Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSilver is looking incredibly cheap compared to gold

Precious metals have been widely out of favour with investors for some time, but a recent bout of stock market volatility could see them come back into fashion, particularly if the US dollar starts to weaken.

The most talked about metal is gold. It typically does well at times of great uncertainty or fear, because it is seen as a physical store of value and an alternative form of currency for anyone worried about the value of paper currencies.

For that reason, the gold price tends to surge when confidence is at its lowest. Silver, too, typically follows the same course. By far the cheaper option, its price tends to fluctuate more aggressively making the potential for both gains and losses greater.

Gold and silver often move in the opposite direction to the US dollar. They’ve not done well this year because the dollar has been strong. Some experts believe the US dollar could weaken in 2019 which theoretically makes gold and silver worth exploring again.

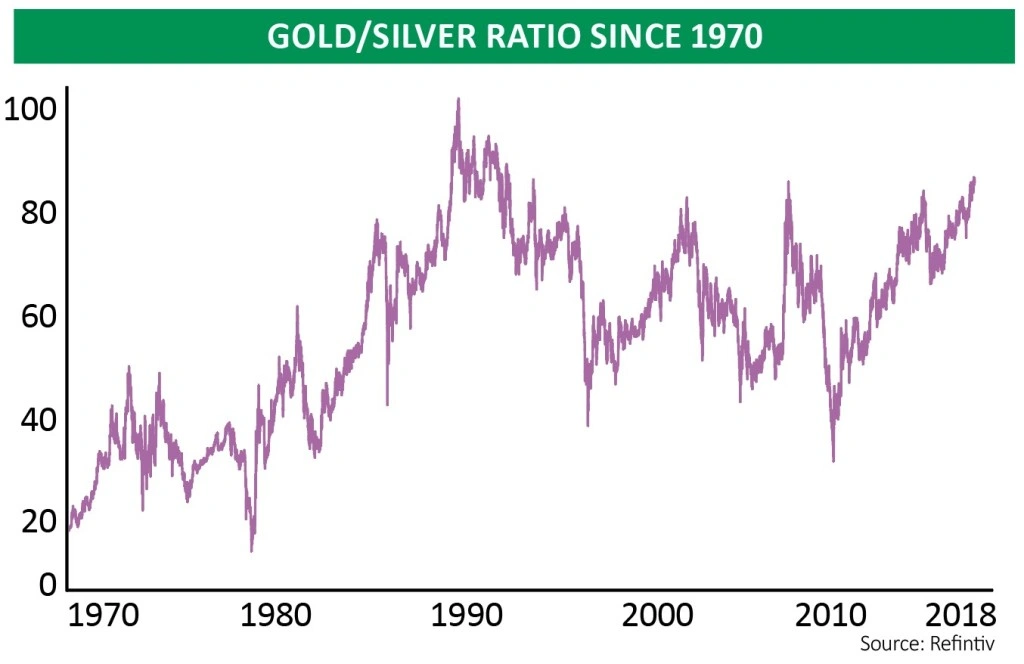

UNDERSTANDING THE GOLD/SILVER RATIO

One of the measures which many precious metal investors watch is the gold/silver ratio. This is the price of an ounce of gold divided by the price of an ounce of silver.

The metric has recently reached a long-term high of 86:1, which means that for every single ounce of gold you could purchase, you could get 86 ounces of silver. Perhaps, unsurprisingly, investors have started to wonder whether this is not a clear sign to buy.

The long-term average, looking at data back to 1970, is 57:1. The ratio has exceeded 70 since April 2017.

Ned Naylor-Leyland, manager of the Merian Gold & Silver (BYVJRB3) fund, says: ‘Like gold, silver is usually seen as a hedge against any loss of purchasing power in paper money. The current gold to silver ratio infers that silver is a value opportunity compared to gold. It is certainly a more volatile version of the yellow metal, which is being accumulated by the world’s central bankers as an apolitical reserve asset.’

UNDERSTANDING PRICE MOVEMENTS

Investing in silver may not be as simple as looking at a mathematical formula. Often, when the ratio has widened to these levels it is because the gold price has surged and then fallen back, rather than because of any specific movements in the silver price.

In the late 1980s, for example, gold surged amid fears of a recession after Black Monday on the stock market and then retreated.

After the financial crisis, precious metals initially lost value as investors sold assets indiscriminately, but they later started to climb as their safe haven status started to shine. For example, between 2009 and mid-2011, silver moved from $10 an ounce to a high of $48 per ounce.

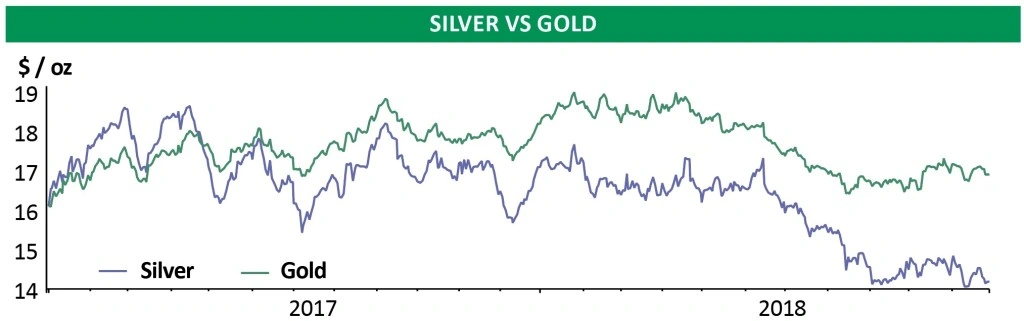

Investors have traditionally increased their purchase of precious metals amid stock market turmoil or when there is political, fiscal or economic fear. But even despite recent trade war rhetoric and the ongoing uncertainties around Brexit, gold has stayed largely steady.

Certainly, in the most recent bout of volatility, fewer investors seem to have been flocking to the yellow metal. Rather than an expected pick-up with so much uncertainty in the air, the gold price has actually fallen over the past year. So too has silver; the metal is currently trading around $14 an ounce, which is 70% lower than levels seen in 2011.

Naylor-Leyland says: ‘Gold and silver have both been out of favour with mainstream investors for some time, but with currency nerves frayed by Brexit, it could be that this is an asset class worth looking at.’

Certainly, investors in precious metals must be prepared to sit tight for the long-term. Investment fund Merian Gold & Silver is down 15.8% over the past year, for example. It invests through mining companies and other funds, with top holdings including Fortuna Silver Mines, which has mines in Peru and Mexico; and Silvercorp Metals, which is focused on China.

Few funds explicitly focus on silver. BlackRock Gold and General (B5ZNJ89) has exposure to the metal through holdings such as Wheaton Precious Metals, but the fund’s primary focus is on gold. It has returned 53.7% over three years and is down 16% over the past year.

Investors can also access the asset through exchange-traded funds such as ETFS Physical Silver ETF (PHAG) which tracks the silver spot price. Its performance highlights the volatility of the metal – it has returned 20.3% over three years but is down 12.7% over the past 12 months.

US-listed iShares MSCI Global Silver Miners ETF tracks an index of silver mining businesses and has returned 61.3% over three years, although it is down 24.8% over the past 12 months.

Examples of London-listed mining companies which produce silver include Fresnillo (FRES) and Hochschild Mining (HOC).

Investors must appreciate that gold and other defensive-like assets aren’t a guaranteed way of making money. Alex Barry, head of UK distribution at asset manager Legg Mason, says: ‘It is understandable that after such a prolonged bull market in equities, investors have once again looked to safe havens such as gold and cash.

‘We understand the need for investors to protect themselves but they must consider the return profile of such assets. Taking gold as a case in point, it has failed to deliver for investors this year and it remains hard to see a catalyst for it to do so.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.