Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSit tight with Randgold as it may attract a counter bid to Barrick's merger proposal

We believe Randgold Resources’ (RRS) proposed nil-premium merger with Barrick Gold is a bad deal for shareholders. Sit tight and see how the situation plays out, as there is potential for a counterbid now that the miner is ‘in play’. Anglogold and Newmont look more suited to a tie-up with Randgold.

Under the Barrick plan, Randgold’s London listing will be cancelled and investors will be left with shares that only trade in New York and Toronto.

There are major cultural differences between the groups which could create problems, plus Randgold is becoming part of a business that has destroyed value for shareholders over the years, not created it.

The winners of the merger are Barrick Gold’s shareholders as they are effectively getting someone to take control of a broken business and potentially fix it.

Having a more disciplined leadership team – Randgold’s management are taking the chief executive and finance director roles at the enlarged group – could help tidy up Barrick.

Randgold is getting access to top tier assets which helps offset the fact it hasn’t had much exploration success recently. However, the early stages of the merger are likely to be focused on cleaning up the business and not advancing growth.

Investment bank Jefferies says it has previously been concerned about ‘a lack of clear strategic direction’ for Barrick as its portfolio had been shrinking, its free cash flow was close to zero and it had no chief executive following the departure of president Kelvin Dushnisky in August.

These are hardly glowing credentials for Randgold’s shareholders seeking to understand the attractions of a business about to merge with their investee company.

Shares in Barrick fell by 89% in the four years to September 2015 – falling from $55.18 to $5.94 – and a recovery rally to $20.5 in 2017 was short lived with the stock subsequently drifting back to $10.47 on the eve of the Randgold merger.

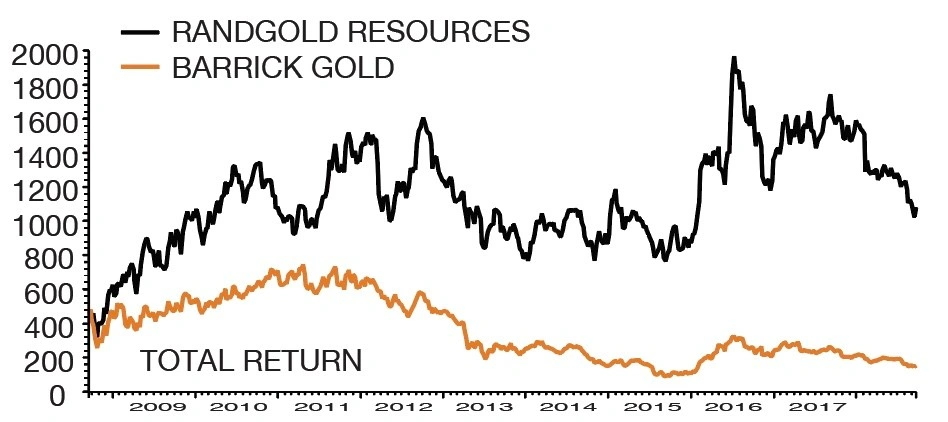

While Randgold’s shares have also been weak of late, due to resource nationalism issues and a weaker gold price, the longer-term performance is far superior. On a 10-year basis with all dividends reinvested, Randgold has delivered 120% positive total return versus a 66% loss from Barrick. (DC)

The number of people betting against the gold price – i.e. hoping it will fall in value – has more than doubled year-on-year, notes Russ Mould, investment director at AJ Bell. ‘But on every occasion this has happened since 2013, bar one, gold subsequently rallied,’ he adds, suggesting the smart trade is to buy gold now.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Brexit tensions stoked as political storm clouds gather

- BAE Systems finally gets jet fighter green light

- Will Aston Martin shares be a luxury you can’t afford?

- Sit tight with Randgold as it may attract a counter bid to Barrick's merger proposal

- Woodford Patient Capital springs back to life

- Why the potential Uber-Deliveroo deal could be a ‘terrifying’ development for Just Eat