Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFive funds beating the market by a significant margin

While many investment funds have recorded heavy losses this year, there have been a few outlier funds which have not only recorded a positive return when looking at the three months to 31 May, but in some cases have also outperformed their benchmarks by a decent amount.

We spoke to various managers of funds in the UK smaller companies, Europe ex-UK, Asia ex-Japan, strategic bond and absolute return sectors to see how they managed to come out on top and stay ahead of the market.

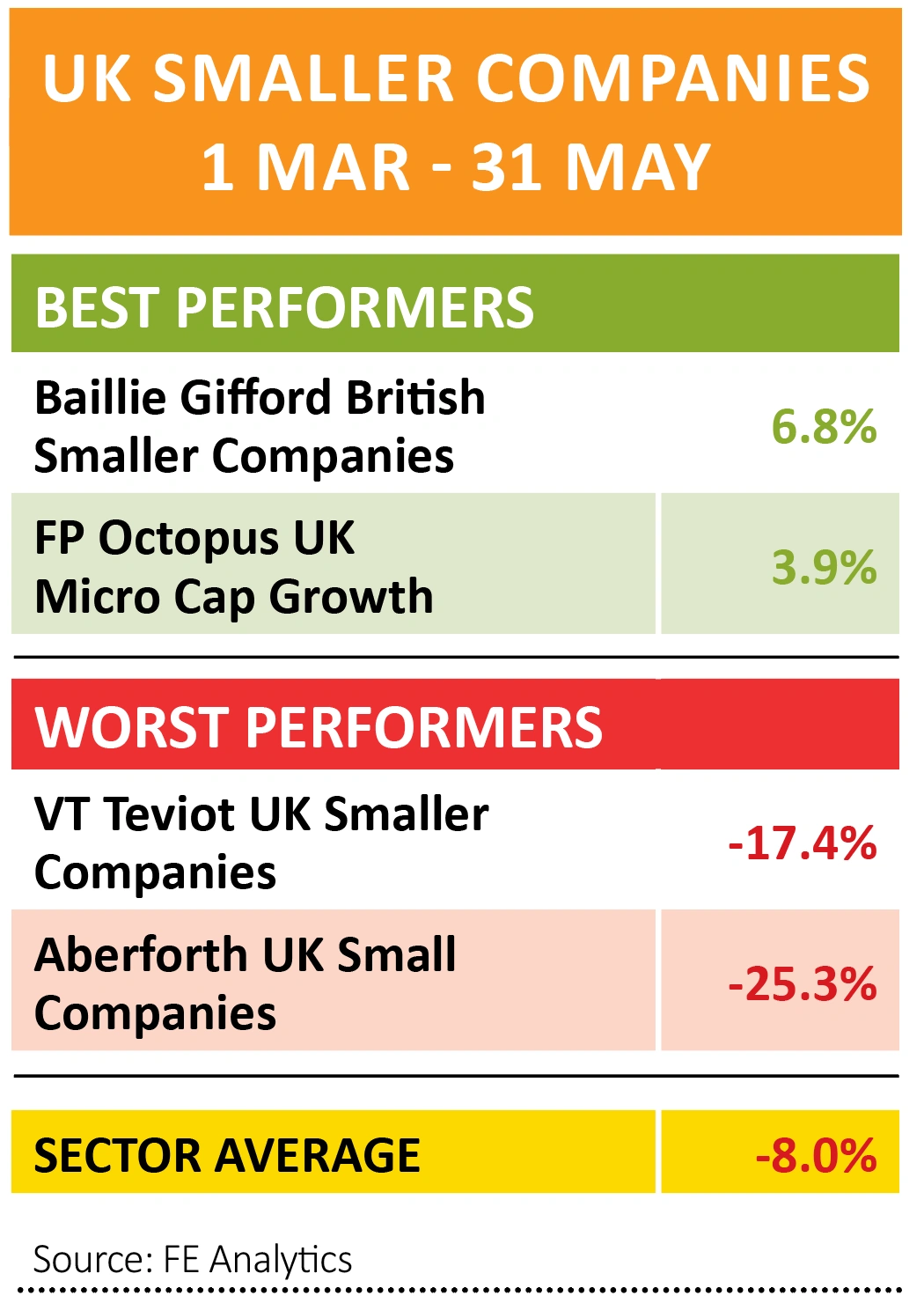

UK SMALL CAP FUND SOARS AHEAD

UK small caps have struggled this year, with the UK Smaller Companies sector having fallen by average of 8% in the three months to 31 May, according to data by FE Analytics.

We chose to analyse this period because it encompasses the worst of the market sell-off and a good chunk of the recovery, thus showing if certain sectors have fully bounced back or still have a lot of catching up to do.

Only two funds in the sector have delivered a positive return in the period – Baillie Gifford British Smaller Companies (0593135), which has returned 6.8%, and Octopus UK Micro

Cap Growth (BYQ7HP6), which has returned 3.9%.

Richard Power, manager of Octopus UK Micro Cap Growth, tells Shares the fund built up a 20% cash position going into the coronavirus crisis, which it was then able to deploy when markets became inefficient.

He estimates this move added between 6% and 7% to performance, while the fund’s sector positioning has also provided a boost. ‘Our sector skew has put the fund in a strong position. There are certain characteristics we look for, such as high levels of recurring revenue, which has naturally led us to sectors like tech. We’ve also never had much exposure generally to the consumer, which has helped.’

Some of the stocks he highlights include diagnostics firm Novacyt (NCYT:AIM), which the fund bought in February at 160p and has since sold most of the shares for 420p to 500p each.

Power also highlights another diagnostics stock, EKF Diagnostics (EKF:AIM), which the fund added to when it dipped as low as 18p in March and has since recovered to around the 50p mark.

While other drivers of performance include media company Future (FTR), which the fund managed to buy around the 600p mark with the shares having since recovered to over £12, as well as pharma firm Clinigen (CLIN:AIM), online education provider Wey Education (WEY:AIM) and a small holding in online competitions firm Best of the Best (BOTB:AIM), whose recent success has attracted takeover interest.

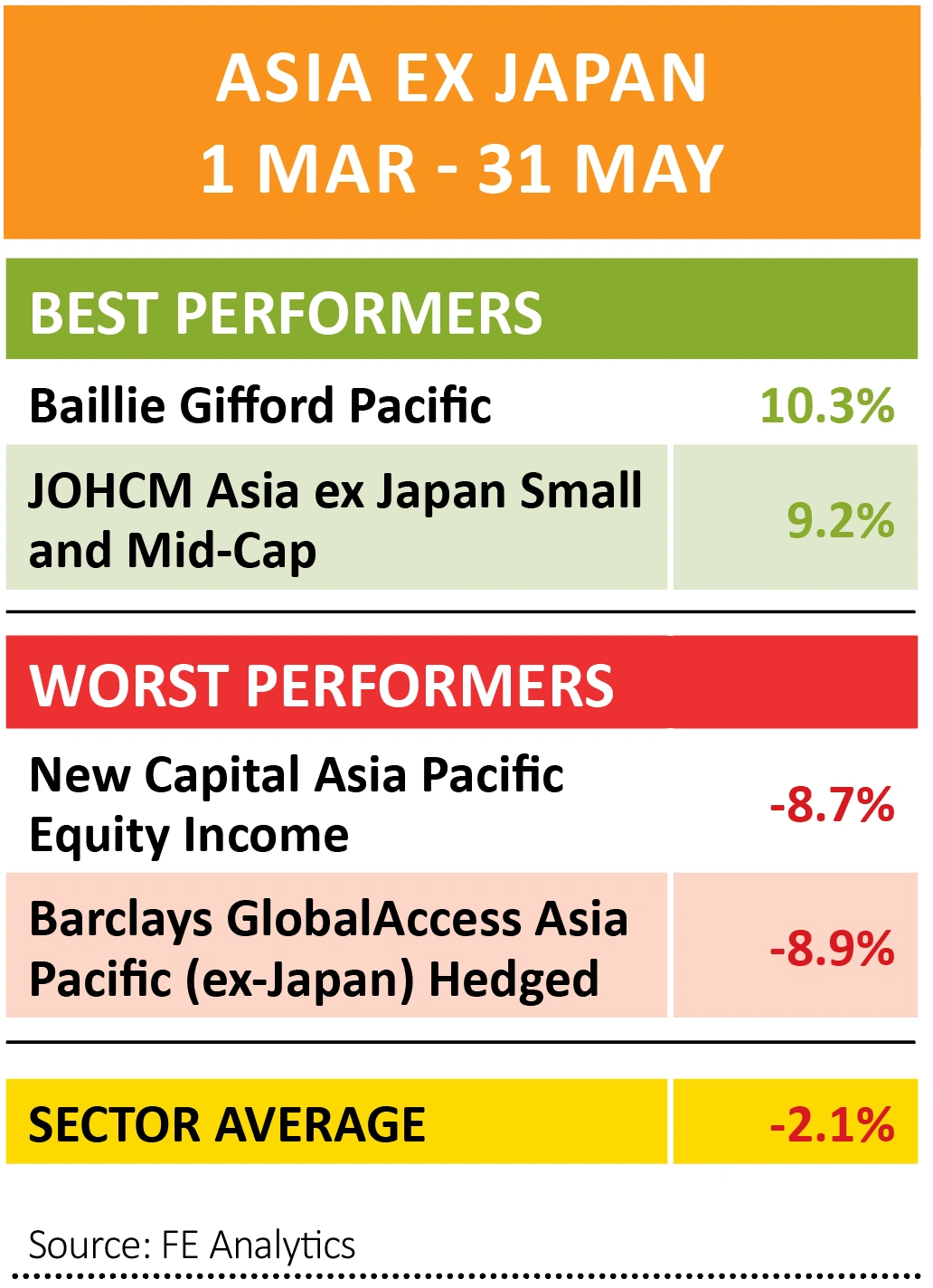

A MARKET-BEATING ASIA FUND

In Asia, one of the few funds that has come out well ahead of its benchmark is JOHCM Asia ex-Japan Small and Mid-Cap (B6R5LS4), which has returned 9.2% in the three months to

31 May, compared to -2% for its MSCI Asia ex-Japan benchmark.

The fund’s manager, Cho Yu Kooi, put outperformance down to being ‘very overweight’ Chinese software stocks, as well as owning companies which are benefitting from the ‘increasing localisation’ of Chinese hardware and software technologies.

Kooi explained to Shares: ‘The US government has continued to tighten the screws on US technology exports to China. This has spurred Chinese state-owned entities and the private sector to replace existing hardware and software technologies, the majority of which have US origin, with non-US and preferably Chinese ones.

‘In addition, China is speeding up the build-out of its 5G networking and data centre infrastructure which has also boosted our technology holdings.’

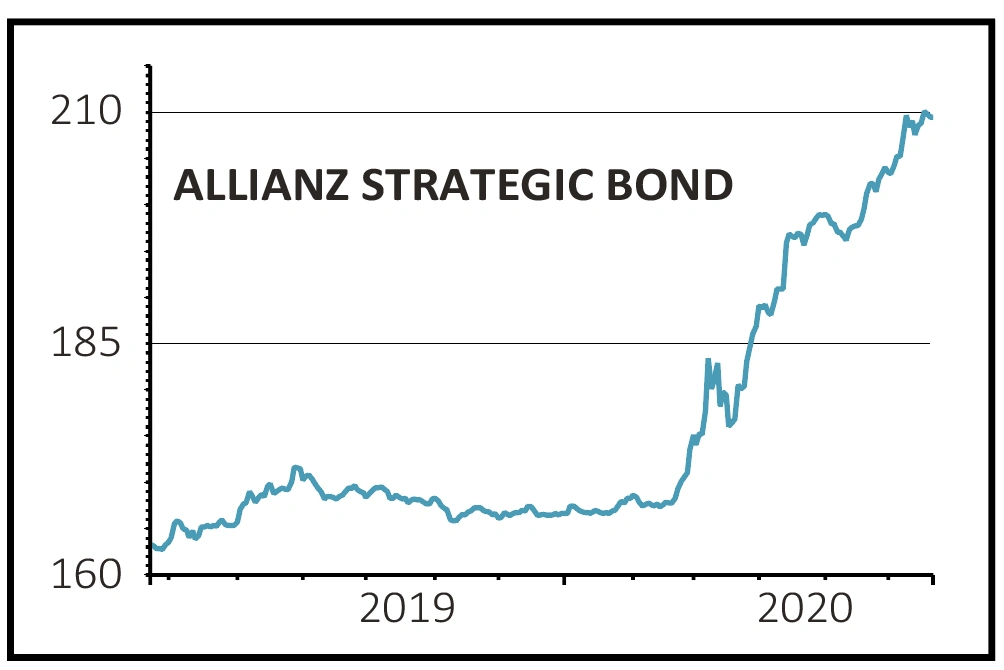

THE BOND FUND OUTPERFORMER

One investment sector that has seen a real anomaly in terms of performance from a fund is strategic bonds. In the three months to 31 May, Allianz Strategic Bond (B06T936) has returned a whopping 18% compared to 4.2% for the next best, Carmignac Unconstrained Global Bond (B46K5H3) – while the average for funds in the sector has been -1.8%.

Going into the coronavirus pandemic, Allianz portfolio manager Mike Riddell tells Shares he moved the fund’s positioning in February to as defensive as its mandate allowed, particularly in the credit and foreign exchange markets, ‘where we saw the largest mispricing and the potential for gains if our very negative macroeconomic outlook materialised.’

He explains: ‘Valuations eventually moved very sharply in March. We first closed out our defensive positions, and then following the announcements of enormous QE programmes, we decided to position the fund aggressively “risk on”. We expected a rapid bounce-back in economic activity in the second half of 2020 given the huge stimulus measures, and also that following the slump in oil prices, the world had near free energy.

‘The “risk on” positions were specifically via long positions in credit, given this is where we saw the most distress.’

Riddell says he took the portfolio from ‘outright’ short credit in February, to having about 65% in investment grade corporate bonds and 10% in Eurozone high yield bonds. This helped the fund perform well as markets bounced back in the second quarter.

He adds: ‘We also expect central bank purchases to prove supportive for inflation expectations, and amid the market pricing of deflation for 2021, we added long positions in US inflation and more recently euro inflation, where this is partly offset by short UK inflation positions given the UK market appears exceptionally expensive.’

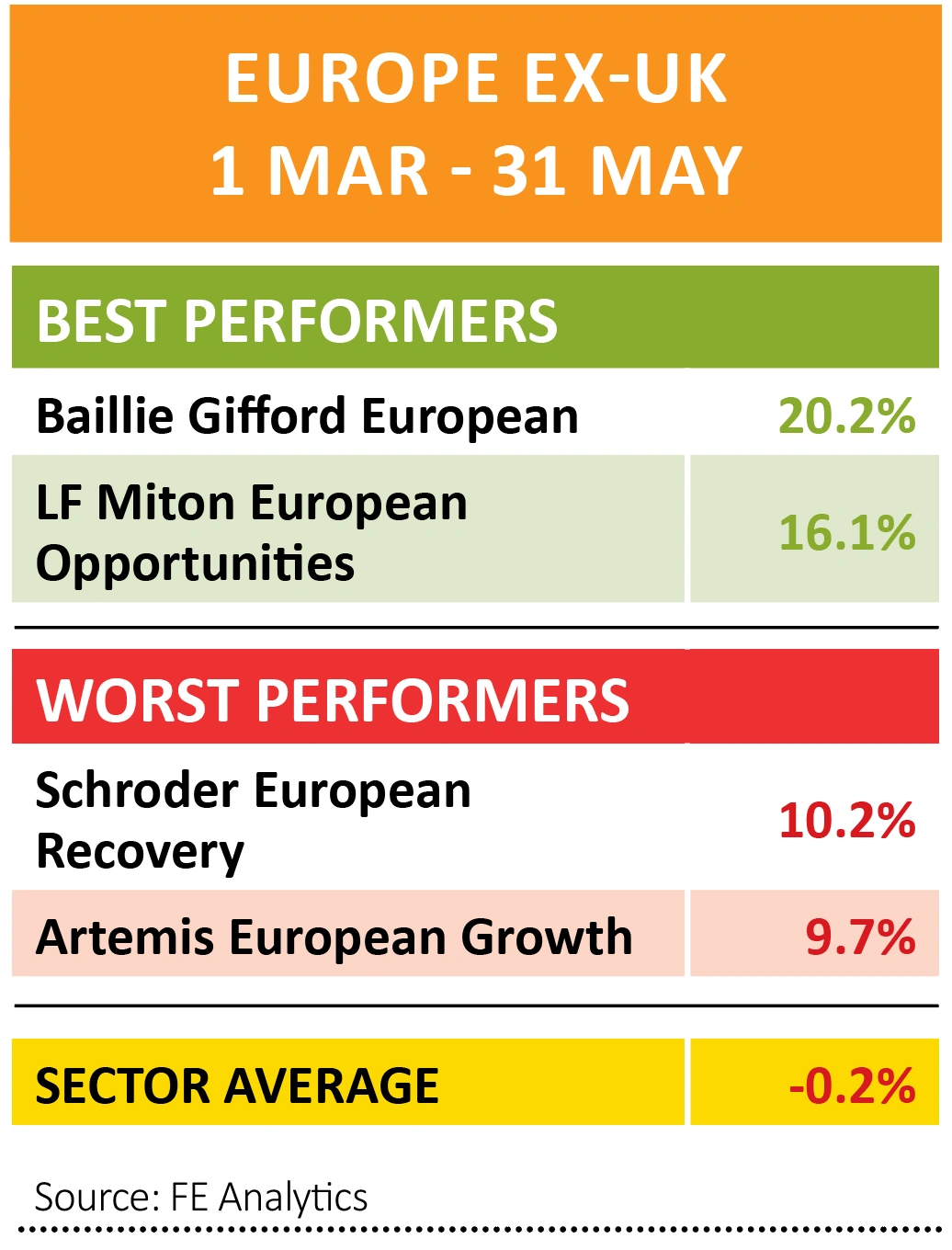

FINDING SUCCESS WITH EUROPEAN STOCKS

If you had a tracker fund or exchange-traded fund simply mirroring the European equities market during the sell-off, you’d have been hit hard. That’s according to Stephen Paice, manager of Baillie Gifford European (6058258), which returned 20.2% in the three months to 31 May, while the MSCI Europe ex-UK index fell 0.2% over the same period.

While Paice is at pains to point out that three months is nothing in the world of investing and investors should really have a five to 10 year minimum horizon, he revealed the Baillie Gifford fund’s weighting towards mid-cap tech stocks like German e-commerce platform Zalando and IT firm Bechtle, as well as Swedish online broker Avanza, have served the fund well in recent months.

The three stocks, all of which are in the fund’s top five holdings and make up 13.6% of the portfolio, took a hit in the sell-off but have since bounced back to go above pre-coronavirus levels.

Paice says: ‘We’re exposed to attractive, changing trends in the European economy, which are positioned for the transition to online and are primed to take market share from weaker competitors.

‘A lot of these companies in Europe tend to be mid-caps. If you look at the index, at the top end it’s full of banks, financial companies, industrials, a lot of companies that are stuck in the past.’

HITTING THE JACKPOT

As the coronavirus crisis started, many investors turned to absolute return funds, either to diversify their portfolio or to introduce a fund focused on more stable returns, with the aim of getting their investments recession-proof.

Returns in the sector have been anything but absolute in the three months to the end of May, with the average absolute return fund delivering -1.5% and the worst in the sector, iFunds Absolute Return Orange (B3Z19M3), returning -11.3%.

The one fund which has soared above the rest is Argonaut Absolute Return (B7FT1K7), which has returned 9.4% during the three-month period and year-to-date has rocketed 19.8%.

The fund tries to maintain zero correlation to the wider market and employs a long/short strategy in a variety of asset classes.

In the fund’s May factsheet, manager Barry Norris said: ‘Since the March market bottom, we have continued to take profits from previously successful shorts, selectively add cyclicality to the long book and increase our net exposure.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Premier Foods is in a sweet spot as it breathes new life into the business

- Lam Research is a best in class stock you need to own

- Buy Touchstone now as it gears up for a big increase in production

- Microsoft shares hit new all-time high as it sees little coronavirus impact

- Fresh pork-to-poultry supplier Cranswick continues to sizzle

- Polar Capital’s shares are up 10% since we said to buy a week ago