Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

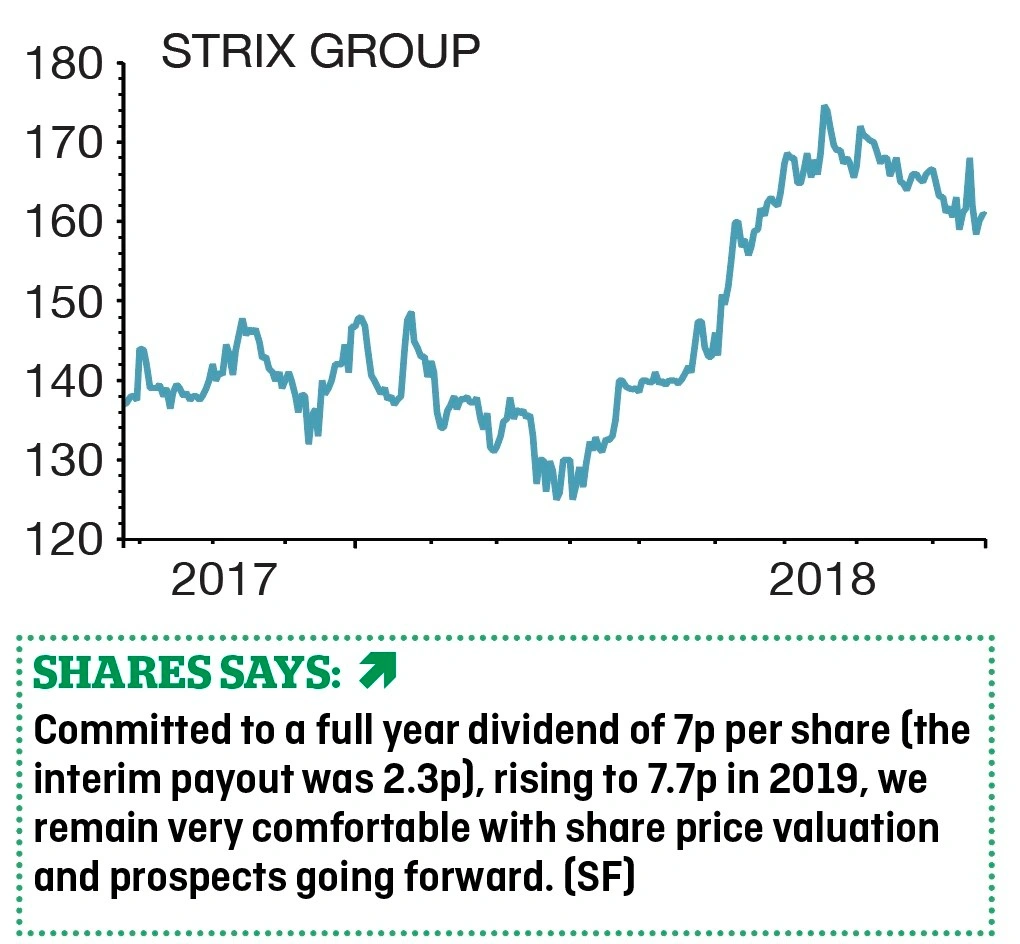

magazinePositive half year results underline Strix appeal

STRIX (KETL:AIM) 160.8p

Gain to date: 14.9%

Original entry point: Buy at 140p, 26 April 2018

Headline revenue growth of just 1.5% in the first six months of this year looks a little on the light side for Strix (KETL:AIM) but exchange rates skew those numbers. Strip out currency effects and the company posted a decent 4% rise.

IPO costs and finance charges also drag on headline pre-tax profits but the underlying picture suggest there is a robust and steady business here.

Maintaining a rough 38% international market share in the kettle controls business is encouraging while it is also worth noting that more than 100% of the £14.8m earnings before interest, tax, depreciation and amortisation (EBITDA) converted into £15.2m cash.

EBITDA margins adjusted for one-off costs also rose 900 basis points to 34.5% while gross profit margins also improved (from 37.2% to 37.9%).

Net debt has also been reduced, another encouraging sign of disciplined financial management, now running at about 1.1-times EBITDA.

Analysts see the shares hitting 210p over the coming months.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Brexit tensions stoked as political storm clouds gather

- BAE Systems finally gets jet fighter green light

- Will Aston Martin shares be a luxury you can’t afford?

- Sit tight with Randgold as it may attract a counter bid to Barrick's merger proposal

- Woodford Patient Capital springs back to life

- Why the potential Uber-Deliveroo deal could be a ‘terrifying’ development for Just Eat