Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineIf you're under 50 do you need to invest in bonds?

The bond market is under pressure. High inflation and the potential for rising interest rates have led to price falls, which may be the beginning of a tougher period for bonds. That’s after a terrific decade in which they have enjoyed abundant returns, thanks to loose monetary policy.

Bonds tend to be viewed as slow and steady investments which find favour with older investors looking to dial down risk.

But should younger investors in their 20s, 30s and 40s consider bonds as part of their portfolio? The answer to that depends on what these investors want from their savings. There are typically two reasons why investors might choose bonds: diversification, and income.

GOVERNMENT BONDS OFFER SAFETY

If you’re in the market for safety, government bonds, or gilts as they are known in the UK, might appeal. They’re viewed as safe because the chance of the UK Treasury failing to pay back borrowings is very low, though that doesn’t apply to every government around the world. Some people therefore invest in government bonds for diversification from a portfolio of stock market investments.

When stock markets are falling, gilts tend to move in the opposite direction, because these are seen as safe havens. Higher yield corporate bonds by contrast tend to have a higher correlation with stock markets, because these are loans to companies rather than the government, so they are also seen as a risky asset like shares.

A mixed portfolio of bonds and shares might suit younger investors who are quite cautious, and don’t want to see big fluctuations in the value of their portfolio.

BUT RETURNS ARE TYPICALLY LOWER

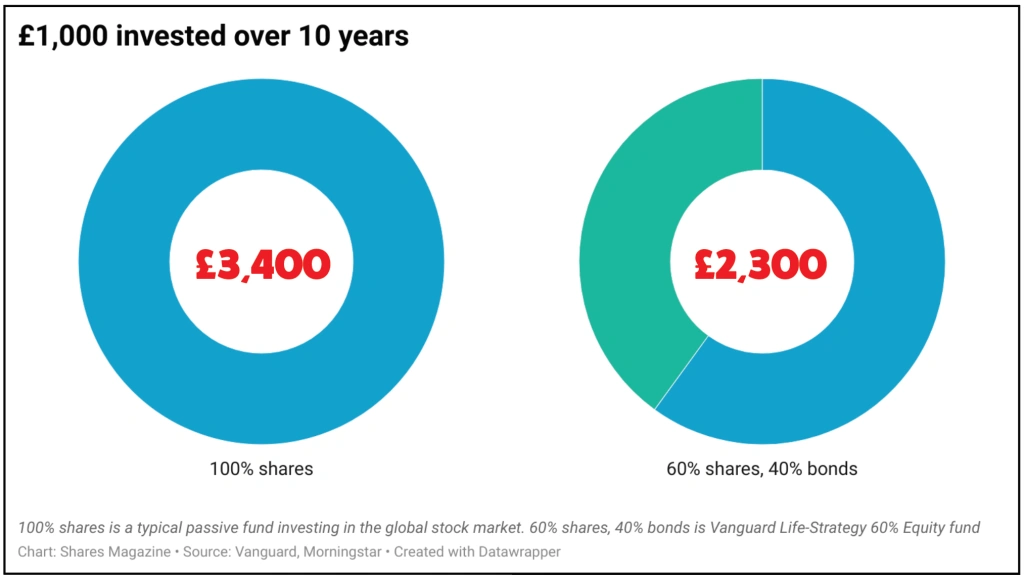

But there will likely be a price for this caution, in the total returns harvested by lower risk mixed portfolios over the long term. As an example of this, over the last 10 years, a portfolio of 60% stocks and 40% bonds (the Vanguard LifeStrategy 60% Equity fund) has turned a £1,000 investment into £2,300.

A pretty good result, but according to Morningstar a typical passive fund investing in the global stock market would have turned £1,000 into £3,400 given the same timeframe. Over longer periods, such as those enjoyed by younger investors, one would expect this differential to grow.

Nonetheless some more conservative younger investors might choose to invest in a mixed portfolio of shares and bonds, if they really don’t want the ups and downs of stocks alone. Likewise younger investors who are saving for a medium-term goal, like a house deposit, or children’s university fees, where they may have five to 10 years to invest, rather than 10 to 20.

THINKING ABOUT INCOME

Income is another important consideration which may lead investors to consider bonds. Gilts offer a relatively low income, because the UK government will almost certainly pay you back.

Corporate bonds have a higher yield, because there is a greater risk they will default, so they have to pay more interest to attract lenders.

That’s particularly the case with what are called ‘high yield bonds’, or less generously ‘junk bonds’, issued by companies which don’t have a strong credit rating. Some high yield bond funds are currently offering a yield of 5%, which is pretty attractive compared to cash for example, but the risks are much higher.

However, the vast majority of people in their 20s, 30s or 40s are unlikely to want income from their investments, as they’ll most likely have earnings from a job or self-employment. So this aspect of bond investment probably comes into its own when investors hit retirement.

THE MARKET CONTEXT

If you’re considering investing in bonds, it’s also worth considering the market context. Over the last 10 years, gilt prices have been driven up by low interest rates. That means if you buy a gilt maturing in 10 years’ time today, your return will be around 1% a year for 10 years, factoring in income and capital returns.

That will leave your money going backwards by 1% a year in real terms, if the Bank of England hits its 2% inflation target. In case you’ve been living in a bunker, the Bank hasn’t been doing that, with expectations that inflation will hit 6% or even 7% this spring.

So that’s not a particularly encouraging backdrop for government bonds, which set the tone for the rest of the bond market, leading some commentators to describe gilts as ‘return-free risk’.

One of the benefits of being a younger investor is that you usually have a long time until you need to cash in your investments, which allows you to take more risk in search of better performance.

Someone in their 20s, 30s or 40s would therefore only really invest in bonds if they wanted to dial down that risk for a smoother journey, and were happy to accept the likelihood of lower returns in the long run.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

Great Ideas

- Recovery or takeover likely to drive DotDigital shares higher

- Hipgnosis shares hit 11-month low on Neil Young / Spotify spat

- Revolution Beauty can still dazzle despite tough start on the market

- Play the momentum in high quality Bloomsbury Publishing

- Why Hargreaves is still a buy after rising 61% in less than a year

- Investors searching for real assets should snap up Industrials REIT

- A great way to play brighter prospects for Chinese shares