Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineAre motor retailers out of gas?

Quoted motor retailers’ shares have fallen heavily along with other domestically-exposed names following the vote for Brexit. Investors are pricing in a softer outlook for the industry, which already appeared to be cooling having enjoyed a sustained boom in new car sales. The Society of Motor Manufacturers and Traders (SMMT) is forecasting new car registrations to fall by 5% in 2017.

But there are opportunities for contrarian investors. Shares would steer any investors towards sector constituents with proven management, strong balance sheets and the ability to grow earnings through the cycle, both organically and through acquisitions.

Gas in the tank

Poor sentiment towards car retailers reflects expectations of a slower new car market in 2017 and 2018 and their exposure to big ticket-item purchases, as well as headwinds including sterling weakness and its unknown impact on manufacturers’ strategies as well as rising costs (national living wage, business rates, apprentice levy).

Most operators have highlighted a robust used car market, although newly listed used car specialist Motorpoint (MOTR) crashed following a profit warning (19 Oct ‘16) blamed on referendum-related uncertainty and margin pressure caused by falling residual used car values.

Zeus Capital’s automotive retail expert Mike Allen says ‘interest rates are likely to remain low for the foreseeable future, and we continue to believe the PCP (Personal Contract Purchase) cycle will result in greater activity levels potentially providing a shallower trough point vs. previous economic cycles.

‘A weaker new car market should also benefit future residual values further down the line, as it alleviates the margin pressure on 0 – 3 year-old cars, which has a greater impact on the operational gearing of motor retailers. Aftersales will continue to benefit from high levels of new car activity since 2011.’

Allen also believes comparisons to the 2008 downturn are overdone, since most companies have better balance sheets and systems and are also benefiting from shorter buying cycles and better earnings visibility thanks to PCP.

What is PCP?

PCP or Personal Contract Finance is a financing option for a prospective car purchaser which offers a vehicle for a variable deposit at a monthly fee. At the end of the (usually) three-year period, customers either hand the car back, make a ‘balloon payment’ and own the car outright, or put any equity they have in the car towards a new model.

Canaccord Genuity analysts Sanjay Vidyarthi and David Jeary highlight the potential for continued positive newsflow, at least into August’s interim reporting season.

Referencing the new car registrations forecasts, they note: ‘We maintain our view that the issue here is not about the headline level of decline, rather it is about whether the decline is a function of supply (less OEM push) or demand.

‘It is imbalance between the two which will cause greatest pain to the dealers through gross margin pressure. We think that there could be less push, given sterling weakness and the strength of demand in Europe, making a decline in the market more manageable for dealers.’

The analysts highlight the prospect of a strong March as demand is pulled forward ahead of changes to Vehicle Excise Duty (road tax) due to be implemented on 1 April, which will lead to a more onerous charging structure.

This, argues the broker, could provide a re-rating catalyst for underrated players including Lookers (LOOK), boasting one of the broadest spreads of brands in the industry, successful buy and build Vertu Motors (VTU:AIM) and the ambitious Cambria Automobiles (CAMB:AIM), where savvy CEO Mark Lavery has plenty of ‘skin in the game’ with a 40% stake.

Making sense of M&A

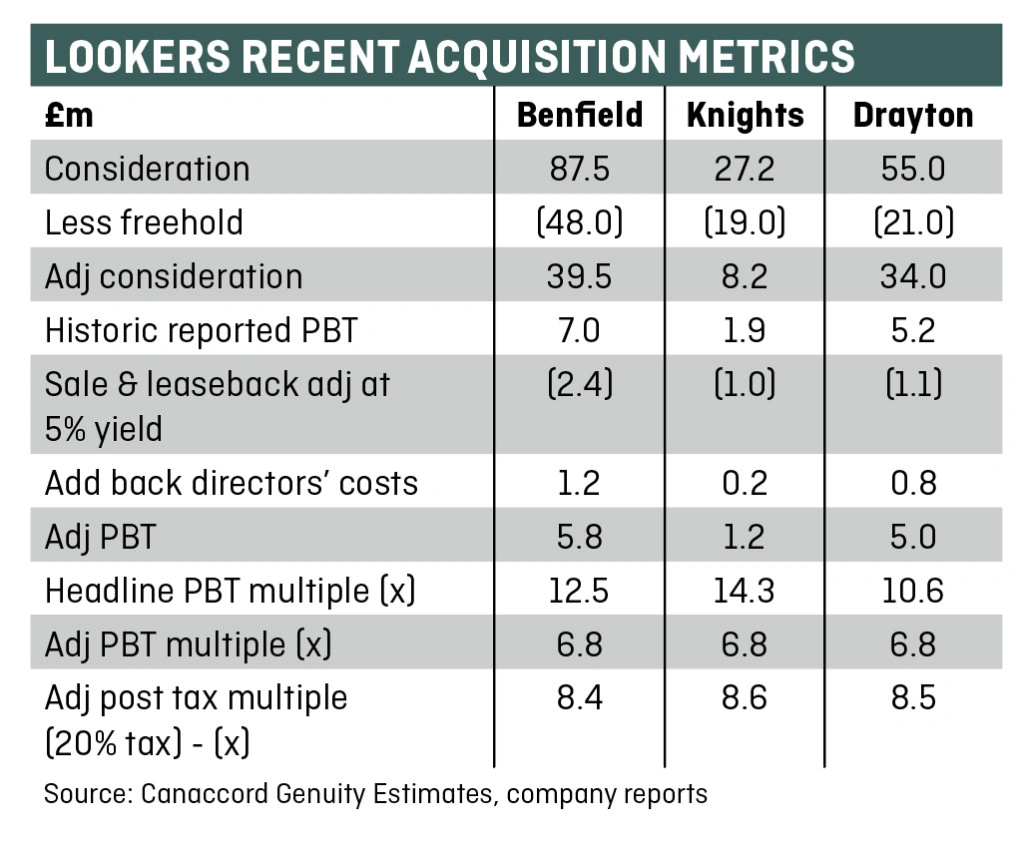

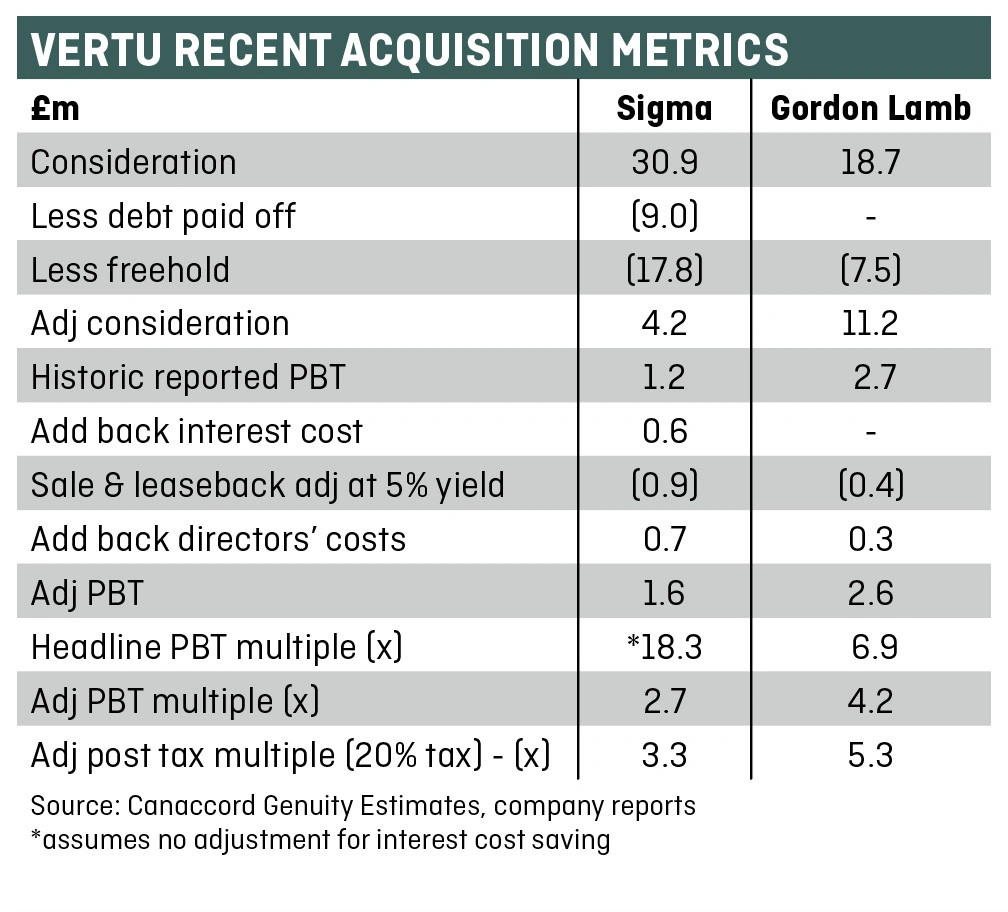

Canaccord’s Vidyarthi and Jeary also explain that ‘a common refrain among investors that we have met recently has been that the motor retailers are over-paying for acquisitions at the top of the cycle.’ However the pair has used annual reports filed at Companies House to dig into the financials of some recently acquired businesses.

Deconstructing recent Lookers and Vertu M&A, Canaccord argues that the headline multiples are mis-leading in the context of the freehold property that has been acquired as well as the potential profit upside.

For instance, with Lookers’ £55.4m acquisition of Drayton, by deducting the freehold property value from the deal cost as well as a notional rent, then adding back directors’ costs (since Lookers’ management has taken over the business), the pre-tax multiple drops significantly.

With Vertu Motors, steered by canny industry operator Robert Forrester, the broker illustrates how the multiples paid for 2016 acquisitions Sigma and Gordon Lamb are far lower, once freeholds are deducted and directors’ costs added back.

We’re positive on oversold-yet-growing operators with strong balance sheets including Vertu and Cambria, while global distributor Inchcape’s (INCH) overseas exposure in a weak sterling environment should provide insulation for tougher times ahead. (JC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.