Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

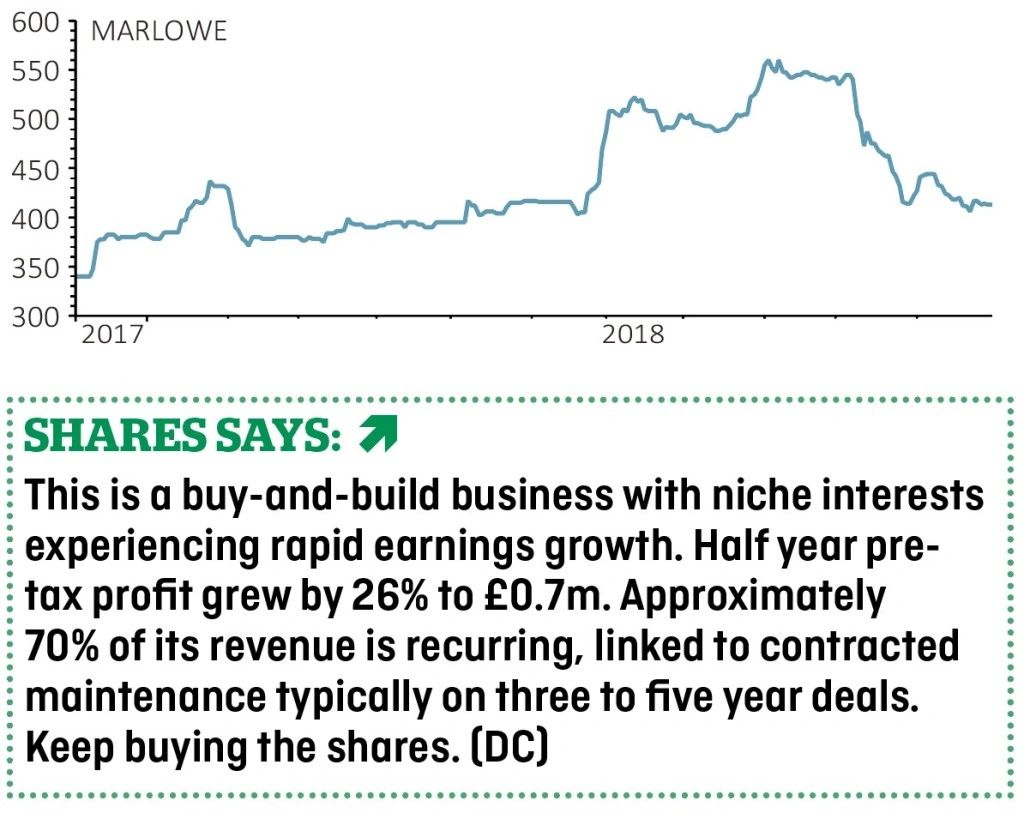

magazineLarge earnings upgrades at Marlowe following strong trading

Marlowe (MRL:AIM) 434p

Gain to date: 1.9%

Original entry point: Buy at 426p, 28 June 2018

The safety expert says full year results will now be better than previous market expectations, thanks to good trading across its business and positive contribution from recent acquisitions.

Stockbroker Cenkos has subsequently upgraded its earnings per share forecast by 18% to 17.9p for the year to March 2019, and by 19% to 20.5p for 2020.

Marlowe’s chief executive Alex Dacre says half-year organic growth was just below 5%, approximately split into 6% for its water division and 4% for its fire division. He believe the company can achieve 7% annual organic growth in the long term via cross-selling and efficiency gains.

He is looking to increase the scale of acquisitions and is targeting deals in the health and safety auditing and inspection market. ‘This is an attractive market underpinned by critical regulation, following similar themes to the rest of our business,’ comments Dacre.

Marlowe’s current focus is installing, testing, inspecting and certifying fire systems to make sure they are working and comply with legislation. It does the same with water and ventilation systems.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.