Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTroubled recruiter could be at a turning point

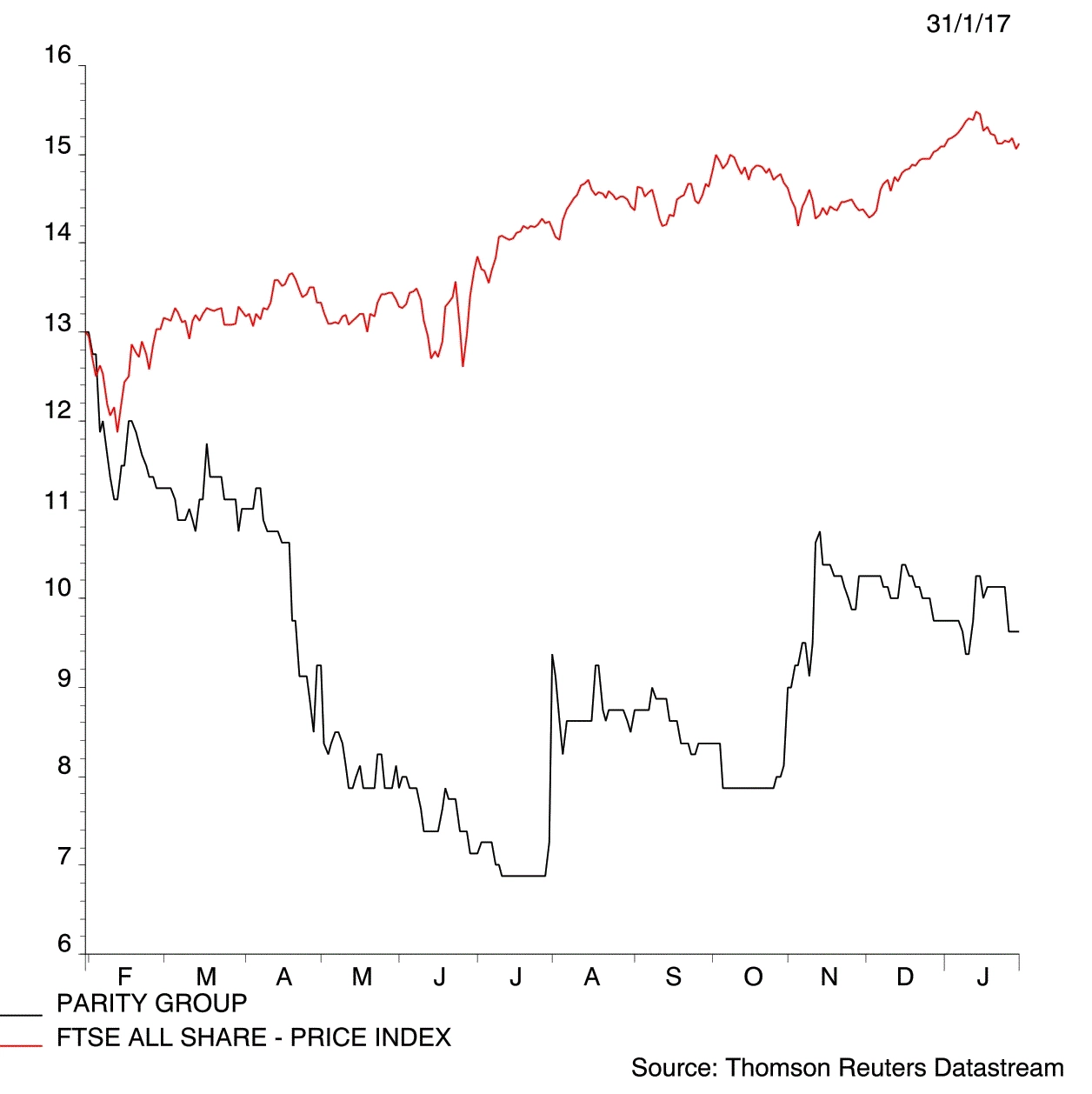

Recruitment agency and management consultant Parity (PTY:AIM) looks more interesting after an internal shake-up. Profit margins and cash generation are improving and we believe it may soon sell a non-core business, the proceeds of which could help repair its weak balance sheet.

Parity’s founder Philip Swinstead returned to the business in 2010 and tried to turn it into a digital media agency. The £9.8m cap business made several acquisitions which flopped. It wasted further money on due diligence for potential acquisitions but lost out to rival firms who acted faster.

The share price has been constrained by frustrated investors selling into any rally in a bid to reduce their holdings.

The group has spent years strangled by debt and pension obligations. It is making headway trying to fix these problems. Net borrowings were £6.5m as of mid-2016. The company has negotiated lower payments into its pension scheme which has a £1.6m deficit. It is unlikely to pay dividends in the near future, in our opinion.

Different this time?

Changes have been made to the way the business operates with the consultancy arm now the growth driver thanks to higher profit margins than plain recruitment.

Some of Parity’s biggest consultancy jobs are in the utilities sector, helping the water companies prepare for deregulation.

From April this year businesses in England will be able to select their own water provider, just like the electricity and gas market. That’s prompted the water industry to need more staff to ensure billing systems are up to scratch, pipes are fixed and data can be managed properly.

It also does a lot of work in the defence and health sectors. Specialist consultants are found via Parity’s recruitment division to undertake project work via its consultancy arm. Clients are happy as Parity’s fees are half that charged by the big consultants such as KPMG.

Potential asset disposal

Parity has told Shares it might sell a small division called Inition. Once a struggling 3D printing business living off £200-a-go contracts, Inition has become more successful in the topical field of virtual and augmented reality.

Management said any proceeds would be used for debt repayment and investment into the consultancy division.

![]()

Currently trading at 9.75p, Broker Investec believes the shares will jump 50% and hit 15p by the end of the year, saying it can’t ‘it cannot fly under the radar forever’. Parity is certainly looking interesting after a long period of underperformance. However, we want to see more evidence of both operational and financial improvement before turning bullish on the shares.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.