Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineRuffer is top performing capital preservation trust in market shake-up

A global equity markets sell-off at the start of 2022, driven by concerns over hot inflation and rising interest rates, together with growing tensions between Russia and Ukraine, has left many investors nursing significant portfolio losses.

Those with exposure to the technology-rich Nasdaq index across the pond have endured a particularly punishing 2022 so far, as monetary policy tightening, accelerated by inflationary pressures, has driven a market shift away from growth stocks and into value names.

The correction in equities is a salutary reminder for investors to ensure they hold a diverse portfolio of uncorrelated assets that hopefully don’t all move in tandem.

While equity markets have been weak this year, having exposure to bonds, gold and property would have been beneficial and this is where capital preservation funds can appeal. They position themselves defensively to reduce risk and volatility.

WHAT ARE CAPITAL PRESERVATION FUNDS?

Capital preservation funds are positioned to help investors avoid large losses while growing their wealth too, albeit more slowly than adventurous, more risk-tolerant funds.

The Association of Investment Companies’ flexible investment sector is home to a small band of capital preservation specialists that have done a good job at protecting investors’ money during tough markets historically, though they haven’t always avoided losses entirely.

These trusts can suffer losses during widespread sell offs and there is no guarantee they will always make you money. Yet their whole ethos is to fall by less than the market during a downturn, limiting your losses and protecting your hard-earned capital.

It is also important you understand that when equity markets rip-roar ahead, these funds are unlikely to keep pace, since they tend to have a lower exposure to shares than a standard income or growth fund.

PORFOLIO PROTECTION

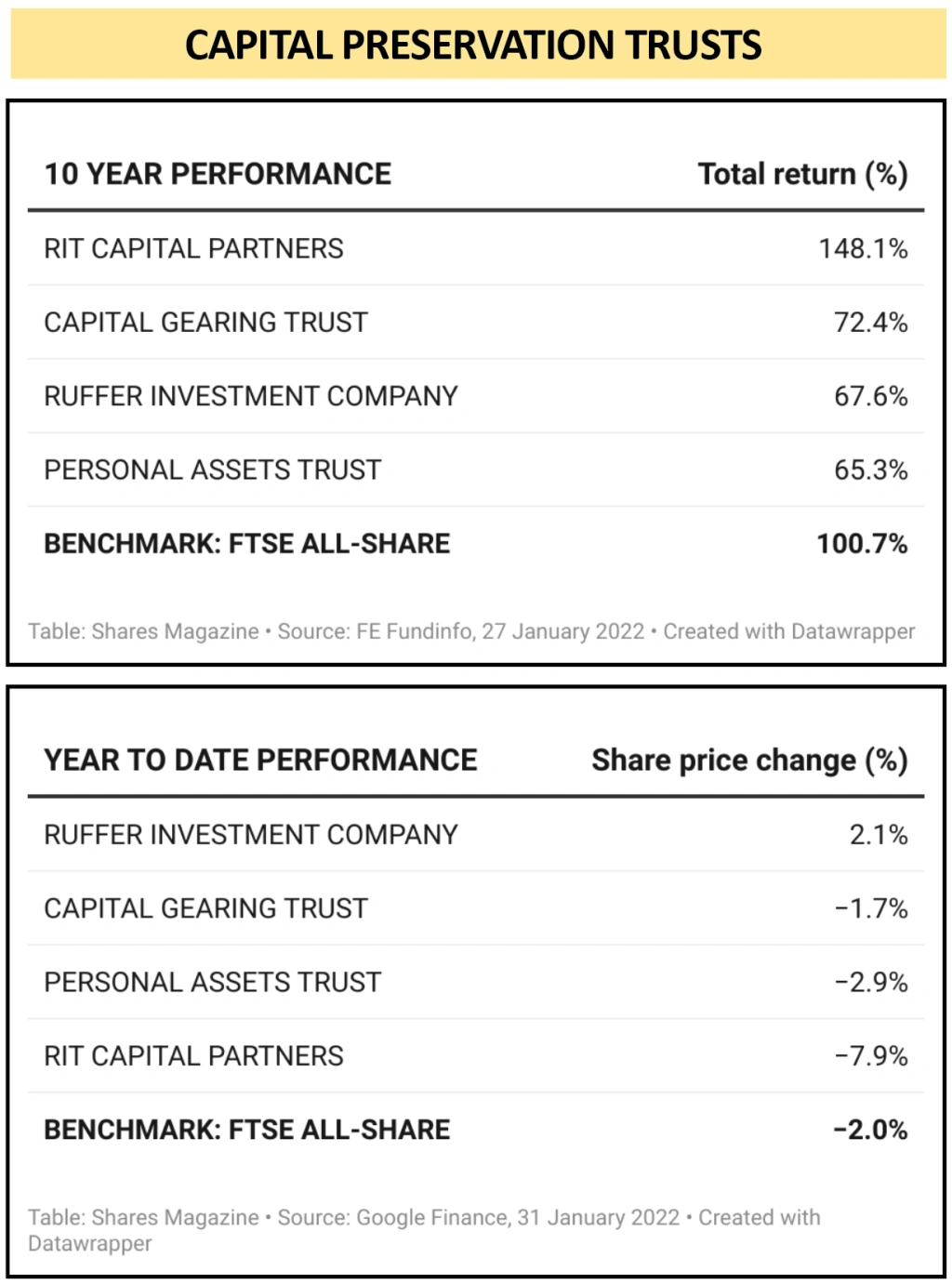

The main three investment trusts in the capital preservation space are Ruffer Investment Company (RICA), Capital Gearing Trust (CGT) and Personal Assets Trust (PNL), each one positioned to cope with the volatile markets, inflationary pressures and interest rate rise increases ahead. RIT Capital Partners (RCP) also has a capital preservation slant.

Based on data to 31 January, shares in Ruffer are up 2.1% year-to-date, ahead of the FTSE 100’s 0.4% decline but significantly outperforming the FTSE 250’s 8.4% slump and the 2% drop in the FTSE All-Share.

Shares in Personal Assets are down 2.9% and Capital Gearing is off 1.7% year-to-date, modest declines which have saved their investors from the sharper falls suffered by the FTSE 250 and from the main US indices.

It is important to note that investments shouldn’t be judged on such a short period.

HOW DO RUFFER AND PERSONAL ASSETS DIFFER?

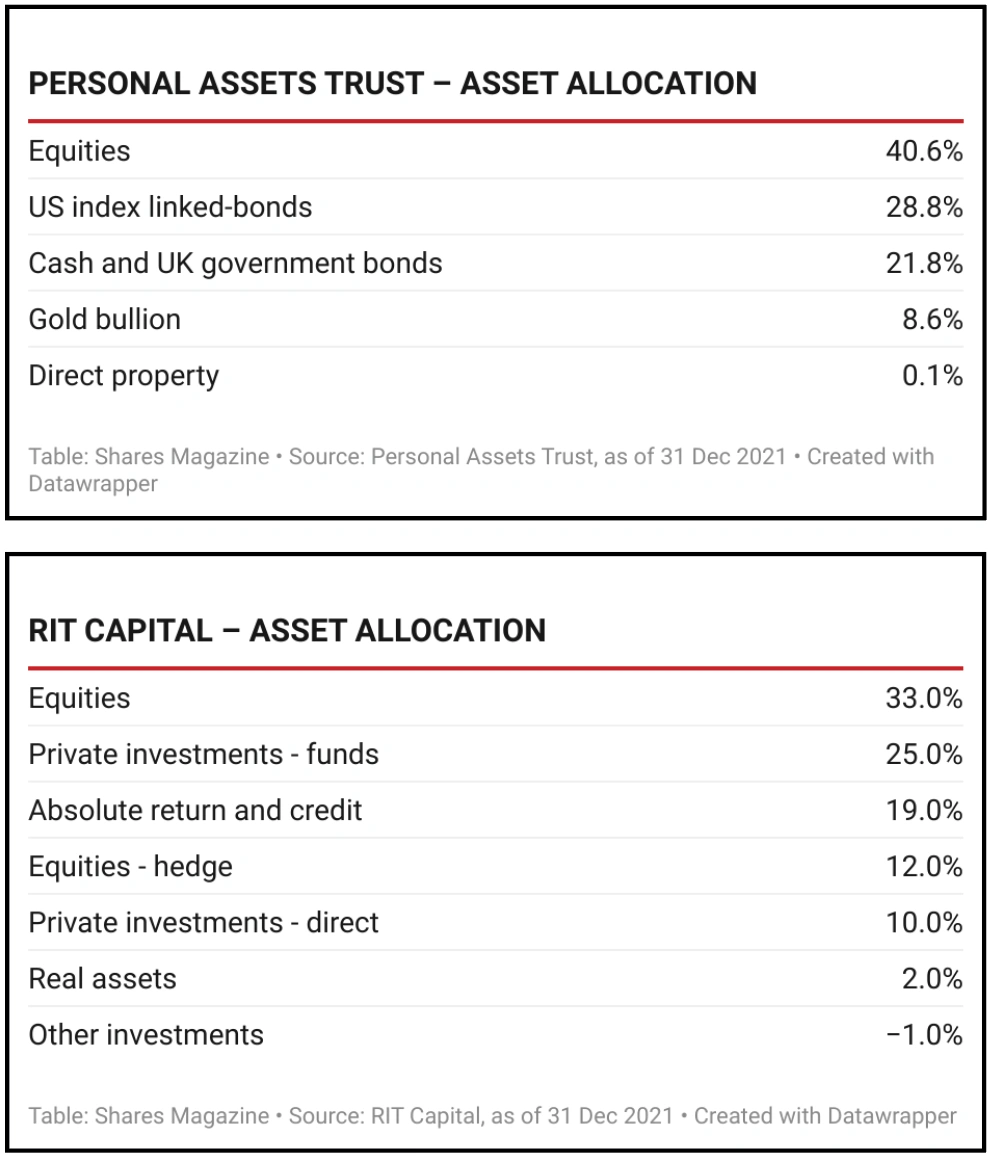

As the asset allocation breakdown tables reveal, 43.5% of Ruffer’s portfolio was in equities at last count, which is greater than the 40.6% Personal Assets has in shares in total.

Given the sell-off in equities seen in 2022 thus far, you might have expected the Ruffer’s portfolio to have suffered more than Personal Assets, whose investment policy is to protect capital first, with growth second on the priorities list.

After all, Personal Assets is aimed at the cautious investor who is more concerned about not losing money rather than making outstanding returns and it has allocations to companies with pricing power in defensive sectors. It also has the highest gold exposure of the trio and invests in low-risk US and UK government bonds.

However, Personal Asset’s top equity holdings include Microsoft and Alphabet, mega-cap growth names marked down during the recent rotation, as well as payments processor Visa. Personal Assets’ performance hasn’t been helped by the underperformance of consumer goods goliath Unilever (ULVR) either.

In contrast, Ruffer’s equity holdings were more skewed towards beneficiaries of the rotation towards value, including energy and financials names such as Shell (RDSB) and BP (BP.) and Lloyds (LLOY) and NatWest (NWG). Ruffer also holds GlaxoSmithKline (GSK), in demand after receiving a blockbuster bid for its majority-controlled consumer healthcare unit from Unilever.

WHAT ELSE IS IN RUFFER’S PORTFOLIO?

The core of Ruffer’s portfolio is formed of index-linked bonds, gold and equities, and the strategy has the flexibility to use derivatives (credit default swaps, equity put options and interest rate swaptions) to manage risk.

As Peel Hunt points out, Ruffer’s managers have been actively hedging the risk of rising rates and are ‘particularly concerned by the threat posed to traditional fixed rate bonds. This is reflected in the index-linked bonds within the portfolio (circa 38% of net asset value), and the value bias within the equity book’.

In the six months to December 2021, Ruffer’s NAV total return was 2.8% and the share price total return was 2.6%, with the largest performance contributor being index-linked bonds, which added 1.9%.

This return was boosted by some active trading and duration management during a period of rising inflation and interest rates in which the fund’s interest rate protection to offset the portfolio duration added 1.3% to performance.

Standout contributors from the equities book included Marks & Spencer (MKS) and Tesco (TSCO) amid growing private equity interest in the groceries sector.

As Ruffer explained in its latest update: ‘We enter 2022 satisfied that our all-weather investment strategy has fared well through a wide range of investment conditions in the last three years. However, for all investors things are likely to get more rather than less difficult from here. In order to protect and grow their savings, investors will need to focus on risk rather than return and adopt a multi-asset approach containing genuinely uncorrelated assets.’

WHICH TRUST HAS THE BEST LONGER-TERM PERFORMANCE?

Over a 10-year view, the best-performing wealth preservation trust is RIT Capital Partners (RCP) with a total return of 148.1%, comfortably ahead of the 100.7% haul from the FTSE All-Share.

Over the past decade, Capital Gearing has returned 72.4%, a smidgeon ahead of Ruffer with a 67.6% total return and Personal Assets Trust, which is up 65.3%.

WHAT IS RIT’S STRATEGY?

Like the three pureplay capital preservation specialists, RIT is a multi-asset portfolio that invests in credit, macro strategies and real assets.

However, it also aims to deliver long-term capital growth through the purchase of risk assets including equities and private companies, both directly and through funds.

Exposure to risk assets explains why it has been so successful during the bull market yet proved more vulnerable to this year’s correction than the more dedicated capital preservation plays. It is down 7.9% year to date.

WHAT IS CAPITAL GEARING’S STRATEGY?

Managed by Peter Spiller alongside Alastair Laing and Chris Clothier, Capital Gearing’s objective is to ‘preserve and over time to grow shareholder’s real wealth’, i.e. accounting for inflation.

Its portfolio is currently defensively positioned with a focus on inflation protection. It has a 34% allocation to index-linked government bonds, balanced by a 45% allocation to risk assets such as equities, property and alternatives. The remainder is invested in conventional government bonds, corporate debt, cash and gold.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

Great Ideas

- Recovery or takeover likely to drive DotDigital shares higher

- Hipgnosis shares hit 11-month low on Neil Young / Spotify spat

- Revolution Beauty can still dazzle despite tough start on the market

- Play the momentum in high quality Bloomsbury Publishing

- Why Hargreaves is still a buy after rising 61% in less than a year

- Investors searching for real assets should snap up Industrials REIT

- A great way to play brighter prospects for Chinese shares