Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFlash sale: five quality stocks to buy now

With global stock markets going through a rocky patch, triggered by the US central bank signalling the end of loose monetary policy, Shares believes now is an opportune time to pick up high-quality shares which may have been oversold in the broad market correction.

There is a lot of uncertainty and confusion even among professional investors and a good way to navigate this turbulent period is to focus on high quality businesses that can survive any economic scenario.

In this feature we have created screens to unearth shares which have been unduly punished in January’s market sell-off but display bucket loads of quality.

HOW DO YOU DEFINE QUALITY?

Before we get to the metrics which often characterise good quality businesses it should be remembered that many aspects of quality simply cannot be measured and require a qualitative assessment.

In other words, unlike the concept of value there is no universally accepted definition for quality.

Conceptually, quality implies resilience and pricing power of a company’s products which makes them stickier and harder to compete against.

Many years ago, Richard Branson’s Virgin brand launched a competing coke-flavoured drink to challenge the beverage giant Coca-Cola, but despite its best efforts and strong brand it couldn’t dislodge the 130-year-old beverage maker.

Coca-Cola’s largest shareholder is famed investor Warren Buffett who once said that if you handed him $1 billion to compete against the drinks business, he would hand the money back, because it wasn’t possible.

Buffett coined the phrase ‘moat’ to describe businesses which possessed certain characteristics (brands, scale, know-how) which made them more resilient and higher quality.

What Buffett also liked was the superior financial characteristics of high-quality firms – high margins, returns on equity and strong free cash flow generation.

Buffett’s thinking influenced the quality metrics which are used today to identify quality companies. For this article, Shares has used those metrics to search for quality firms, as well as applying one less well-known quality metric, being the gross profits to assets ratio.

WHY IS THIS RATIO IMPORTANT?

The gross profits to assets ratio is best associated with finance professor Robert Novy-Marx whose research showed that firms which exhibited a high ratio, considered to represent high quality, generated significantly higher average stock returns than firms which exhibited a low ratio.

It sounds like a very simple metric, but let’s dig into the moving parts. Gross profit is the value-add and defined as sales minus cost of sales. The gross margin is sales minus cost of sales, divided by sales.

A higher value-add margin reflects pricing power and arguably the success and stickiness of the product in the marketplace.

Large global brands like Nike and Apple can sell their goods at higher margins because their customers perceive them to be superior to alternative products.

The other side of the gross profits to assets ratio is totals assets, which represent all the capital investment required to run the business and generate sales.

Asset light businesses are generally lower risk because they generate higher cash flows which can be used to grow the business or pay dividends.

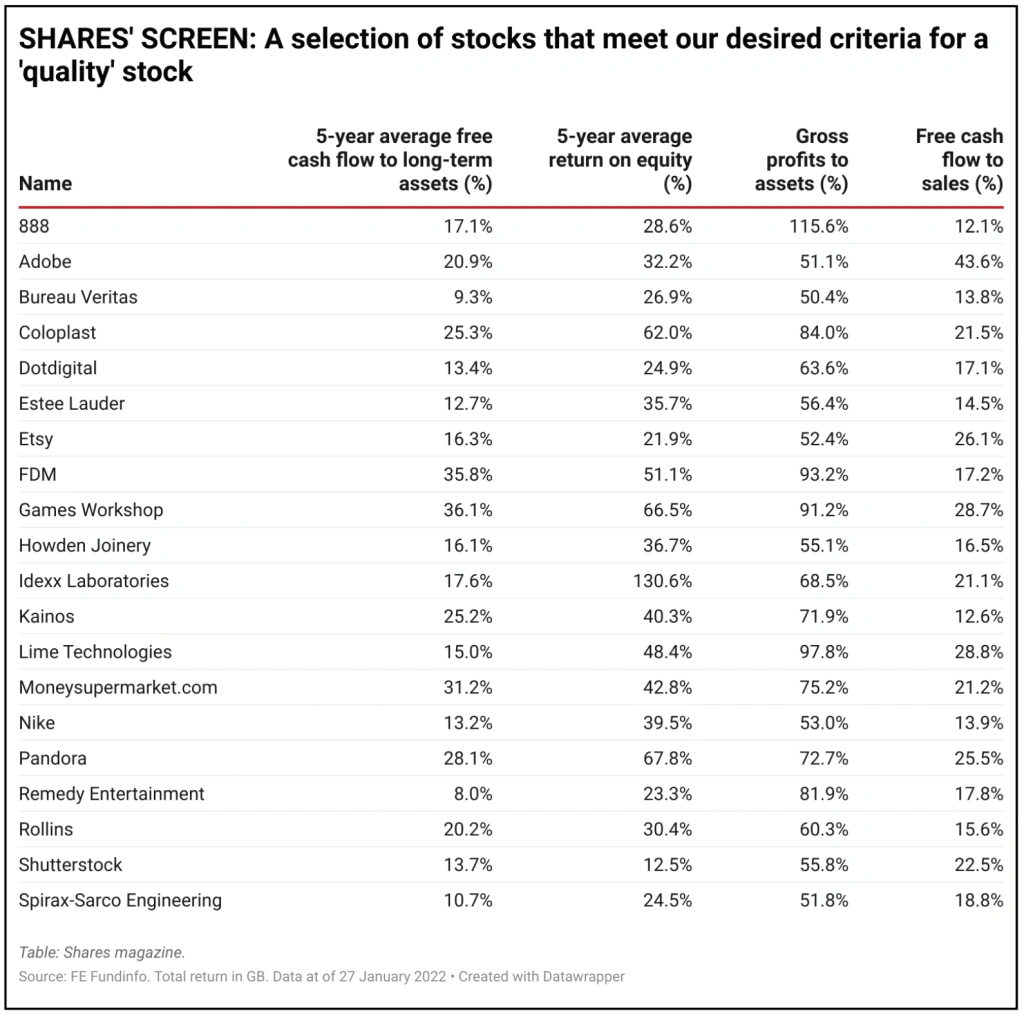

In essence, companies which have a high gross profit to assets ratio are considered high quality businesses. For the screening process we have looked for firms with a ratio above 50%.

SEARCHING FOR QUALITY

Shares has used Stockopedia’s system to create a screen which narrows the investment universe to the most attractive quality companies which have underperformed over the last six months.

This is the criteria we used:

– 5-year average free cash flow to long term assets >/= 5%

– 5-year average return on equity >/= 12%

– Gross profit to assets >/= 50%

– Free cash flow to sales >/= 12%

We filtered the list to only have the top quartile of companies on all these measures. We then further filtered the list to only include shares which have underperformed their local market over the last six months.

From this screen we have selected L’Oreal, Nike, Coloplast and Games Workshop (GAW).

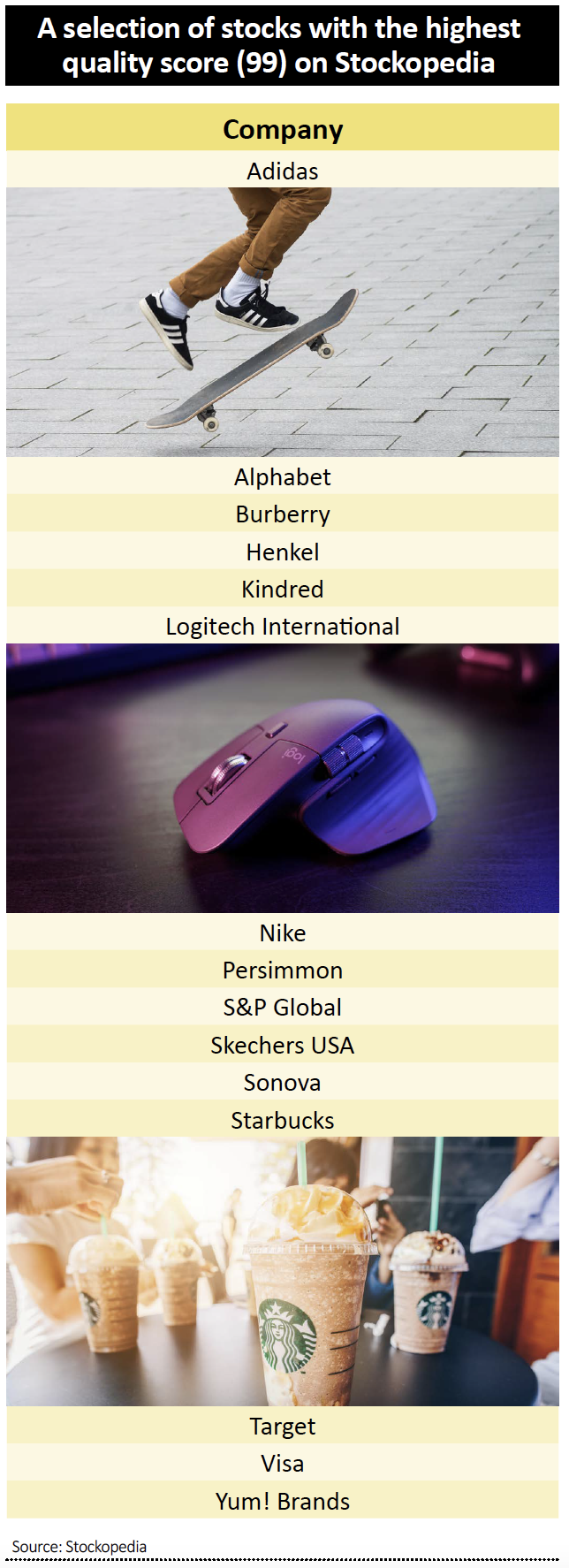

For extra thoroughness, we ran a second screen on the market using Stockopedia’s quality filter which scores companies across nine different quality metrics.

We looked at stocks scoring 90 or above, and again filtered by share price performance to only include companies which have underperformed over the last six months.

From this list we have chosen safety products expert Halma (HLMA) which has been caught up in the market sell-off, presenting a great opportunity to buy shares at a lower price in a fantastic company. It has a quality score of 91 out of 99 on Stockopedia.

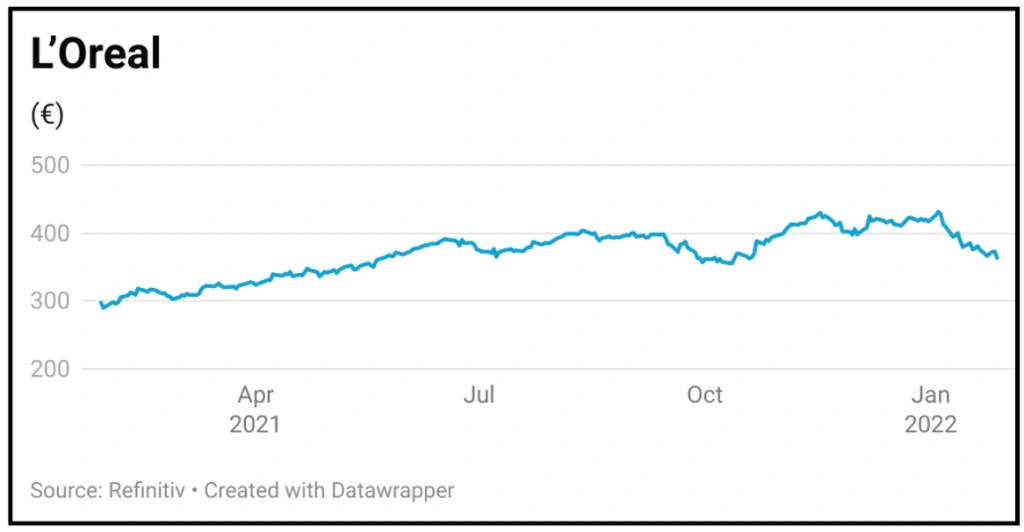

L’OREAL (OR:EPA)

Price: €375 – Market cap: €210 billion – (£174 billion)

We doubt L’Oreal needs much introduction, but it is probably worth explaining why it is such a good long-term earnings compounder.

The personal car and beauty market typically grows around 5% per year and this year is estimated to be worth more than $560 billion according to consultant Statista. The biggest market is the US, which accounts for 15% or just under a sixth of global demand.

In the first nine months of last year, L’Oreal generated sales of €23.2 billion, an increase of 18% on a like-for-like basis against single-digit growth for the market, with the US accounting for €6 billion or more than a quarter of group turnover.

The group throws off so much cash that it can afford to add bolt-on acquisitions to grow its market share while at the same buying back stock to improve its per-share returns.

With its attractive margins, strong brands, control of distribution and high spend on R&D, L’Oreal typifies the ‘strong moat’ kind of company which appeals to Terry Smith, who owns a big chunk of the shares in his Fundsmith Equity Fund (B41YBW7).

As Smith says, on the whole business returns don’t change: ‘Good businesses remain good, while businesses with poor returns have persistently poor returns’. [IC]

DISCLAIMER: Editor Daniel Coatsworth has a personal investment in Fundsmith Equity Fund

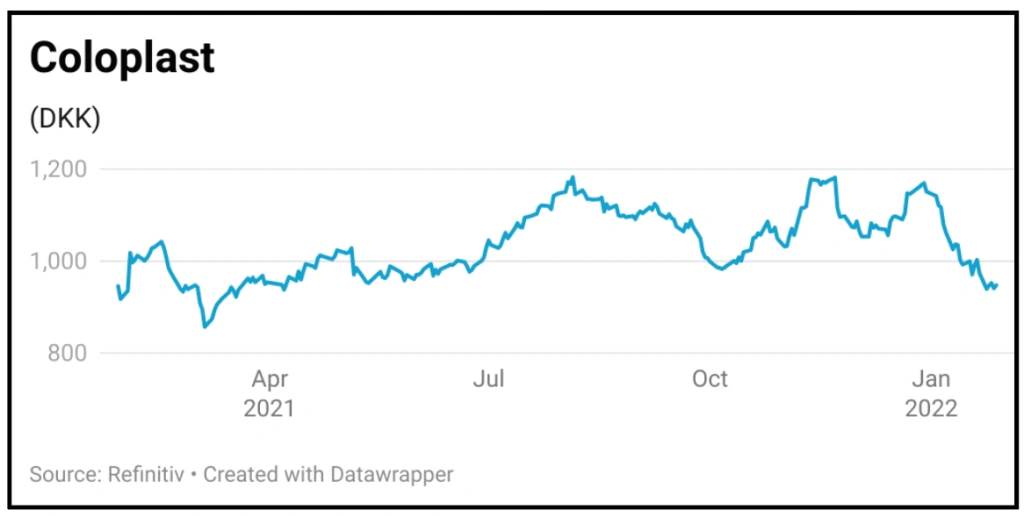

COLOPLAST (COLO-B:CPH)

Price: DKK 947.40 – Market cap: DKK 203 billion – (£22.7 billion)

Danish healthcare firm Coloplast is one of the world’s leading makers of products that make life easier for people with personal and private medical conditions.

Its businesses include ostomy care, continence care, wound and skin care, and interventional urology. Because its products are consumable and the conditions it treats are long-term, the firm has high visibility of revenues and earnings.

Sales are growing at 6% to 8% on an organic basis, with the recent acquisition of Atos Medical likely to push total revenue growth to 15% this year. Earnings before interest and tax is seen growing at a similar pace to the top line, generating a margin of over 30%.

Hospital activity is seen normalising in Europe and the US this year with growth in patients back to pre-Covid trends, which will drive sales of the firm’s chronic and continence care products.

Outside of China, emerging markets are expected to see double-digit growth in patient numbers helping to drive growth across the firm’s product range.

Christian Diebitsch, manager of the Heptagon European Equity Focus Fund (BPT3468), says he first bought shares in

Coloplast in 2004 and has always owned the stock since as it still fits his definition of ‘a high-quality growth compounder’. [IC]

DISCLAIMER: The author (Ian Conway) and editor (Daniel Coatsworth) have personal investments in Heptagon European Equity Focus Fund.

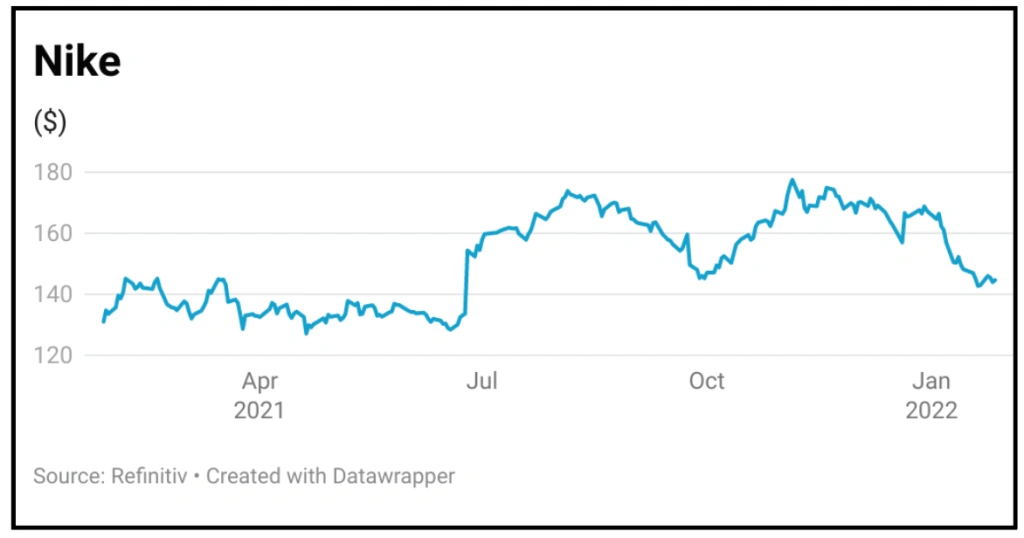

NIKE (NKE:NYSE)

Price: $143.99 – Market cap: $228.7 billion

Shares in sportswear giant Nike have been caught up in the maket sell-off, dropping 14% from $166.67 at the start of the year to $143.99.

That correction is unwarranted, as the company famed for its iconic swoosh logo has all the hallmarks of a high-quality business.

A company with a wide economic moat, Nike should remain one of the world’s preferred sportswear brands for years to come given its scale, brand strength and digital savvy.

It has a strong track record of value creation as measured by high return on capital employed and return on invested capital, metrics that indicate the presence of a sustainable competitive advantage.

The sportswear group generates premium pricing on products such as its performance athletic shoes, demonstrating its brand power.

Despite supply chain disruption, second quarter results (20 December 2021) beat expectations as Nike benefited from robust demand in its biggest market, North America, and a bumper Black Friday week.

CEO John Donahoe believes his charge is in a ‘much stronger competitive position’ than before the pandemic.

Increasingly selling products through its own stores and website to control brand messaging and margin, Nike has also made in-roads into the metaverse with the launch of the 3D immersive world of Nikeland on Roblox and the acquisition of virtual sneaker company RTFKT. [JC]

GAMES WORKSHOP (GAW)

Price: £77.35 – Market cap: £2.6 billion

Shares in fantasy games and miniatures maker Games Workshop have dropped around a third from their highs in September 2021.

Shares believes the factors driving the stock price lower are temporary and the fundamentals and quality of the business are as strong as ever, providing long term investors with a good buying opportunity.

Arguably, the company has suffered from its success and reputation for under-promising and over-delivering financial results.

Over the past 18 months analysts have increased their earnings forecasts a lot, significantly raising the bar for the company to beat.

Lapping strong prior year growth provided tough comparatives at the half year stage which, combined with higher shipping and employee costs, resulted in the company failing to beat expectations.

Rumbling customer complaints about Games Workshop’s hard-line approach to protecting its intellectual property also played a role in dampening investor sentiment towards the shares.

We believe investors should look beyond the short-term issues and focus on the high quality of the business which has delivered an average return on equity of 66% over the last five years according to Stockopedia. [MGam]

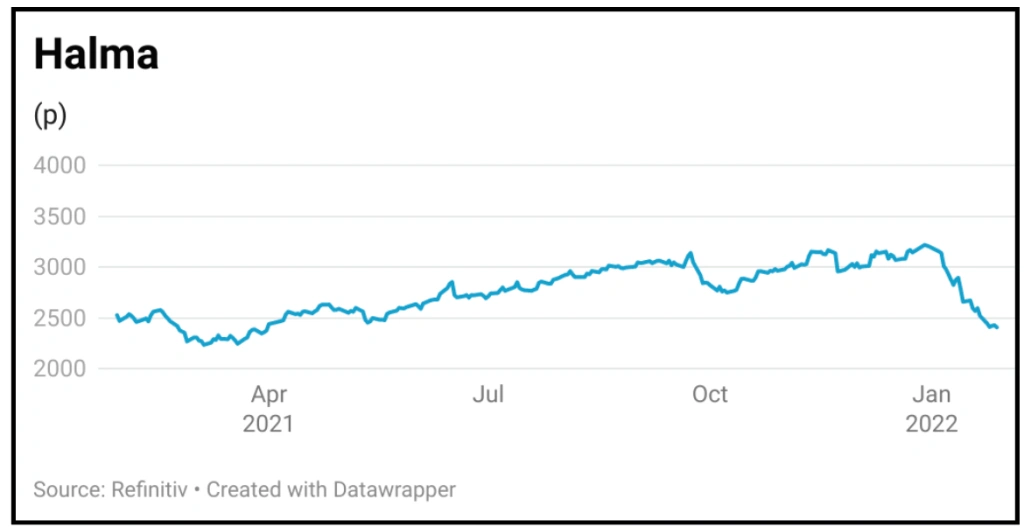

HALMA (HLMA)

Price: £23.98 – Market cap: £9.2 billion

Any time it is caught up in a wider market correction there is a good case for taking a close look at Halma with a view to buying the shares on the dip.

The designer of health, safety and environmental electronics equipment has delivered record annual results and consistent dividend growth for more than a decade, including through the pandemic, benefiting from its exposure to long-term growth markets which often enjoy regulatory drivers. In effect Halma’s kit often represents non-discretionary spend for its clients.

As well as investing heavily in research and development, the company has a strong track record of making small bolt-on acquisitions to bolster its market position. As such today it employs some 6,000 people in around 50 small to medium-sized enterprises operating across upwards of 30 countries.

Unsurprisingly these qualities have attracted a high market valuation – currently 37 times 2022 forecast earnings. However, you can buy the shares for 20% less than you could at the start of the year despite no negative news of any note from the company, with the weakness merely reflecting the market rotation out of expensive growth stocks.

History would suggest this is a buying opportunity which you should grasp with both hands, with Halma’s ongoing potential likely to

be rewarded over time. [TS]

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

Great Ideas

- Recovery or takeover likely to drive DotDigital shares higher

- Hipgnosis shares hit 11-month low on Neil Young / Spotify spat

- Revolution Beauty can still dazzle despite tough start on the market

- Play the momentum in high quality Bloomsbury Publishing

- Why Hargreaves is still a buy after rising 61% in less than a year

- Investors searching for real assets should snap up Industrials REIT

- A great way to play brighter prospects for Chinese shares