Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine‘Double your money’ with SDX Energy

Oil and gas producer SDX Energy (SDX:AIM) is on course for a step change in scale. The company has secured $40m in an over-subscribed placing (27 Jan) to fund the acquisition of assets in Egypt and Morocco from financially distressed peer Circle Oil (COP:AIM). Buy the shares at 38.23p.

Broker Cantor Fitzgerald believes the company will be worth 78p a share in a year’s time, implying that investors could double their money.

Why the new deal is important

The acquisition will boost SDX’s output by 247% to 4,705 barrels of oil equivalent per day. Proved and probable reserves will increase by 64% to a little over 12m barrels of oil equivalent per day (boepd).

Cantor estimates the deal will pay for itself in a mere 16 months, based on current oil prices. It believes the acquisition will boost cash flow by $22m in 2017 and by $28m in 2018.

A quarter of the way towards the big target

Analyst Sam Wahab says: ‘In terms of deal metrics, we believe SDX has secured a value accretive set of assets at a considerable discount to net present value, with an inferred acquisition price of $6.40 per barrel of oil equivalent.’

SDX raised $11m when it joined AIM in May 2016. At that time, chief executive Paul Welch told Shares about his plan to raise output to 20,000 boepd through exploration, development drilling and acquisitions.

Welch hinted SDX might put itself up for sale once that goal was achieved, flagging aspirations for a potential takeover in the region of $850m and $1.2bn.

The Circle Oil deal effectively gets SDX 25% of the way to Welch’s 20,000 boepd target.

It incorporates a further 40% in the NW Gemsa concession where SDX currently has a 10% working interest, in addition to two assets onshore Morocco.

Improved investment case

The move into Morocco improves the investment case as SDX no longer has a single country focus.

The transaction includes $16m of receivables which is essentially cash owed to Circle by the Egyptian government.

Investors will need to keep an eye on SDX’s ability to recover this money. Encouragingly it has had few problems with receivables in its existing business.

Although the company’s focus is low-cost production there are also plans to drill an exploration well on the South Disouq licence. Scheduled for the first quarter of 2017, this will target 715bn cubic feet of gas net to the company’s 55% interest.

The stock looks an absolute bargain at 38.23p, trading on a mere 1.9 times forecast earnings for the year to January 2018. Buy. (TS)

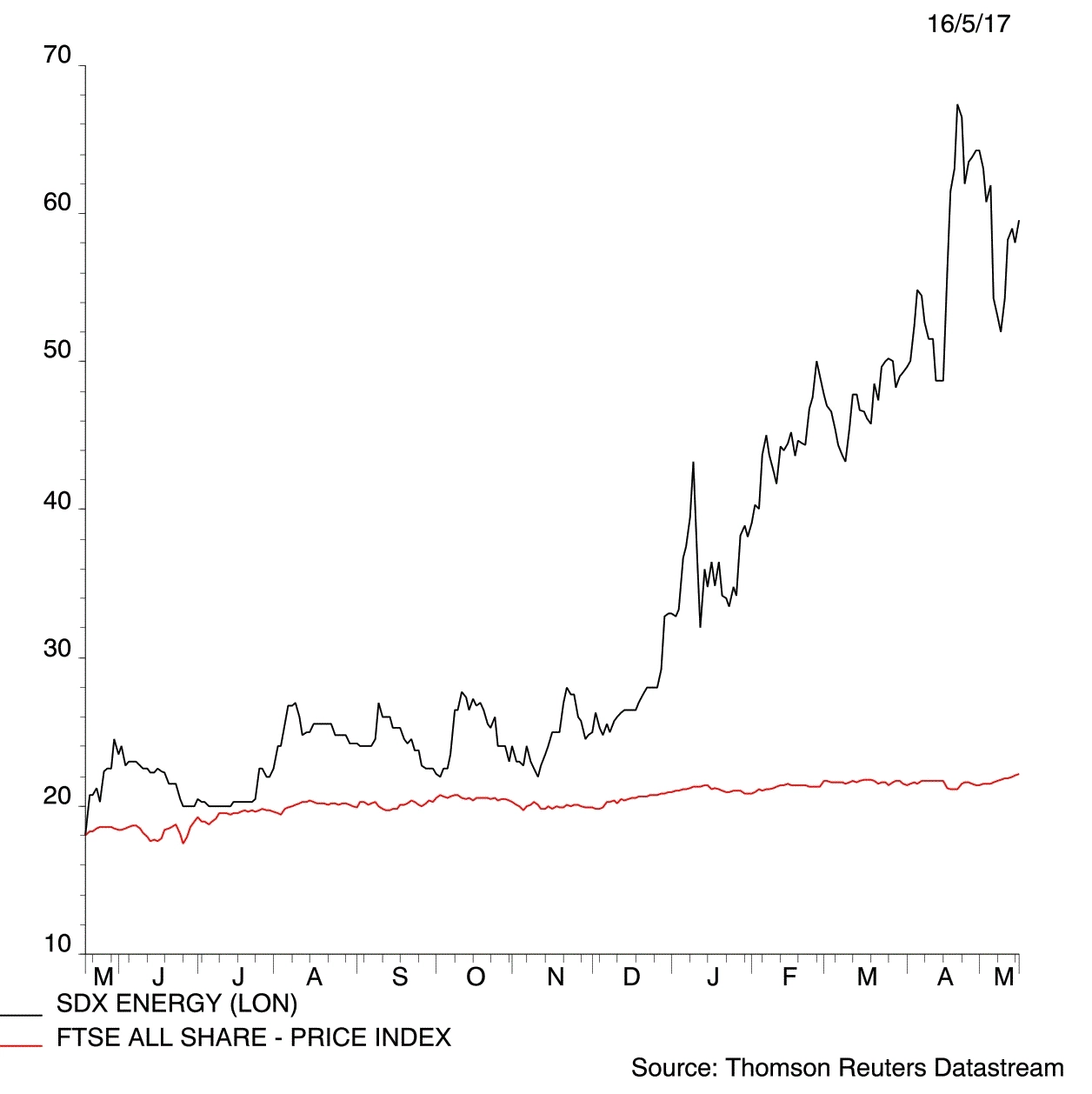

SDX Energy (SDX:AIM) 38.23p

Stop loss: 25p

Market value: £31m

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.