Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy it is still all quiet on the Western front

Erich Maria Remarque’s All Quiet on the Western Front is one of the best-known anti-war novels (and films) as it outlines how German soldiers in France suffered physically and mentally in the trenches (and, ultimately, even once the defeated survivors had returned home).

All the troops want is a peaceful, quiet life and no doubt many investors would share that sentiment, especially with their portfolios in mind.

One of the most startling features of the global equity markets (or at least developed ones) is just how calm they seem to be and history shows this tends to be a good thing, although there do seem to be four clear ‘cycles’ when it comes to market volatility:

– A period (often lengthy) of total calm, where headline indices do not gyrate, as they make steady, consistent upward progress

– A period where the first doubts about the bull market creep in, sellers begin to challenge buyers with the force of their opinions and headline benchmarks make progress but at a lesser rate and with greater effort. Ultimately, this proves too much for nervy buyers and holders, who crack and start to sell.

– A period where doubt finally leads to panic. Volatility becomes the norm as share prices and indices gyrate wildly, but with a clear downward bias. Finally, the wet towels come slopping into the ring as buyers capitulate and turn seller at almost any price.

– Markets bottom amid this final frenzy. Calm descends as buyers begin to regather their nerve as they find assets that are once more attractively valued, and markets begin their next march higher.

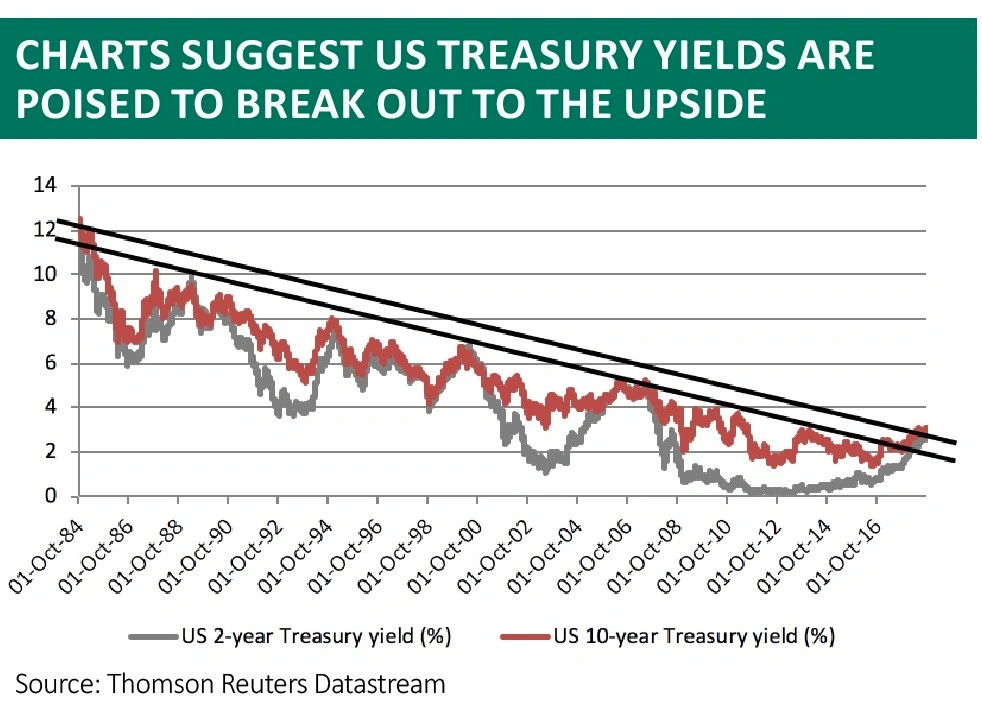

It is not hard to work out where we are now. In the US, the S&P 500 has moved by more than 1% from open to close on a daily basis just 33 times in 2018 to date.

While that is an increase on 2016’s soporific count of just eight times, it leaves the US on track for its quietest year, using this benchmark, since 2006.

In the UK, life is a little livelier, but not much. Thirty-six open-to-close gains or falls of more than 1% in a day again exceeds 2017’s lowly tally of 17 but leaves the FTSE 100 on track for its most docile year since 2005.

So, the questions now are why is trading so torpid? And will it continue?

After all, the good news is that volatility is spookily low as that has tended to be good for equity returns.

But low volatility could be bad news, too. The accompanying charts also suggest that unusual calm leads to unusual risk-taking which leads to over-exuberance, poor capital allocation and eventually volatility’s return with a vengeance as poor (or simply over-valued) investments falter and confidence finally cracks – even if we all know the past is no guarantee for the future.

COOLING DOSE OF CASH

It does seem odd that stock markets should be so calm, given America’s tariff attack on its largest trading partner; the US Federal Reserve’s determination to increase interest rates and withdraw quantitative easing (QE); a bubbly oil price; a stronger dollar; surging global indebtedness; and the cracks that have already appeared in riskier arenas such as cryptocurrencies, emerging/frontier markets and richly-valued technology stocks.

Perhaps those cracks explain why more developed Western markets are holding up, as money retreats from the periphery to the core and to a narrowing selection of assets, geographies, sectors and stocks that are perceived to be ‘safer’.

Equities also appear to be taking the view that central banks still have their back as cheap liquidity leaves oceans of cash sloshing around looking for a decent (risk-adjusted) return.

Many market participants may still favour stocks, given the lowly interest rates available on cash and the historically modest yields offered by (Western) government, corporate and high yield bonds, relative to the risks involved.

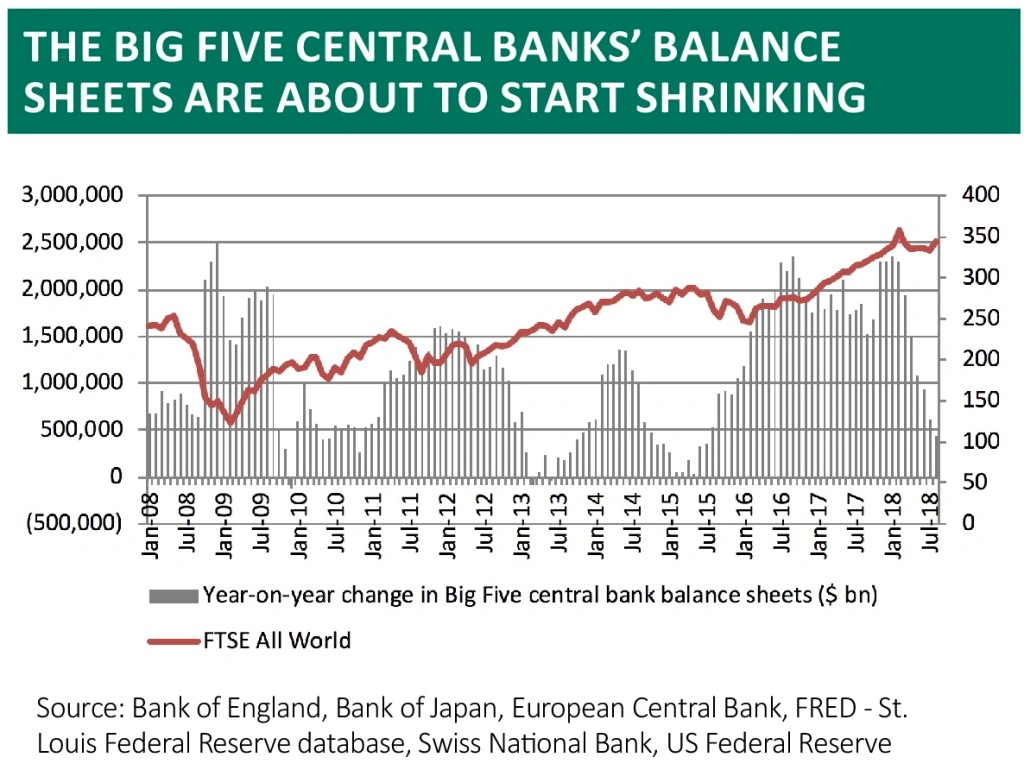

It is easy to see why, looking at how the balance sheets of the US Federal Reserve, European Central Bank, Swiss National Bank, Bank of England and Bank of Japan have swollen since 2008 thanks to the QE, asset-buying schemes.

Every time they have tried to ease back on the stimulus, stocks (and even economies) have wobbled and central banks have turned the taps back on, providing the liquidity in which asset valuations could bathe.

Perhaps the test will come in 2019, as the Fed sterilises QE all the faster and the Bank of England and European Central Bank stand pat, with the result that liquidity will be withdrawn on a net basis.

And if that is accompanied by greater equity index and share price volatility, that could be one early warning signal that investors might like to ponder.

By Russ Mould, investment director, AJ Bell

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Brexit tensions stoked as political storm clouds gather

- BAE Systems finally gets jet fighter green light

- Will Aston Martin shares be a luxury you can’t afford?

- Sit tight with Randgold as it may attract a counter bid to Barrick's merger proposal

- Woodford Patient Capital springs back to life

- Why the potential Uber-Deliveroo deal could be a ‘terrifying’ development for Just Eat