Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCan stocks fight back after US-China truce?

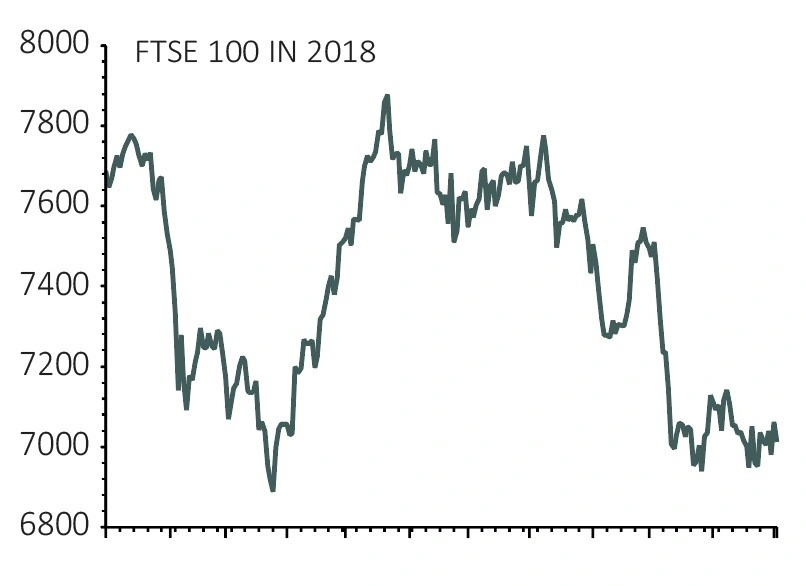

The final quarter of 2018 was shaping up to be a bruising period for investors as stocks drifted in September and then capitulated in October amid a host of economic and geopolitical concerns.

A truce on the trade war between the US and China seems to have been a catalyst for an easing of these concerns and the FTSE 100 is now comfortably back above the 7,000 mark and other major market indices are clawing back some of the ground lost in recent weeks.

In this article we will look at why there has been a stock market recovery and consider if it can be sustained.

WHY HAVE STOCKS BEEN SO VOLATILE IN 2018?

Several factors lie behind the stock market volatility seen in 2018 but the big one has been US interest rates, in particular suggestions that rates could rise faster than the market expects, leading to rising yields on US government debt.

This in turn negatively impacts equities as the income available from relatively lower risk government-issued bonds becomes more attractive than that from higher risk stocks and shares.

As rising yields also reflect higher costs of borrowing, they can be indicative of pressure on business and consumer spending.

Meanwhile political uncertainty created by Brexit and the US mid-term elections, combined with bubbling tensions over trade between the US and China, have added to the pressure on financial markets.

And a sell-off in the technology sector, which has helped fire some of the big gains seen in recent years, has been another factor as investors have become more uncomfortable with the sky-high valuations in this space.

A look at the performance of FTSE 350 sectors from the start of 2018 to the recent low seen on 23 November shows industries with particularly strong exposure to economic conditions have been among the worst performers.

WHAT’S HAPPENED TO MAKE INVESTORS MORE POSITIVE?

Two pieces of news have emerged in the last week to put investors in a sunnier mood.

First on 28 November the head of the US Federal Reserve Jerome Powell said that current interest rates were just below the range of estimates for a neutral rate.

Previously Powell had said a neutral rate (essentially an interest rate for ‘normal’ economic conditions) was a ‘long way off’.

Characterised as a ‘Powell Put’ traders took this to mean that rate hikes might slow or even be paused entirely.

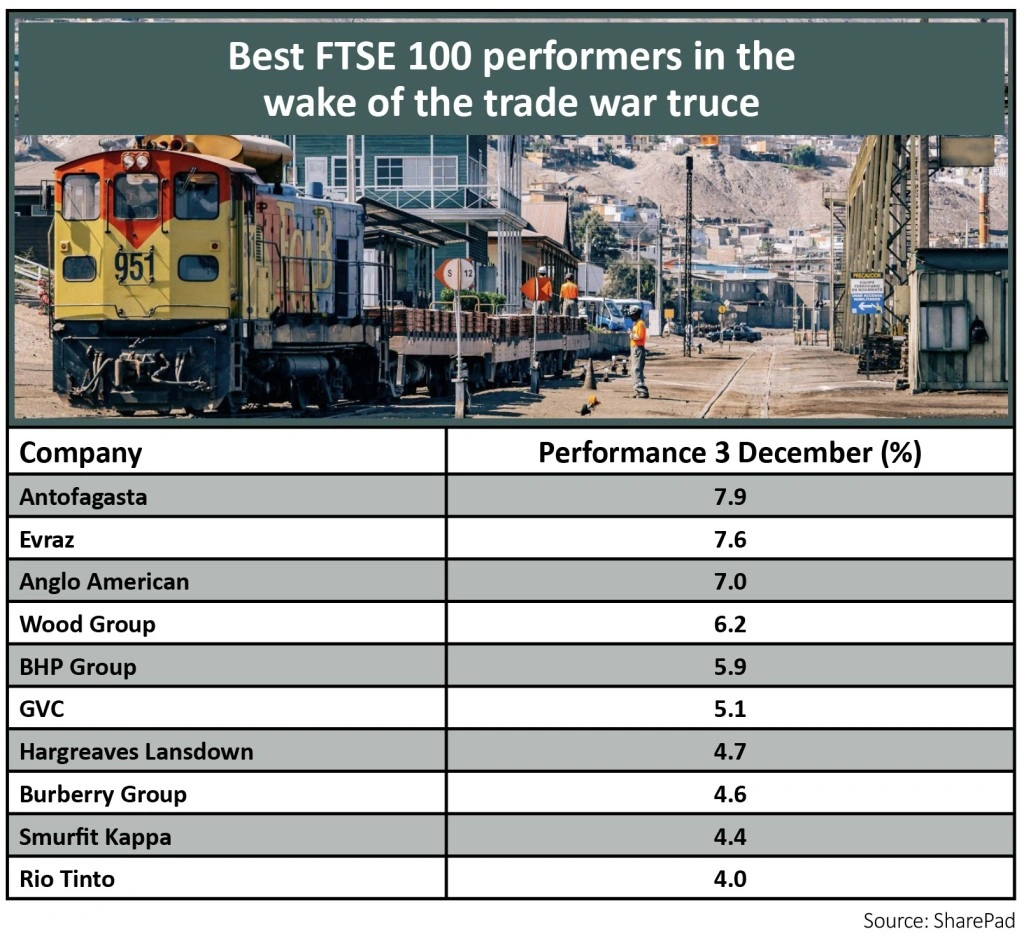

Then on 2 December it emerged that following a meeting at the G20 summit in Argentina between the respective leaders of the US and China, Donald Trump and Xi Jinping, the two countries had agreed a 90-day ceasefire in their trade war.

This addressed, at least partly, another key market worry and sparked a fresh round of gains for global shares.

WHY OIL MATTERS

The FTSE 100, where oil companies BP (BP.) and Royal Dutch Shell (RDSB) have significant weightings, was also boosted by talks between Saudi Arabia and Russia at the G20 which brought the promise of a coordinated effort in the oil market, only slightly soured by news Qatar is quitting OPEC, a cartel of oil producers.

This follows a big sell-off in the oil price from highs above $85 per barrel in early October to around $60 per barrel as we write. Oil and other natural resources were also lifted by hopes that progress on trade between the US and China would support the Chinese economy and support its consumption of commodities.

Unsurprisingly, oil stocks and miners are among the best performers since stocks hit their most recent trough.

WHAT WILL HAPPEN NEXT?

Having opened sharply higher on 3 December, many markets including the FTSE 100 have since surrendered some of those gains, dampening hopes for a so-called ‘Santa Rally’.

Investors should never base their investment decisions on stock market superstitions but research from asset manager Schroders suggests global stock markets have risen in 79% of Decembers since 1987 making it the best month of the year for stocks on average over the last 32 years.

Beyond a positive mood created by the Christmas spirit, one of the reasons for a strong showing in December could be a lack of news flow, negative or otherwise, to knock markets off course.

In 2018 UK investors do not have that luxury – with MPs widely expected to vote down Theresa May’s draft Brexit deal on 11 December, thus prolonging Brexit uncertainty. An OPEC summit today (6 December) could also have a bearing on UK stocks given the FTSE 100’s weighting towards the oil sector.

THE LONG-TERM PICTURE

Longer term the multi-asset investment team at BMO Asset Management are still positive on equities. ‘Growth is above trend in most major countries. With the exception of a few special cases in emerging markets, recession is absent,’ they note.

‘Inflation is also generally low, and the spectre of deflation has receded completely. US interest rates are rising, and the Federal Reserve is shrinking its balance sheet. But interest rates remain low even in the US and are ultra-low in Europe and Japan.

‘We must expect volatility to continue but, in our view, the bull market still has further to run.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.