Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineUp, up and away: 8 momentum stocks to buy now

Investing in companies that are in a rising trend can often be a great way to profit from the market. Stocks on a tear often find those strong runs last far longer, and go far higher, than most normal investors might expect.

Fund manager and renowned momentum investor Richard Driehaus takes exception to the old stock market adage of buying low and selling high by saying ‘far more money is made buying high and selling at even higher prices’.

DOES IT WORK?

It certainly can. Almost exactly two years ago Shares ran a momentum exercise focusing on half a dozen UK stocks.

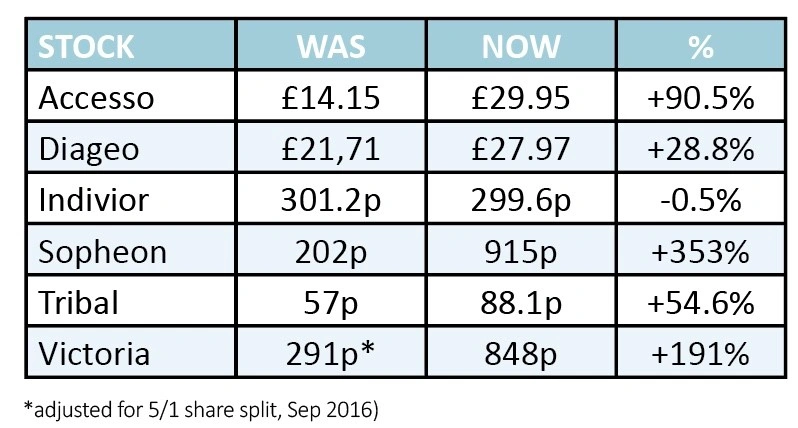

These six companies included: Smirnoff vodka-to-Guinness stout owner Diageo (DGE), acquisitive floor coverings maker Victoria (VCP:AIM) and attractions software supplier Accesso (ACSO:AIM). We also give our view on lifecycle management software play Sopheon (SPE:AIM), e-learning software and services provider Tribal (TRB:AIM) and pharmaceuticals company Indivior (INDV).

The 2016 year-to-date returns at the time of selection ranged from the reasonably good (17% from Diageo) to the quite astonishing (253% Sopheon, 138% Tribal and 71% Accesso).

Most sceptics would be hard-pressed to see substantial extra upside from stocks that had already chalked-up such staggering returns. Yet nearly all of them have made investors even richer in the subsequent period.

Here’s how the six have performed in the two years since 18 August 2016:

Despite being roughly 10 years into the current bull run for UK (and global) share prices there remains more investment upside. Shares has looked across the FTSE All Share index to see what’s been going up this year. We’ve picked out 10 investment stories we think are worth explaining. All of these highlighted shares have been outstripping the overall market performance.

True, so far this year the UK stock market has done precious little, clawing out a measly 0.6% so far in 2018. That’s the FTSE 100 performance, but it’s pretty much matched by the 0.5% return of the wider FTSE All-Share index.

DOUBLE THE MARKET’S RETURN

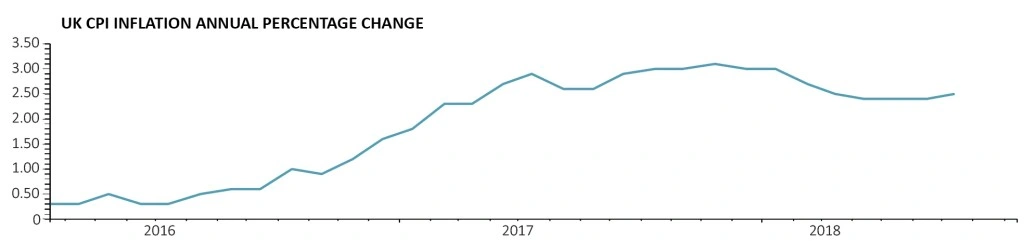

That said, the seven and a bit months since 2018 began have not been entirely uneventful, with anodyne UK economic growth, rising interest rates, higher inflation and those big Brexit questions churning below a seemingly calm surface.

Since the end of March (26 March, 2018 low point), for example, the FTSE 100 has jumped by nearly 1,000 points, while the FTSE All-Share has rallied more than 11%.

Interestingly, of the 638 companies included in the FTSE All-Share index (according to FTSE Russell’s 31 July data) 87 have put up return of at least double that performance. Some of those performances are due to takeovers, either real or speculated, but many have been driven by firm trading, forecast outperformance and optimism on future prospects.

Our 10 stocks might not be the best performers in absolute terms during the past few months but these are (largely) companies that we believe have a very good chance of continuing their forward momentum.

A couple – supermarket chain J Sainsbury (SBRY) and pharma firm Hikma Pharmaceuticals (HIK) – stand apart because we see very good reasons why market sentiment is at risk of turning against these investment stories. Here’s why we believe eight of our 10 featured companies are worth buying high to go even higher.

BCA MARKETPLACE (BCA) 235p. BUY

55.8% gain since 26 March 2018

BCA Marketplace (BCA) owns car auction sites and webuyanycar.com and has a large market share of the used car market. The company sold 1m used cars in its 2018 financial year, with around a 60% share of the auction market which accounts for about 20% of annual used car transactions.

Its share price ascent stepped up a gear when private equity house Apax Partners approached the company with a buy-out offer in June.

However, the company’s share price had been rising before the Apax bid came in and continues to ascend after the private equity house walked away when its second improved offer was rebuked by the board.

BCA’s chairman Avril Palmer-Baunack says the company looks after the whole life of the car and its deal with BMW shows the scope of the business. It provides BMW with a host of services from refurbishment, inspection and remarketing.

Despite Brexit, BCA is creating a standardised platform called ‘One Europe’ which sells cars across various borders in continental Europe. The company currently operates auctions in nine countries in Europe, it looks to be growing the number of jurisdictions it operates in and should continue to see its value rise. (DS)

BLOOMSBURY PUBLISHING (BMY) 234.2p. BUY

27.1% gain since 26 March 2018

The starting gun on Bloomsbury Publishing’s (BMY) recent outperformance was fired by full year results showing pre-tax profit, before one-off items, up 10% to £13.2m in the 12 months to 28 February.

The company also noted that a strong autumn book list and the acquisition of I. B. Tauris & Co would result in performance for the February 2019 year well ahead of previous expectations.

An encouraging first quarter update on 18 July maintained that guidance and revealed some encouraging new developments – including a new book from celebrity chef Tom Kerridge to accompany a major BBC TV series.

Results for the six-month period to 31 August will be announced on 23 October and could provide a relatively near-term driver for the share price.

The Harry Potter series continues to generate significant sales for the publisher and the release of the Fantastic Beasts: The Crimes of Grindelwald film this winter should sustain interest in the series given it is set in the same universe.

In the longer-term the company’s Bloomsbury 2020 digital resources growth strategy aims to focus on digital non-consumer publishing for the business-to-business academic and professional information market. (TS)

ELECTROCOMPONENTS (ECM) 754.4p. BUY

30.7% gain since 26 March 2018

Electrical goods distributer Electrocomponents (ECM) has enjoyed and continues to enjoy a renaissance since Lindsley Ruth took over as CEO in 2015. His performance improvement plan began in 2016 and achieved savings of £30m; part two looks to make £12m of annualised savings a year from now until 2021.

The company’s addressable market is huge, it supplies a vast array of equipment to engineers such as tools, safety equipment and even semiconductors.

Electrocomponents is cyclical in nature. As economic activity remains resilient, there should be a heightened need for the company’s services.

It has made a great move with the introduction of the RS Pro range of equipment. These tools are made by the company so rather than distributing products made by others, Electrocomponents is also manufacturing which will increasing its profit margins substantially.

With the International Monetary Fund’s predictions of improving global growth for 2018 and 2019, there doesn’t look to be too much immediate risk to Electrocomponent’s continued share price ascendancy.

Last month’s first quarter growth statistics show a company in good shape, with all its geographic regions being in growth mode. (DS)

FINDEL (FDL) 280p. BUY

25.4% gain since 26 March 2018

Shares in value retail-to-educational supplies specialist Findel (FDL) are flying high and we reckon the positive momentum can continue.

Under the stewardship of CEO Phil Maudsley, adjusted profit before tax ticked up 21% to £26.8m in the year to March 2018 and the multi-channel retailer has made a strong start to fiscal 2019 too.

Revenue growth at its core Express Gifts division accelerated in the 16 weeks to 20 July with online ordering levels rising from 68% at the year end to 70%, providing a strong platform ahead of Christmas.

Meanwhile, the turnaround of the Education business is showing encouraging signs with the customer base now in growth for the first time ‘in several years’ and online ordering on the rise.

A purveyor of budget clothing, footwear and toys whose active customer base grew 0.2m to 1.8m last year, Express Gifts is geared into the structural shift online and the quest for value.

Findel’s largest shareholder Sports Direct (SPD) is already supplying menswear ranges to Express Gifts and can help Findel to improve its own supply chains.

Extending ties with Sports Direct could turbocharge the top line and even pave the way for an eventual takeover bid. Meantime, the investment is being de-risked with Findel’s balance sheet strengthening, core net debt (excluding receivables-related debt) was down 8.7% to £73.8m last year. (JC)

HALMA (HLMA) £14.06. BUY

22.7% gain since 26 March 2018

This is a big business with significant growth tailwinds such as advances in safety regulations, ageing and urbanising global populations, and other demographic trends.

Halma is a global manufacturer and seller of a wide range of equipment largely demanded by health, safety and environmental rules. This includes hazard detectors, sensors and assorted environmental protection kits.

Organic growth is supplemented by carefully selected bolt-on niche acquisitions that generate strong returns and which it can help to develop, under its Halma 4.0 growth strategy, which should protect the company as its markets adapt to technological changes and opportunities.

The strategy has produced a virtuous circle of reliable growth and cash generation that pays for the next stage of investment. Analysts note it has a 30-year track record of 11% a year compound revenue growth rate, impressive to say the least.

But there’s a valuable income story too thanks to Halma’s unrivalled record in dividend expansion which extends to 40-odd years. (SF)

HIKMA PHARMACEUTICAL (HIK) £16.75. AVOID

45% gain since 26 March 2018

Hikma has enjoyed a share price rally recently, but we think this is unwarranted as the generic drugs market remains difficult with overseas rivals such as Teva and Mylan suffering over 20% declines in sales.

The ongoing struggle to launch a generic version of GlaxoSmithKline’s (GSK) Advair continues as Hikma needs to conduct a further clinical trial, delaying its attempt to beat rivals to the US market.

In May, the drugs developer revealed a robust start to its financial year across the business, driven by several product launches.

Unfortunately, intense competition remains a concern and is expected to accelerate throughout the year, potentially keeping pricing under pressure. Investors should be cautious and wait for greater evidence of a recovery as Hikma was forced to cut profit guidance three times in 2017. (LMJ)

JOHNSON MATTHEY (JMAT) £37.17. BUY

20.1% gain since 26 March 2018

By 2022, chemicals business Johnson Matthey is expected to have the best long-range, high-nickel cathode technology in the world according to Berenberg analyst Sebastian Bray.

Johnson Matthey is making impressive progress developing its enhanced lithium nickel oxide material for use in electric vehicles. Earlier this year, capacity at its demonstration plant was doubled to 1,000 tonnes with more capacity potentially being added in the future.

One of the biggest issues clouding sentiment is a disconnect between investor expectations and Johnson Matthey’s outlook, leading to a significant discount to rival Umicore according to Berenberg.

Despite the growing ‘death of diesel’ rhetoric, the company is still expected to grow its autocatalyst business by 5% to 6% every year until 2022.

Investors should note that Johnson Matthey can tap into a growing switch to electric cars with its battery tech and it is unlikely the diesel industry will disappear anytime soon.

This is not the only division with strong prospects as Johnson Matthey also creates active pharmaceutical ingredients for treatments, which is forecast to add £100m to earnings by 2025. (LMJ)

PREMIER OIL (PMO) 123.2p. BUY

79.6% gain since 26 March 2018

Oil producer Premier Oil (PMO) is on the march as it gets its balance sheet under control and starts to see the benefits of a higher oil price reflected in its financial performance.

The company took on too much debt ahead of the oil price crash in 2014 and completed a fairly painful financial restructuring in 2017.

The rise in crude has allowed it to begin paying down its borrowings and under chief executive Tony Durrant, former finance director, considerable emphasis has been placed on cost discipline.

As Premier deleverages we would expect the market to ascribe more value to its equity. In terms of catalysts the company is scheduled to being appraisal drilling on its substantial Zama discovery offshore Mexico in the fourth quarter.

That said, indebted oil firms are particularly sensitive to movements in the oil market as even relatively modest movements can make a significant difference to their financial position, so a big fall in oil prices could undermine our positive view. (TS)

J SAINSBURY (SBRY) 333.7p. AVOID

47.2% gain since 26 March 2018

Shares in J Sainsbury (SBRY) have surged since CEO Mike Coupe announced an audacious £7.3bn takeover of Asda that would see the combined entity leapfrog Tesco (TSCO) in UK market share terms.

Coupe insists the combination will create a dynamic new player in UK retail, a resurgent Tesco and the looming Amazon threat no doubt giving him sleepless nights. Yet this complex merger will prove a huge distraction for management and has understandably fallen into the clutches of the Competition and Markets Authority (CMA) given the impact on suppliers and customers.

Shore Capital says the CMA’s involvement means ‘the Sainsbury investment case is fossilised and so based more around speculation and likelihoods rather than financial visibility’. And don’t forget, Sainsbury is already swimming in treacle.

Like-for-like sales growth slowed to 0.2% in the first quarter to 30 June and the latest Kantar Worldpanel (24 Jul) data, covering the 12 weeks to 15 July, revealed a 0.4% market share decline to 15.6% in the face of growing competition from Aldi and Lidl, albeit Asda surprisingly proved the best performer of the big four retailers for the first time since December 2014. (JC)

SCOTTISH MORTGAGE INVESTMENT TRUST (SMT) 555.5p. BUY

24.1% gain since 26 March 2018

Lots of investors prefer collectives to buying individual company shares but that needn’t mean missing out on a momentum ride.

Scottish Mortgage’s shares have consistently grown for five years and its track record of returns makes it one of the stock market’s most popular investment trusts.

Run by respected manager James Anderson for the best part of two decades (with help from capable deputy Tom Slater), it takes big stakes in some of the most exciting mega-cap growth companies in the world including Tesla.

For example, the trust has 9.9% of its funds invested in online retail giant Amazon, whose shares have risen five-fold in five years.

There are decent stakes in Netflix, genome testing kit maker Illumina, and two of China’s internet stars, Tencent and Alibaba as well. But this is not a technology fund; Scottish Mortgage’s management team look for ‘blue sky growth,’ the trust says, aiming to buy the best growth companies in the world for the next five or 10 years.

Investing in emerging stars of tomorrow will be a popular strategy for many longer-term investors and Scottish Mortgage’s record stands up to pretty much any other similarly focused fund. That explains the 3.75% premium to net assets at which the stock currently trades. (SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.