a reversionary surplus and it uses these funds to reinvest into higher yielding new private rented sector homes. This surplus equated to 66p per share in the September 2018 financial year.

The resilient income from regulated tenancies was beneficial to the company through the 2007/8 downturn and Arden analyst Kunal Walia comments: ‘(It) provides an interesting proposition for investors looking to maintain a defensive play while capturing the strong fundamental growth prospects within the UK private rented sector market.’

Grainger’s results for the 12 months to 30 September 2018 showed group revenue rising from £264.7m to £270.7m while the firm’s operating profit increased by 30% to £123m. This increase in profit was supported by several asset disposals and Gordon says the company takes a ‘disciplined’ approach to asset recycling.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.