Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineA great way to play brighter prospects for Chinese shares

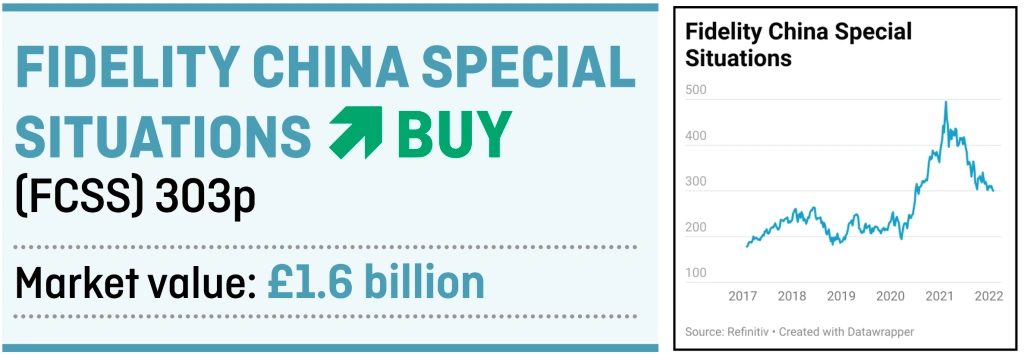

Exuberance towards China at the beginning of 2021 gave way to disappointment and pessimism as the year progressed. A lot of the bad news is now in the price and Chinese equities are starting to look attractive again, which means now is a good time to invest in Fidelity China Special Situations (FCSS).

The £1.6 billion investment trust provides exposure to the most dynamic companies in the greater China region. Its shares are trading on a 4.2% discount to the value of its underlying assets, and Chinese stocks have yet to recover from last year’s widespread sell-off, meaning you’re able to get in at a low level to play the rebound.

REASONS TO BE OPTIMISTIC

There are several reasons to be optimistic about the outlook for Chinese equities in 2022.

Valuations are starting to look appealing, and we are likely to be past the peak of government regulatory interference. The Chinese authorities also retain plenty of headroom to provide policy support. Recently they cut interest rates and accelerated approvals for infrastructure projects.

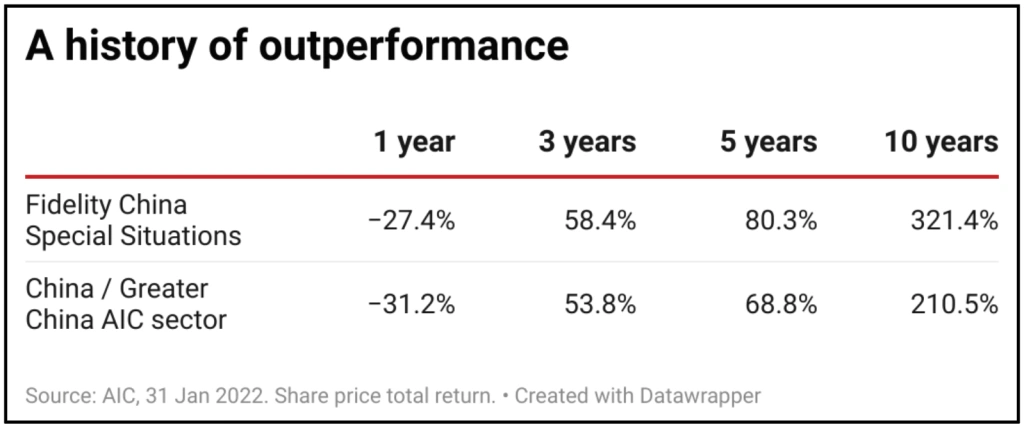

Although the one-year performance record for Fidelity China Special Situations has been uninspiring, returns over three, five and 10-year periods have been impressive. The trust has consistently outperformed the AIC Greater China sector over these periods.

REGULATORY OVERSIGHT DISSIPATES

The unexpected cancellation in November 2020 of Ant Financial’s stock market listing signalled the inception of a government campaign to increase its control over the private sector.

This increasingly draconian regulatory environment has encompassed private tutoring, e-commerce, social media, fintech, ride sharing and video streaming platforms.

Fidelity China Special Situations fund manager Dale Nicholls argues that from a timing and historical perspective, it is not the first time that we have witnessed heightened regulation in China.

‘We only need to cast our minds back to 2018 when the government felt the younger generation was spending too much of their time playing online games and as a result halted new gaming licences.’

Nicholls suggests we may now be past the peak of regulatory intervention. He says: ‘There is a good chance we are well into, if not past the peak of regulatory reforms, particularly within the technology sector – I would not expect the same degree of intensity that we saw last year and at the end of 2020 to continue.’

2022 is an election year in China. In November the Party Congress is scheduled to affirm Xi Jinping for his third term as party leader. For investors this suggests a period without significant unpopular announcements.

ATTRACTIVE VALUATIONS

We are entering a new phase in the Chinese economic growth story, where we can expect a more modest period of economic growth over the coming years.

This is very much in line with new government policy initiatives to engender a more balanced economy which is less dependent on fixed asset spending, but rather high-quality manufacturing and consumption.

The MSCI China index is currently trading on a 34% discount to the US market based on 12-month forward earnings.

Nicholls says: ‘History teaches us that these volatile periods usually offer the most attractive opportunities. Corporate earnings for the market are forecast to grow over 15% for the next 12 months, and the company’s portfolio should grow well above this level. Meanwhile, the market overall is trading on a price earning multiple that is attractive relative to history and relative to other stock markets globally.’

SCOPE FOR FURTHER POLICY SUPPORT

The end of 2021 witnessed a rush of economists downgrading their growth forecasts for China. However, as Nicholls highlights, ‘China is certainly at a different stage in the cycle with an easing bias, that history shows often supports markets. China’s central bank has more levers to pull to encourage growth after the slowdown of 2021’.

The mid to long-term Chinese growth outlook is robust given the expansion of the middle class. This has been facilitated by the increase in the urbanisation rate. In the most recent five-year plan, a target of 65% was established, up from the current level of 61%.

Within the urban population a significant cohort lack the Hukou (household registration rights and documentation). Government plans to expand the Hukou system will confer increasing rights upon a significant number of urban workers. This will act as another catalyst for consumption and economic growth.

This thesis is reflected in the composition of Fidelity’s portfolio that continues to have a large exposure to companies that are focused on growing domestic consumption, supported by the ongoing expansion of the middle class.

Beneficiaries of this trend aren’t just consumer stocks but also in areas like healthcare and technology that play into the theme of domestic consumption.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

Great Ideas

- Recovery or takeover likely to drive DotDigital shares higher

- Hipgnosis shares hit 11-month low on Neil Young / Spotify spat

- Revolution Beauty can still dazzle despite tough start on the market

- Play the momentum in high quality Bloomsbury Publishing

- Why Hargreaves is still a buy after rising 61% in less than a year

- Investors searching for real assets should snap up Industrials REIT

- A great way to play brighter prospects for Chinese shares