Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineStocks that have failed to recover from coronavirus

Stock markets around the world have staged a big recovery from their March lows, yet there are many individual companies that have stubbornly failed to find their feet.

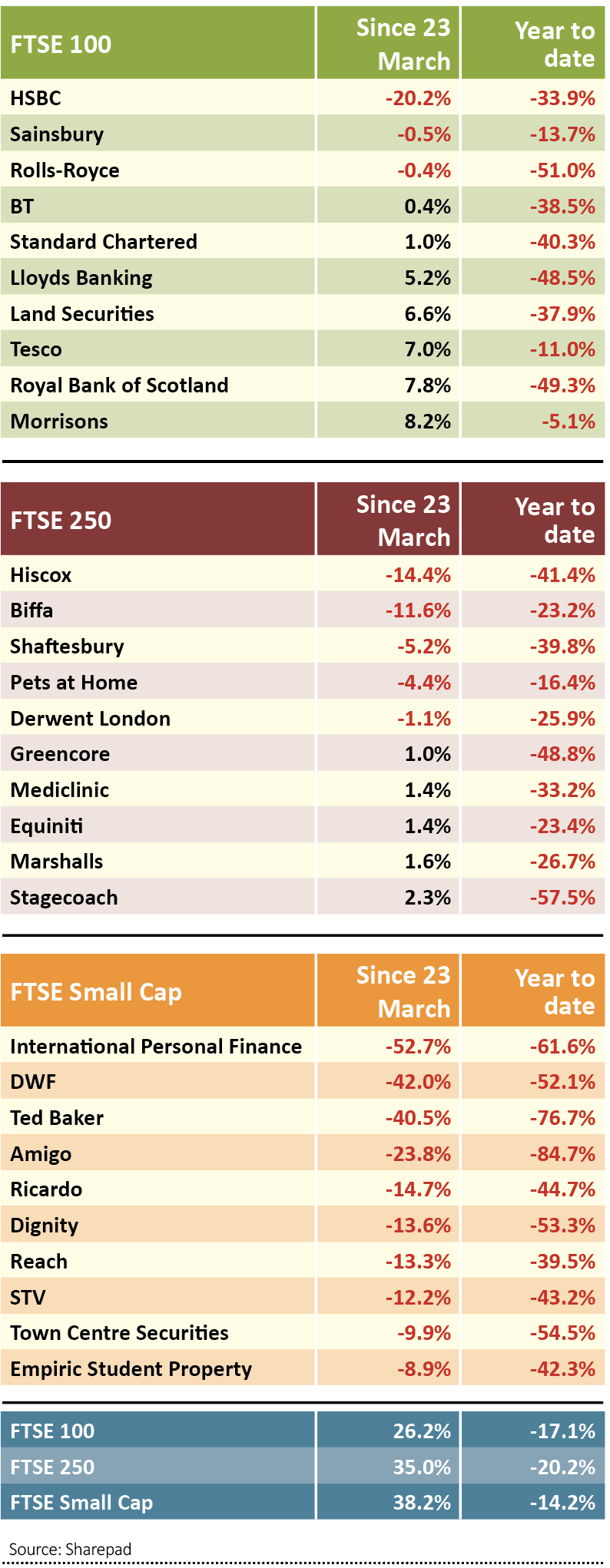

Supermarket chain Sainsbury’s (SBRY) and aircraft engines maker Rolls-Royce (RR.) are among a small clutch of FTSE 100 companies to have extended share price losses since 23 March, when the UK’s benchmark index hit its pandemic low of 4,993.89.

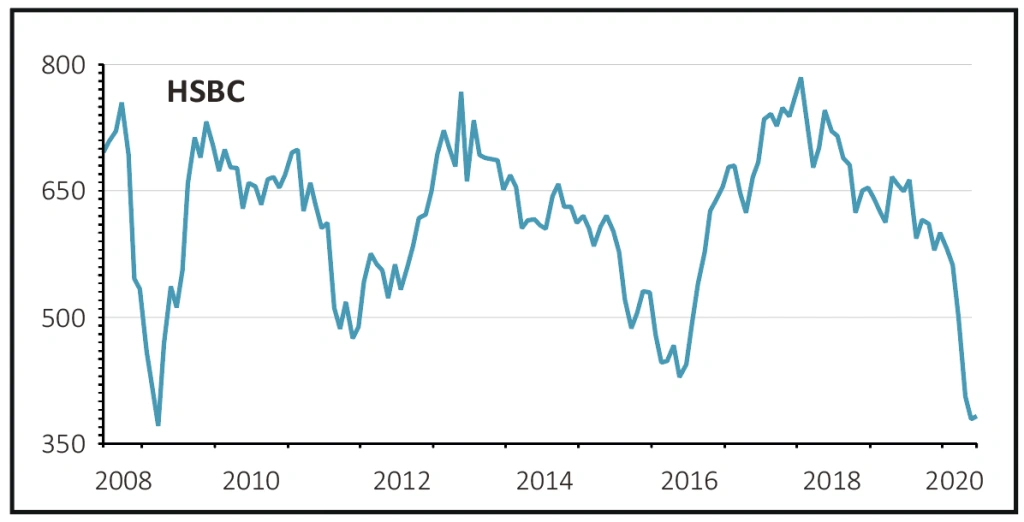

These laggards are led by HSBC (HSBA), the UK’s largest listed bank and one of the worlds’ biggest. Its stock has slumped more than 20% since March and now trades at depressed levels not seen since the global financial crisis more than a decade ago.

Combined, these three FTSE 100 companies have lost almost £21 billion in market value, albeit, most of this down to HSBC.

In all, 10% of FTSE 100 companies have returned less than 10% during the market’s recovery phase, while another 23 FTSE 250 companies have failed to meet this seemingly undemanding target.

Running the data across the wider FTSE All-Share, we find that more than 9% of stocks have returned less than 10% since 23 March, and 21 companies have seen their share prices decline, including insurer Hiscox (HSX), loans company Amigo (AMGO), waste manage firm Biffa (BIFF) and fashion chain Ted Baker (TED).

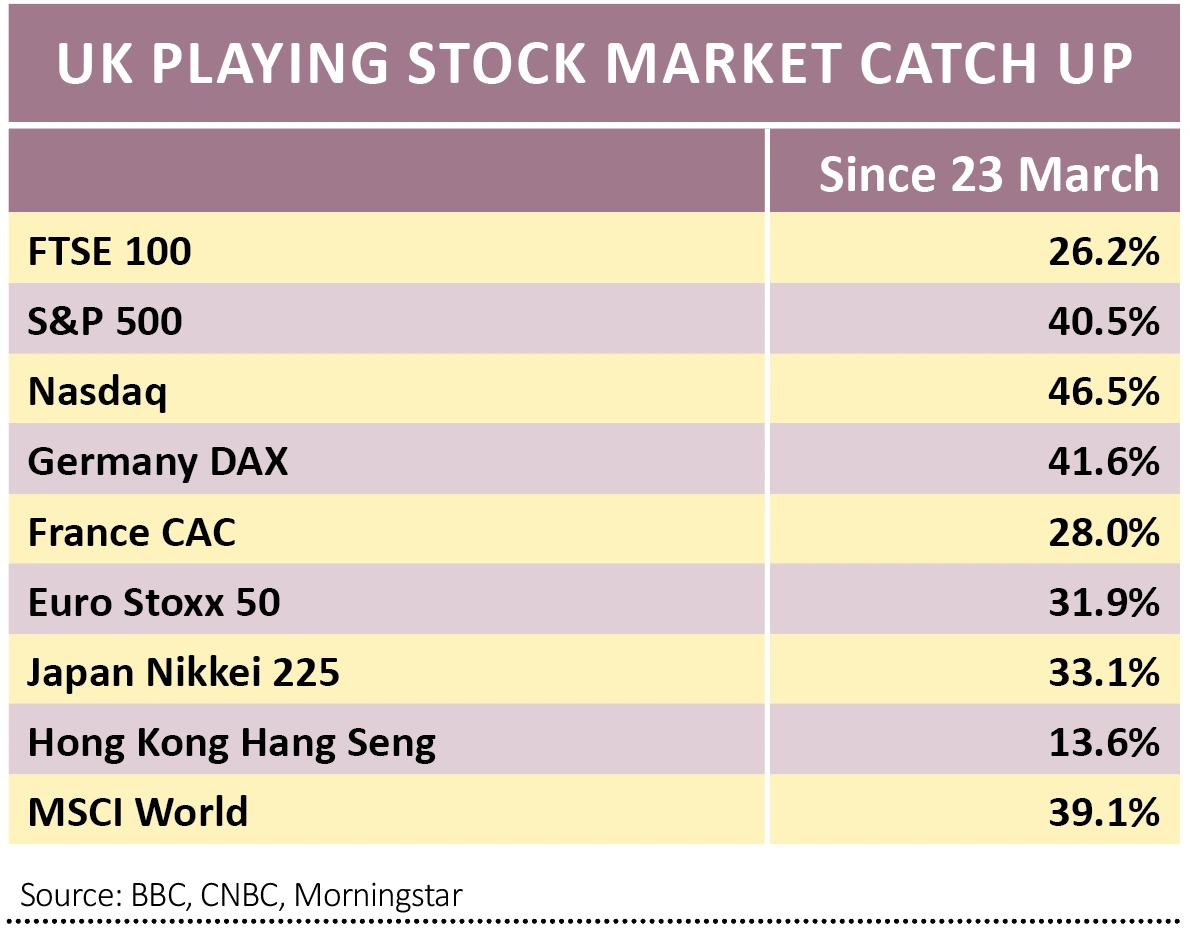

This is startling when we look at the recovery of the FTSE 100, and other global share indices. Since 23 March the UK benchmark has rallied roughly 25%.

That looks impressive on the face of it, but it is also the case that the UK has underperformed the majority of its global peer group.

This includes the US S&P 500 and tech heavy Nasdaq, Germany’s DAX, Japan’s Nikkei 225 and even the CAC 40 of France. The Europe-wide Euro Stoxx 50 is up 37% while the MSCI Global index, a measure of stocks market around the globe, has rallied more than 38%.

The culprit for UK’s dawdling pace of recovery probably lies, in varying degrees, to the widely held belief that Britain has not handled the pandemic terribly well, the squeeze on dividends, the collapsing oil price hitting BP (BP.) and Royal Dutch Shell (RDSB) – two of the UK’s biggest companies – particularly hard, and a litany of other factors both related and unrelated to lockdown.

At the company level, there are some very obvious reasons for poor share price performance. For example, given that Rolls-Royce makes most of its profit from maintenance and servicing of engines, having entire fleets of planes grounded for weeks on end was always going to exact a heavy toll.

At HSBC, quarterly profits have halved while provisions for credit losses could hit £11 billion this year, the bank has warned. But perhaps more importantly, increasing numbers of investors are deciding there is little reason to own bank shares without income, with dividends on hold for the foreseeable future thanks to an edict from the regulator.

With others, the rationale for poor returns since March, are not so clear. This might tempt some investors to go bargain hunting for stocks at near-term discounted prices. That strategy is well-worn and can unearth opportunities gems as long as investors do proper research. But beware, those that do not run extensive financial and operating litmus tests on potential bargains risk losing their shirts.

We have seen a bizarre, and extreme, example of fuzzy investment thinking in the US recently, where financially-distressed car rental company Hertz saw its share price jump five-fold in a week. That is despite the claims from bondholders on its beleaguered assets making the equity all but worthless.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Premier Foods is in a sweet spot as it breathes new life into the business

- Lam Research is a best in class stock you need to own

- Buy Touchstone now as it gears up for a big increase in production

- Microsoft shares hit new all-time high as it sees little coronavirus impact

- Fresh pork-to-poultry supplier Cranswick continues to sizzle

- Polar Capital’s shares are up 10% since we said to buy a week ago