Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineGI Update - Diageo

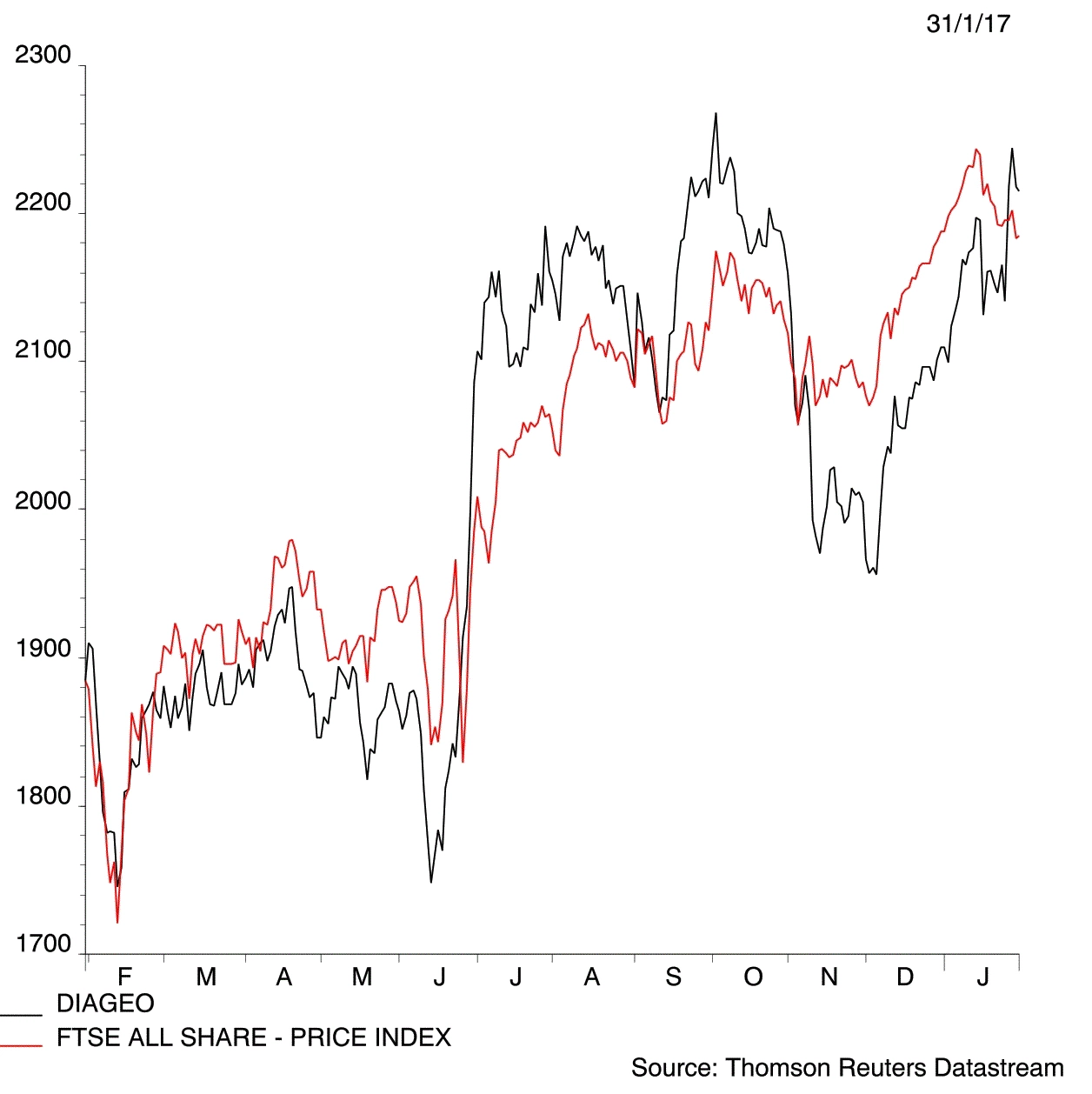

Diageo (DGE) £22.24

Gain to date: 2.3%

Original entry point: Buy at £21.73, 12 January 2017

We’re sticking with our positive stance on alcoholic drinks giant Diageo (DGE), our ‘buy’ call modestly in the money following better-than-expected first half results (26 Jan). These revealed organic volume growth of 4.4%, ahead of expectations of 3.1% and helped by Johnnie Walker whisky and the reinvigorated US business.

While Diageo’s shares have enjoyed a rally over the past two months, management’s tone is upbeat and we think there are more positives to emanate from the turnaround. In particular, productivity and cost savings are coming through.

Diageo remains a high-quality name worth owning given 2017’s uncertainties. Strong brands represent an economic moat, engendering loyalty among consumers, conferring pricing power upon Diageo and creating barriers to entry for rivals. Earnings are geographically diversified and free cash flow generation remains strong – up £245m to £1.08bn in the six months to December – supporting investment in competitive advantage and a progressive dividend. The payout was up 5% to 23.7p at the interim stage.

We’re in agreement with the bullish consensus view, heartened by the improved first half results from the world’s biggest spirits business. (JC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.