Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

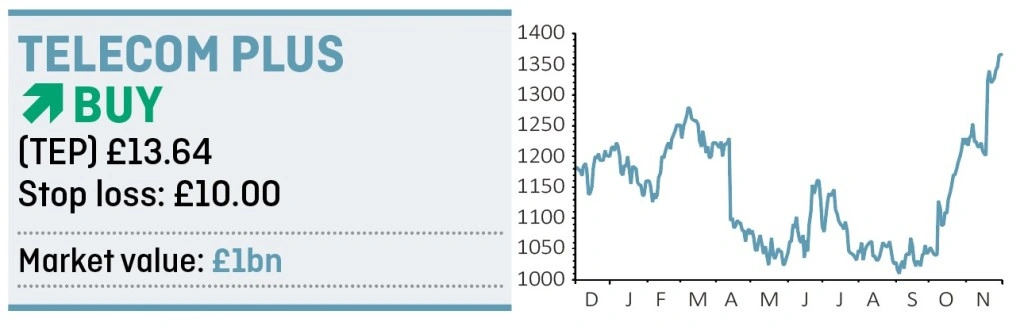

magazineThe outlook for Telecom Plus is very attractive

After several years fighting its corner in a viciously competitive energy market the tide is finally set to turn in favour of multi-services supplier Telecom Plus (TEP).

Trading as Utility Warehouse, the company is Britain’s biggest independent energy supplier (not one of the big six), supplying gas and electricity to more than 621,000 UK homes and businesses.

It also offers home phone, broadband and mobile into a single billing package, and more recently added home insurance to its roster. Furthermore, it has a cashback card that provides discounts on a wide range of third parties offers. More than a fifth of customers (21.8%) take five services or more. Altogether it is currently providing 2.43m services across the UK.

This strategy will eventually be bolstered with plans to extend its services offering. Boiler cover, pet insurance and possibly water supply could feature in the future.

This is good news for shareholders for two distinct reasons. First, it should cap churn well below the industry’s 20% annualised mark. Churn is the measure of customers switching away to a rival, and Telecom Plus’s metric stands at 12%.

Second, it means the company earns better gross profit margins. For example, where energy margins run at around 10%, communication gross profit comes in at more than 40%.

ENERGY PLAYING FIELD LEVELLING OUT

The arrival of Ofgem tariff price caps in January 2019 should blunt the big six energy providers’ ability to use highly profitable standard variable tariffs to fund discounted introductory offers to win customers, a game Telecom Plus has refused to play.

Despite this improving backcloth the company resisted the temptation at half year results (20 November) to raise guidance. That leaves its pre-tax profit steer within the £55m to £60m range, versus £54.3m last full year to 31 March 2018.

That tallies with management’s typically conservative nature but it may equally imply scope to beat those estimates, and see future forecasts raised which would push the share price higher.

The stock has in the past traded close to £19 levels and

we wouldn’t rule out getting back to those levels on a 12 to 18-month basis.

In the meantime, Telecom Plus is a cash generative business that pays out more than 80% of earnings as dividends. Next year’s expected full year dividend of 56.1p per share implies an 85% payout ratio. It also equates to an inflation-beating income yield of 4.1%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.