Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFresh pork-to-poultry supplier Cranswick continues to sizzle

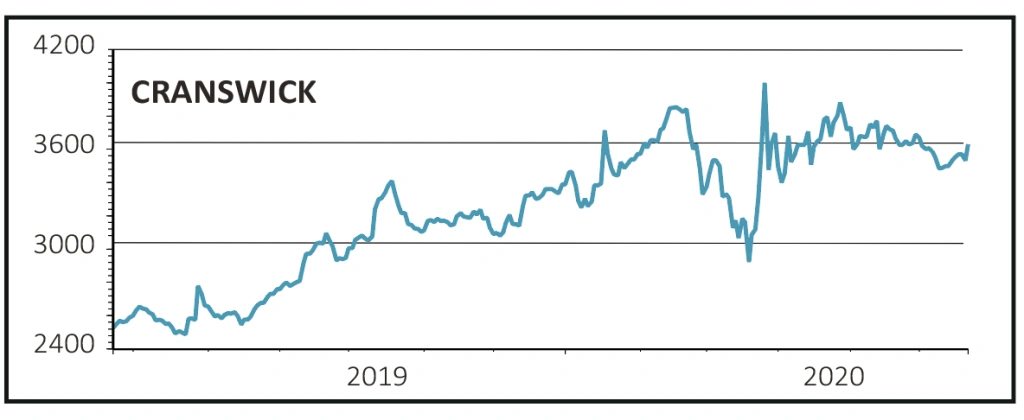

CRANSWICK (CWK) £37.68

Gain to date: 3.8%

Original entry point: Buy at £36.30 on 2 April 2020

We remain positive on quality food producer Cranswick (CWK) following better than expected full-year results on 23 June.

It is benefiting from two major tailwinds; lockdown is driving bumper demand for food consumed at home while African swine fever has destroyed pig herds in China and has presented a major export opportunity for the company.

For the year to 28 March, total sales rose 16% to £1.7 billion, leading to better than expected pre-tax profits of £102.3 million, up 11.2% and aided by the robust UK demand we’d anticipated. Total export revenue rose 92%, with Far East exports up 122%, as African swine fever outbreak boosted volumes and prices.

With a strong balance sheet and healthy liquidity, Cranswick also increased the final dividend by 9.8% to 43.7p for a total dividend of 60.4p, reflecting 30 years of unbroken dividend growth.

‘Whilst management talk of a “positive” start to the new year, with we believe strong growth coming from UK retail channels, enough uncertainty coming from Covid-19, China pork prices and Brexit remain for us to leave our prudently pitched full year 2021 forecasts unchanged for now,’ cautions Shore Capital.

SHARES SAYS: Cranswick is benefiting from two significant tailwinds and given its strong balance sheet and enviable long-run dividend growth record, we

remain buyers.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Premier Foods is in a sweet spot as it breathes new life into the business

- Lam Research is a best in class stock you need to own

- Buy Touchstone now as it gears up for a big increase in production

- Microsoft shares hit new all-time high as it sees little coronavirus impact

- Fresh pork-to-poultry supplier Cranswick continues to sizzle

- Polar Capital’s shares are up 10% since we said to buy a week ago