Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThree reasons why the FTSE 100 can make a fresh high before year-end (and three why it may not)

Before concerns about Turkey and emerging market contagion burst onto the scene last week the FTSE 100’s summer surge had

taken the index back toward its May closing

all-time high of 7,877.

This seemed to be a classic case of share prices ‘climbing the wall of worry’ as they cast aside fears over Brexit, a wobbly Government, modest economic growth and higher interest rates to

press higher.

However, the latest failed attempt at a new peak (and indeed the 8,000 mark) raises the issue of whether UK equities are instead poised to ‘slide down the slope of hope’ if expectations for economic, profit and dividend growth are not met, for whatever (unexpected) reason.

Three factors look quite capable of providing support to the FTSE 100 or even taking it higher although three others suggest that gravity could start to take its toll after a nine-year bull run.

THE CASE FOR FURTHER GAINS

1. Dividend yield

According to consensus forecasts the FTSE 100 offers a 4% dividend yield for 2018, with total payments to shareholders expected to rise by 9% this year to a record £88.7bn.

That 4% easily beats cash in the bank and inflation. It also exceeds the yield available on the 10-year Government bond (also known as gilts).

At the time of writing gilts yield 1.35%, so the FTSE 100 dividend yield tops that by 265 basis points, or 2.65 percentage points. A yield premium of around 200 basis points, or two percentage points, has tended to provide support to the

FTSE 100 index in the post-crisis era.

2. Sterling

The glacial pace of interest rate rises, patchy economic data and concerns over Brexit all mean the pound is on the back foot once more, especially against the dollar, but this is also providing support for UK-quoted stocks.

Around two-thirds of the FTSE 100 index’s earnings come from overseas, so the lower the pound goes, the more those foreign earnings are worth when they are translated into sterling. This helps to explain the clear recent trend of ‘pound down, FTSE 100 up’.

A weak pound also makes British assets cheaper for overseas buyers – it may be no coincidence that FTSE 100 members Sky (SKY), Smurfit Kappa (SKG) and Shire (SHP) have all received bids from overseas firms in 2018 and

any further slide in sterling could perhaps tempt more predators to pounce.

3. Positive earnings momentum

Sterling’s latest slide fits in here, too. In a marked contrast to the past four years, earnings forecasts for the FTSE 100 are rising, not falling, helped by the weaker pound, a higher oil price and the absence of new major restructuring costs, legal bills and asset write-downs at the banks.

The next chart shows how aggregate profit forecasts for the FTSE 100 have developed on a quarterly basis over time.

History suggests that market tops occur when interest rates are rising, stocks are expensive and earnings estimates are falling. For the moment it seems that only the first of those pre-conditions

is in place.

THE CASE FOR CAUTION

However, this is not to say that investors can be complacent. Earnings forecast momentum has begun to ease and there are three reasons for possibly approaching UK stocks with a degree of caution.

1. No fear

A low reading on the FTSE VIX index, which measures future volatility expectations, suggests complacency levels are relatively high.

It may not take much to frighten everyone and usher in a more difficult period and the chart makes the inverse relationship between the FTSE VIX and the FTSE 100 pretty clear. It could be argued that we are overdue a storm of some kind.

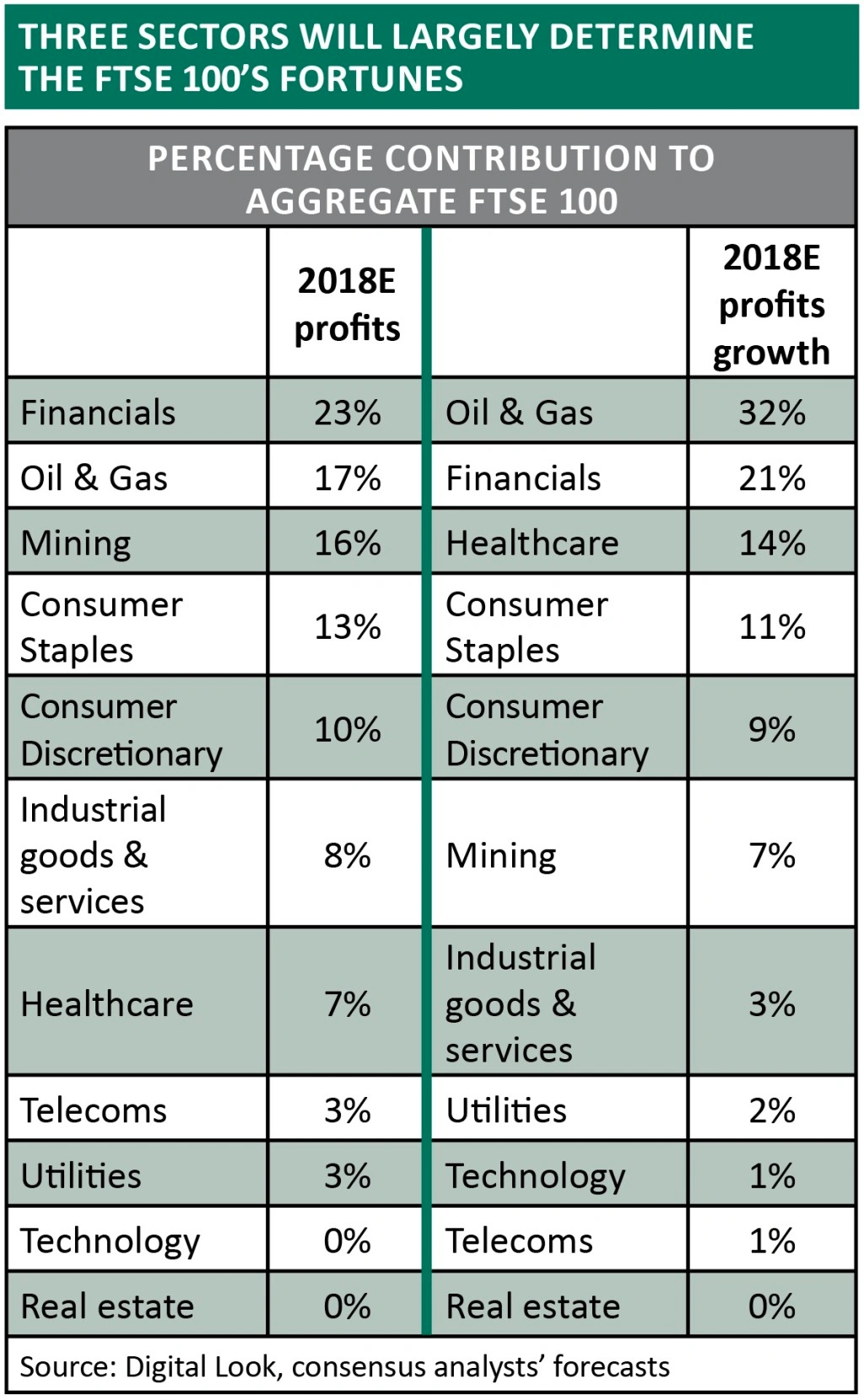

2. The dominance of banks, oils and miners

The FTSE 100 is heavily skewed in terms of its market cap, income and dividends to just a dozen or so stocks and three or four sectors: financials (banks in particular), oil producers and miners.

Investors with exposure to UK stocks, especially those who put their money to work via a passive tracker, must therefore be comfortable with these firms and sectors’ prospects.

For the moment, banks (as the economy chugs along and regulatory pressure and conduct fines start to fade away), miners (cost cuts and greater capital discipline) and oils (juicy dividends, cost cuts and greater capital rigour) all look set fair.

However, they are all volatile, unpredictable industries and nothing can be taken for granted. In addition, oil, copper and iron ore prices have all started to soften again.

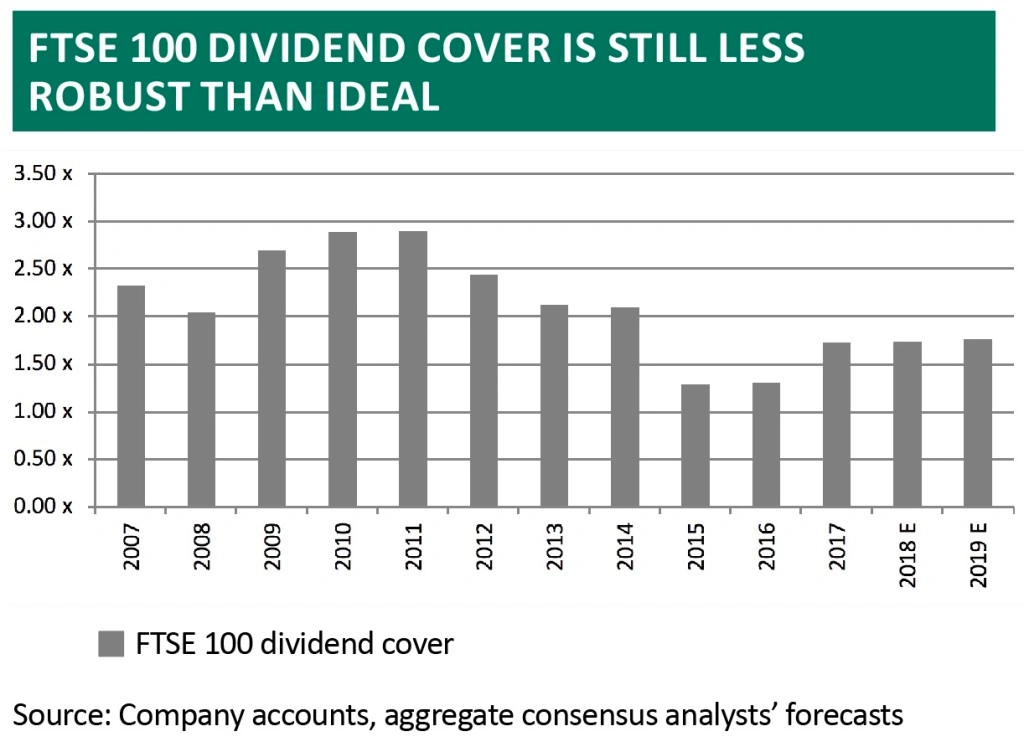

3. Dividend cover

Although the FTSE 100’s dividend yield is attractive, it may not be entirely safe. Forecast earnings only cover forecast dividend payments by 1.7 times – although that is higher than of late, it is still below the 2.0 times cover ratio that provides some comfort should anything suddenly go wrong.

The yield premium relative to bonds may look attractive but if dividends are cut (say in the event of a sudden economic downturn), or bond yields go up (because the Bank of England raises interest rates more quickly than expected) then that relationship could change.

The good news is that dividend cuts have become much rarer after a bad run of reductions in 2015-2016 but any unforeseen economic stumble could leave pay-out growth forecasts exposed – and profit and growth disappointment could then lead to a trip down the slope of hope.

Russ Mould, investment director, AJ Bell

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.