Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

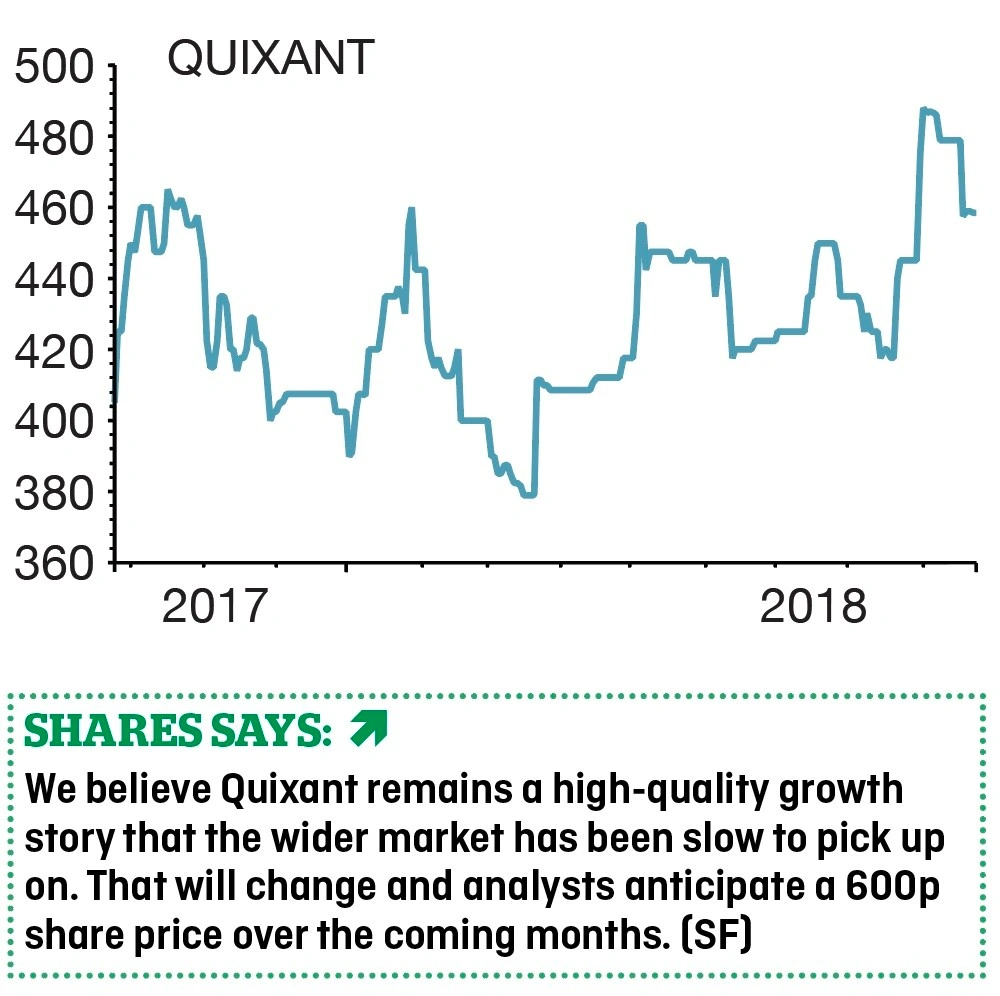

magazineQuixant remains a high-quality growth story with 30%-plus upside

QUIXANT (QXT:AIM) 458.5p

Gain to date: 4.8%

Original entry point: Buy at 437.5p, 25 January 2018

There is no question that Quixant’s (QXT:AIM) share price progress has been surprisingly lacklustre even in the face of continued robust and disciplined financial performance. Half year results on 19 September only embolden our view that it is a long-run, and attractive, growth story.

The first point to make is that last year’s bumper first half was never likely to repeat (thanks to a big one-off order), a point on which management have been crystal clear. A return to the normal 40:60 first half, second half split is expected.

In that light investors can take management’s expectation of another record year in 2018 at face value especially given record unit shipments and order book.

It’s also encouraging that the company will not chase volumes at the expense of profit margins, which should ensure pre-tax profit around the $19m ballpark, versus $17.7m on an adjusted basis in 2017. That’s in spite of some cost pressures, much of which Quixant has been able to pass on to customers, always a sign of a value-adding supplier.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Brexit tensions stoked as political storm clouds gather

- BAE Systems finally gets jet fighter green light

- Will Aston Martin shares be a luxury you can’t afford?

- Sit tight with Randgold as it may attract a counter bid to Barrick's merger proposal

- Woodford Patient Capital springs back to life

- Why the potential Uber-Deliveroo deal could be a ‘terrifying’ development for Just Eat