Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineAlfa Financial has a lot to prove after disastrous start to life on the stock market

In little more than a year Alfa Financial Software (ALFA) has gone from cherished FTSE 250 technology luminary to virtual stock market leper.

In a similar vein to Sir Richard Branson’s quip about how to become a millionaire (start with a billion, then buy an airline), owning shares in Alfa Financial have, thus far, been a ticket to the poor house.

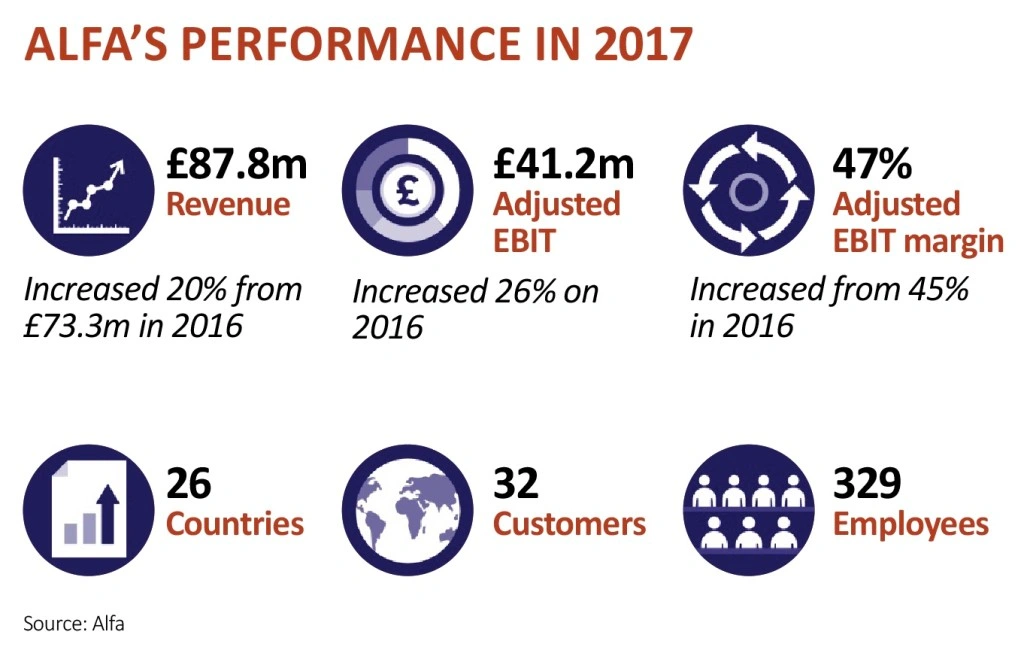

Founded by executive chairman Andrew Page in 1990, Alfa Financial provides an enterprise software system for the asset and consumer finance industry. It joined the stock market on 1 June 2017 with a 325p share price that implied a market valuation of around £975m.

The company is today worth less than half that, the stock changing hands at 153.4p. That puts the market capitalisation at £460m.

WHAT DOES IT DO, AND WHY HAVE THINGS GONE WRONG?

We’ll get to the nitty gritty of events that have shaped this valuation collapse in a bit. First, it is worth understanding what the company does for a living.

Alfa has designed and supplies a browser-based, Java-developed platform that provides tools for financing organisations; computerised new business and agreement management functionality, with workflow and analytics capabilities among other aspects.

Mercedes-Benz, Toyota, Siemens, Barclays (BARC) and Bank of America are all existing clients. Alfa has 10 offices worldwide with more than 250 staff.

Alfa makes its money by first winning pitches to install a solution. This is complex stuff that typically means working closely with a client to assess exactly what is required, and tailoring its platform to fit. This is called software implementation and can take several years to complete.

Clients must take out an accompanying maintenance contract with Alfa once they go ‘live’, which provides online and on-call support, a second line of revenue. Finally, ODS income, or ongoing development services, provides upgrades, new features and customisation.

It is important for investors to get to grips with this income cycle to understand why delays to a few software implementation projects have crushed profits and put investors in a very dark mood.

Results for the six months to 30 June 2018 showed a currency-adjusted 21% fall in revenue to £32.9m, including a 48% slump in software implementation sales (to £13.2m). But because of the knock-on effect to maintenance and ODS, operating profits collapsed by 53% to £8.7m.

Putting that into perspective, analysts at Numis are forecasting Alfa to achieve approximately £20m of operating profit for the full year 2018, yet in early March they had estimates in the market for £47.4m. That’s a massive downgrade by anyone’s standards but adding salt to the wounds is that bad news has trickled out over several months rather than in a single blow.

HOW LIKELY IS A CHANGE FOR THE BETTER?

The big question overhanging Alfa Financial and its share price now is not one of management capability. Chief executive Andrew Denton has almost as many years with the company as chairman Andrew Page (23 versus 28) while non-executives such as Richard Longdon and Robin Taylor have heaps of UK technology industry experience.

Nor is there a problem in principle with the growth opportunity. That’s largely because of the continued dominance of legacy IT systems often developed by large organisations in-house.

With the demand for increased digitisation and new functionality, many of these systems are fast becoming outdated. With a rapidly developing cloud infrastructure, it means organisations are increasingly open to the idea of outsourcing to Alfa’s best in class suite of tools.

Rob Warensjo, of the Megabuyte software industry analysis boutique, has previously stated his belief that Alfa has only scratched the surface of the market opportunity so far.

It is also worth saying that even against such poor recent trading, cash conversion remains impressive, a mark of a quality company. Operating cash flow of £9.9m in the first half equals 115% of operating profit.

No, the big issue facing the company and investors is one of visibility, with management (let alone analysts or investors) unable to predict near-term implementation workloads with any real confidence.

Alfa’s reliance on large deals to meet expectations clearly represents a significant ongoing risk. Yet this cuts both ways. If new or delayed projects come through more quickly than now being forecast there is real scope to reverse the market’s current mood and lift the negative cloud swirling over the company. And that could spark a sudden and substantial re-assessment of Alfa’s nearer-term prospects.

There is positive news, such as an upgrade with a retail bank. Alfa also talks of a ‘healthy’ pipeline of new business bids while there is an order book worth £106m (in total contracted value). This suggests to us that at current share price levels, there is substantially more share price upside potential than down. (SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Brexit tensions stoked as political storm clouds gather

- BAE Systems finally gets jet fighter green light

- Will Aston Martin shares be a luxury you can’t afford?

- Sit tight with Randgold as it may attract a counter bid to Barrick's merger proposal

- Woodford Patient Capital springs back to life

- Why the potential Uber-Deliveroo deal could be a ‘terrifying’ development for Just Eat