Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineRecovery or takeover likely to drive DotDigital shares higher

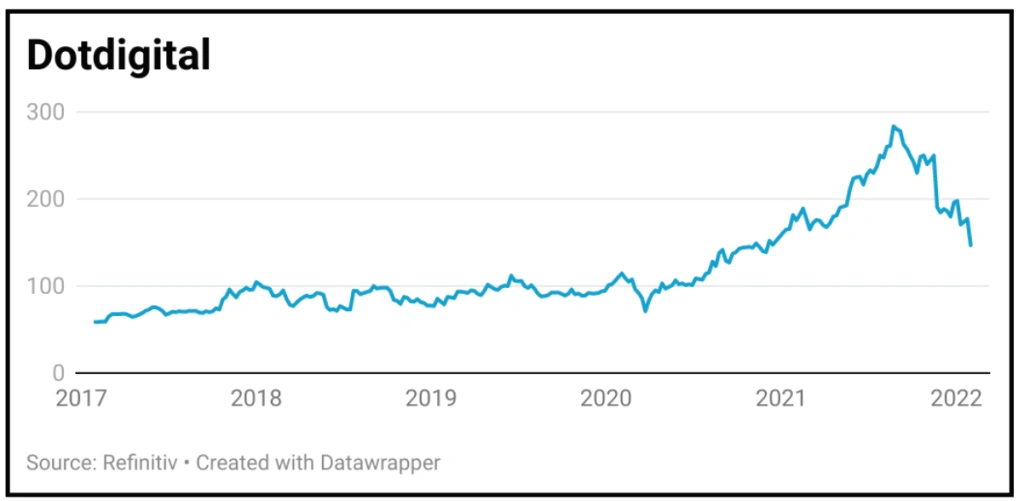

DOTDIGITAL (DOTD:AIM) 154.5p

Loss to date: 9.4%

Original entry point: Buy at 170p, 4 March 2021

It’s been a rollercoaster year for many technology companies yet DotDigital’s (DOTD:AIM) own ride has been particularly violent.

From gains of more than 70% in September 2021 versus our entry price to recent 20% losses, it is perhaps the sort of wild performance that some readers have come to expect from AIM-listed stocks.

We believe that AIM is less important in the DotDigital story than the pressure being placed on profit margins and the widely reported sell-off in tech and growth stocks.

The margins issue is not new. While DotDigital marketing department clients have embraced technology through the pandemic to improve customer relevancy, personalisation, and bang for buck, the wider use of lower margin SMS over social media or email platforms across the firm’s Engagement Cloud platform spooked investors. There is also wage inflation.

Last month’s update flagged these issues were getting back to normal, boding well for future growth. High recurring revenues, strong balance sheet and excellent cash generation appeal, and a share price recovery looks likely this year. If the shares stay at depressed levels, then DotDigital could become a takeover target.

SHARES SAYS: We continue to back the company and its shares, and investors should too.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

Great Ideas

- Recovery or takeover likely to drive DotDigital shares higher

- Hipgnosis shares hit 11-month low on Neil Young / Spotify spat

- Revolution Beauty can still dazzle despite tough start on the market

- Play the momentum in high quality Bloomsbury Publishing

- Why Hargreaves is still a buy after rising 61% in less than a year

- Investors searching for real assets should snap up Industrials REIT

- A great way to play brighter prospects for Chinese shares