Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

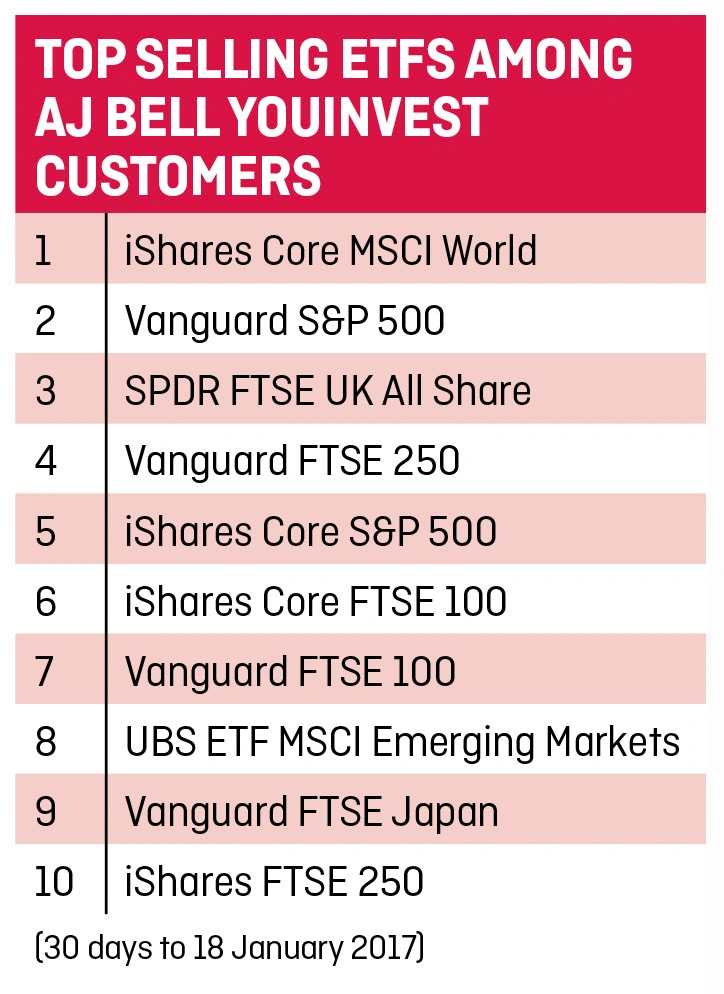

magazine

magazineETFs demystified: Part 1 of our fund series

You may have heard of exchange-traded funds (ETFs), but have you actually invested in any? Over the next three weeks we will explain their appeal and how they can play an important role in your investment strategy.

In the coming weeks we will also discuss how many ETF products are very clever in how they focus on specific factors like value, momentum and quality.

Many people only talk about ETFs being low cost instruments and don’t really consider any other points. In reality, there is much more to consider with ETFs such as the stocks or other asset classes they are tracking and why you would want to have such exposure in your portfolio.

We will touch on all those points in our three-part series so that you can better understand why ETFs can potentially enhance your returns and be more efficient investment vehicles than some mainstream actively-managed funds.

What are ETFs?

Exchange-traded funds are growing in popularity as a simple, low-cost tool for getting access to a range of companies, commodities and countries across the globe.

They are similar to funds in that they invest in a pool of assets and provide exposure to a particular theme or market.

The key difference is ETFs are traded on an exchange. This means you can buy and sell them at any time during trading hours, at the price shown.

ETFs are fairly transparent. Unlike a fund, whose manager might be reluctant to reveal their holdings and tactics, you can generally see what ETFs are investing in. This is because the vast majority of ETFs track a specific index. They will clearly state the name of each index, so you can easily check how that index is constructed.

ETFs fall under a broader umbrella of exchange-traded products (ETPs), which also include exchange-traded certificates (ETCs) and exchange-traded notes (ETNs).

ETCs track specific baskets of commodities, such as gold, wheat or corn. ETNs are more complicated because they’re issued as senior debt notes, which introduces credit risk.

In our opinion, retail investors shouldn’t get involved with ETNs unless they are very experienced and fully understand the risks.

Are ETFs aimed at certain types of investors?

ETFs are relevant for both short-term and long-term investors. Traders sometimes use them to play the market. Biotech ETFs, for example, saw significant inflows around the US election as a short-term trade on Donald Trump winning the presidency.

The pharmaceutical and biotechnology sector had previously been dragged down by concerns that Hillary Clinton would impose strict price caps on drugs (and therefore hurt corporate profitability in the drug sector) if she had won the US presidential election.

ETFs are also good vehicles for long-term investing and can form the core part of an investment process.

Typical fees for ETFs can be circa 0.30% a year vs 0.75% to 1.25% for traditionally actively-managed funds

What are the fees compared to an actively-managed fund?

In recent years, ETFs have become very popular among retail investors. Part of their appeal is their low-cost. In general, ongoing charges for ETFs are in the range of 0.30% compared with 0.75% to 1.25% for a traditional actively-managed fund.

Chris Mellor, executive director at ETF provider Source, says fees are extremely important in the current environment of low interest rates, which have led to poor returns on fixed income and lower growth rates for equities. ‘High fees eat into returns a lot more in this environment, so there is a lot of pressure to reduce fees,’ he says.

In recent years there has been a lot of furore around the inability of several active fund managers to beat their benchmarks. In the US, for example, more than 99% of active funds have trailed their benchmark over the past 10 years, according to S&P Global.

‘Every pound you pay to someone to manage your money for you is money which cannot work for you in the market,’ says Adam French, co-founder and chief executive of online wealth manager Scalable Capital.

As we mentioned at the start of this article, cost is not the be-all and end-all. There are a whole range of factors to consider before buying an ETF.

Top five questions to ask before investing in an ETF

1. What is the underlying index?

Exchange-traded funds track a huge array of indices. Some track well-known indices like the FTSE 100 or S&P 500 which feature large companies on the UK and US stock markets, respectively. Other indices track emerging or frontier markets. Some track specific sectors like technology; and others track fixed income securities.

You should look at the underlying index being tracked and consider why you want exposure to it. If you’re a new investor you might want to opt for a very broad ETF. For example, a suitable product might be Source MSCI World UCITS ETF (MXWO) whose constituent equities give you access to several developed markets.

Mellor says you could then add other ETFs to skew your portfolio, take a particular view or broaden your exposure.

If you think the US is going to do well you could invest in Source S&P 500 UCITS ETF (SPXP), which gives you exposure to the largest companies in the US, such as Apple (AAPL:NDQ), Microsoft (MSFT:NDQ), Amazon (AMZN:NDQ), Facebook (FB:NDQ) and JPMorgan Chase (JPM:NYSE).

If you want to add some emerging markets exposure to your portfolio you could invest in a broad emerging markets ETF, such as Vanguard FTSE Emerging Markets UCITS ETF (VFEM). Its top holdings include Tencent (0700:HKG), China Construction Bank (0939: HKG) and China Mobile (0941:HKG).

Broad ETFs are useful if you want to spread risk and don’t know enough about a single country’s economic prospects.

Just because an index is located in a particular country, it doesn’t necessarily mean you’ll get exposure to that country’s economy.

The UK’s FTSE 100, for example, contains several global companies and less than a third of total profits come from the UK.

The FTSE 250 index, which includes the 250 next-largest companies on the UK stock market, is more domestically-focused and includes companies like Auto Trader (AUTO), Rightmove (RMV) and Travis Perkins (TPK). An example of an ETF tracking this index is iShares FTSE 250 UCITS ETF (MIDD).

ETFs are a great and easy way to diversify your portfolio

2. Do I already have exposure?

It’s important to take a close look at the assets within an index and check whether you already have exposure via other investments in your portfolio.

If you invest in a biotech fund, you might want to steer clear of a specific biotech ETF as they could ultimately track the same companies.

Similarly, an S&P 500 ETF might not be suitable for someone who already has individual shares in Apple, Amazon and Facebook as these are among the big companies in the US index.

Morningstar puts ETFs and active funds into specific categories which can help you avoid duplication. For example, Source EURO STOXX 50 UCITS ETF (SX5S) is in the Eurozone large-cap equity category because it offers exposure to the 50 largest stocks in the Eurozone, including Siemens (SIE:ETR), Bayer (BAYN:ETR) and Allianz (ALV:ETR).

3. What are the fees?

Although ETFs are low-cost, the fees can vary widely. The average fee across Europe is 0.29%. A core FTSE 100 ETF is much cheaper than a niche single emerging market ETF because the FTSE 100 is less volatile and easier to track. The iShares FTSE 100 UCITS ETF (CUKX) has an ongoing charge of just 0.07%.

You can also get access to fees this low by opting for a similar non-ETF product – namely a tracker fund. BlackRock 100 UK Equity (GB00B7W4GQ69), which also tracks the FTSE 100, has an ongoing charge of 0.06%.

Unlike ETFs, trackers aren’t listed on a stock exchange and their units are typically priced at midday.

It is possible ETF fees could reduce even further in the future as products become more popular and competition among providers intensifies.

In the US, fees are trending towards zero, with some products having ongoing charges as low as 0.03%. Mellor says some providers engage in stock lending as a way to make money, or bundle their ETFs with other products.

Make sure you fully understand how an ETF works and how it tracks an index before investing

4. Is there a history of tracking error?

It’s important to look at whether the ETF is succeeding in its aim of accurately tracking a specific index or whether it has underperformed. Any difference between the return of the index and the ETF is called tracking error.

ETF providers will usually highlight a product’s tracking error in their factsheet through a percentage-based ‘standard deviation’ figure.

The higher a fund’s tracking error, the more likely it is to outperform or underperform its benchmark in any single period.

Reasons for tracking error include the rebalancing costs incurred when an index’s methodology requires a reweighting of its constituents. You sometimes get ‘cash drag’ when funds have to hold a portion of their portfolio in cash, for example to make dividend distributions. There can also be execution errors, issues with securities lending and when the ETF using a ‘sampling’ replication method.

According to Morningstar, ETFs which track emerging market equities tend to exhibit higher tracking error than those based on developed market large cap indices.

5. Does the ETF actually invest in the assets that feature in the index?

ETFs track an index in one of two ways: physical replication or synthetic replication.

Physically replicating products hold either all or a sample of the underlying assets that make up the index. Sampling is common when the index being tracked has a very large number of stocks or when some of the stocks are not very liquid.

Sampling helps keep costs down because there are fewer companies to buy or sell each time the index is rebalanced. However, tracking error is more likely because some of the index constituents are excluded from the product.

ETFs which use synthetic replication don’t hold the underlying assets. Instead, they replicate the performance of the index via swap agreements. A counterparty contracts to deliver the return of the underlying assets, minus a fee.

Tracking error tends to be less common in synthetic ETFs but there is a risk of the counterparty defaulting on their obligations, potentially exposing you to losses. Synthetic ETFs are backed by collateral to minimise the impact of a default.

Mellor says it doesn’t really matter which method of replication is being used, particularly when it comes to long-term investors. ‘Both deliver similar outcomes and have positives and negatives associated with them,’ he says.

Darius McDermott, managing director at financial adviser Chelsea Financial Services, claims synthetic ETFs are less transparent than physical ETFs because they don’t hold the underlying securities of the index.

‘Synthetic ETFs can be an easy way of accessing assets that are hard to actually own – like commodities. You just need to know the added risks involved,’ he says.

Source MSCI World UCITS ETF (MXWO)

This might suit someone new to investing

Source MSCI World UCITS ETF is a global product which aims to track the performance of the MSCI World Total Return (Net) Index. The index comprises 1,600 large and mid-cap stocks across 23 developed countries.

The US is by far the largest geographic exposure, taking up a 58.5% share. As a result, the largest holdings in the index are very similar to the S&P 500. It includes well-known names like Apple, Microsoft and Facebook.

In addition, the ETF gives exposure to Japan (8.6%), the UK (6.7%) and Canada, France, Germany and Switzerland (all at under 4%), along with a few other countries.

The index is well-diversified on a sector basis, providing exposure to the financials, IT, consumer discretionary, healthcare, industrials, consumer staples, telecoms, materials and energy sectors.

MSCI describes the index as a ‘building block’ around which investors can build a portfolio. For example, you could consider adding small cap exposure, emerging markets, specific sectors or ETFs which focus on particular stock characteristics.

Source’s Chris Mellor says the product could be suitable for someone who is new to investing. ‘The index is broad and consists of solid large cap holdings. If an investor doesn’t have a particular view on any region or sector, MSCI World offers a good base holding,’ he says.

Scalable Capital’s Adam French suggests the ETF could form part of a diversified portfolio for someone who is looking for broad equity exposure. However, he says the amount of equities an investor should typically hold in their portfolio varies greatly depending on their personal circumstances.

A key difference between Source’s product and other MSCI World ETFs is Source uses a ‘swap-enhanced’ structure.

It contracts with one or more banks who agree to pay any difference between the portfolio performance and the index performance, less any applicable fees. These contracts are known as swaps.

It invests in physical equities but there is a swap overlay to try to minimise tracking error. The fund uses multiple counterparties to reduce the potential impact of a default.

The ETF has a total return of 35.8% over the past year (to 23 January) and a five-year annualised total return of 14.4%, according to Morningstar. Total return is the combination of both share price performance and any income paid by the product.

NEXT WEEK:

Getting clever with ETFS: Quality, Size & Value

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.