Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

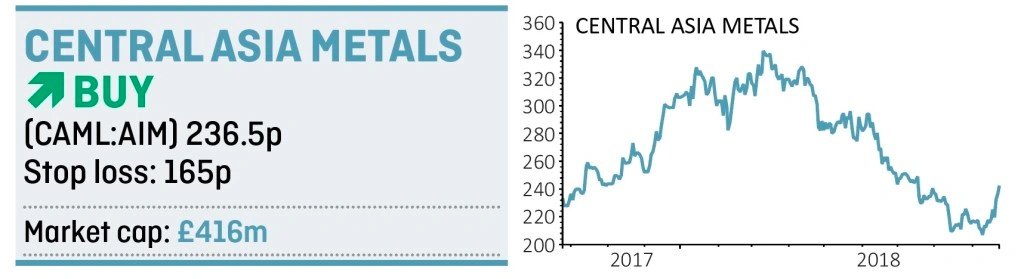

magazineThis metals producer can survive in bleak times and pays a chunky dividend

Buying shares in the mining sector will take some nerve given how commodity prices have been very weak of late, thanks to concerns about how the trade war between the US and China and Chinese economic activity will affect demand for raw materials. Yet buying when no-one is interested can often yield superior returns.

You need to look at the downside risk with mining as much as the upside potential. Many miners operate on slim profit margins and get into all sorts of financial trouble when commodity prices take the slightest knock.

Therefore picking low-cost producers with little or no debt is preferable as they should have a better chance of surviving when times get tougher.

It is against this backdrop that we pick Central Asia Metals (CAML:AIM) as an outstanding stock to buy at the current price. Its management have a track record for being incredibly conservative with their growth plans, in order to ensure they are always creating value for shareholders and not being reckless in the pursuit of growth at any price.

We also note that sector sentiment is improving, as evidenced last week by the highest inflow into industrial metals exchange-traded funds in 15 weeks, according to provider ETF Securities.

Central Asia Metals has very low costs at its two operating mines, plus a $125.2m net debt position is only one fifth of its market cap. It is highly cash generative, meaning it is able to pay down borrowings fairly rapidly and also allocate decent dividends to its shareholders.

You could earn a 6.8% yield based on the consensus forecast 21c (15.98p) dividend in 2019. Its policy is to pay 30% to 50% of operating cash flow, less capital expenditure.

Central Asia Metals’ shares fell from 340p in March to a low of 207p earlier in September, amid a broad sell-off in metal prices. Operationally the business is doing very well apart from a dip in copper production at its Kounrad project in the first half of 2018 due to very cold weather in Kazakhstan.

Kounrad involves reprocessing old mine waste to recover copper. The company has a licence to run this project until 2034.

Last year it bought the Sasa zinc/lead mine in Macedonia which has operated smoothly since purchase. Chief operating officer Scott Yelland says he is looking at ways to improve productivity and efficiency, potentially with a small increase in production. The ore body is being drilled to increase confidence in the mine life, currently at 20 years.

The miner says no acquisitions are currently under consideration despite an appetite to do another deal. (DC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Brexit tensions stoked as political storm clouds gather

- BAE Systems finally gets jet fighter green light

- Will Aston Martin shares be a luxury you can’t afford?

- Sit tight with Randgold as it may attract a counter bid to Barrick's merger proposal

- Woodford Patient Capital springs back to life

- Why the potential Uber-Deliveroo deal could be a ‘terrifying’ development for Just Eat