Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazinePubs, hotels and leisure stocks: should you keep your distance?

Last week saw the much-awaited reopening of ‘non-essential’ retailers, after 12 weeks of lockdown restrictions, with images of crowds milling around at retail parks and lengthy queues outside high-street stores.

Research group Springboard says that while consumers have started to return to shops, footfall in the first week of non-essential retail reopening in England was only half the level versus a year ago.

The focus now turns to the hospitality/leisure sector, which is reopening from 4 July. As with non-essential retail, there are considerable questions over how businesses will cope with the increased cost and inconvenience of enhanced hygiene and social distancing measures.

In this article we look at three sectors – pubs and restaurants, hotels, and ‘other’ hospitality and leisure stocks – and pick the firms which we think are the likely winners. We also identify one stock which we think investors would be best to avoid.

RECORD CONTRACTION

Not to put too fine a point on it, the Government needs the leisure sector to reopen to boost consumer spending. The UK economy shrank by over 10% in the three months to April, and by a staggering 20% in April alone – the first full month of lockdown – according to the Office for National Statistics (ONS).

April’s fall in gross domestic product (GDP) was the biggest the UK has ever seen, more than three times larger than March and almost 10 times larger than the steepest pre-Covid-19 fall. In April the economy was around 25% smaller than in February, according to the ONS.

‘Virtually all areas of the economy were hit, with pubs, education, health and car sales all giving the biggest contributions to this historic fall,’ it says.

Figures from trade body UK Hospitality put April’s fall in monthly turnover for the sector at 89% or £4.7 billion, which it says is almost a quarter of the loss in GDP. Over March and April combined, it believes the hospitality sector accounted for more like a third of the loss in UK GDP.

The sector employs 3.5 million people and generates a large amount of income for the Government, but industry insiders expect the number of pubs, bars and restaurants to shrink by at least 20% and potentially much more unless businesses are permitted to reopen soon.

The Government has another incentive to reopen the sector. As well as rebooting spending, the sooner businesses reopen the sooner it can start tapering the furlough scheme and other support packages which are estimated to already have cost over £20 billion.

According to data from HMRC, by the end of May accommodation and food service firms had furloughed 1.4 million jobs at a cost of £2.6 billion, not far behind retail and wholesale firms which had furloughed 1.6 million staff at a cost of £3.3 billion.

TOO MUCH CHOICE

Before the pandemic, consumer spending on ‘experiences’ was firmly in an upward trend while spending on ‘stuff’ was on a downward path.

As well as spending on cinemas, concerts and holidays, we were eating and drinking out with increasing frequency. This was partly driven by a surge in openings of casual dining and drinking venues such as gourmet burger establishments, gin emporia and other offerings.

This wave of investment inevitably led to poor business decision-making and over-capacity, especially in the restaurant sector. With too many chains chasing too few customers, the turkeys came home to roost for brands such as Byron, Café Rouge, Carluccio’s, Jamie’s Italian and Prezzo.

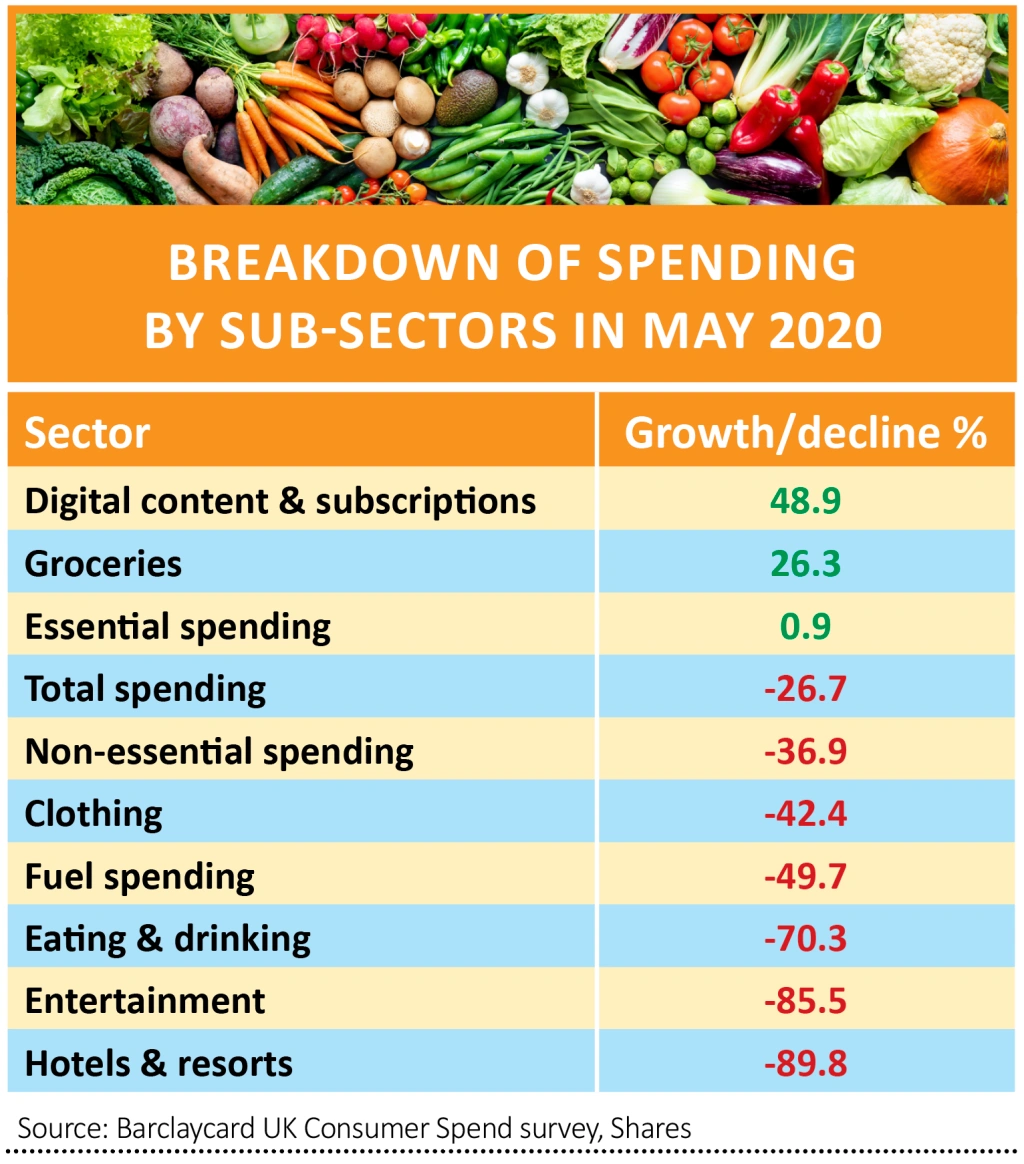

Now, thanks to lockdown, consumer spending on non-essentials has collapsed. According to the latest Barclaycard UK Consumer Spend survey, non-essential purchases fell 48% by value in April and 37% in May. The worst affected sector was eating and drinking out, which fell by 79% in April and 70% in May.

In contrast, spending on food and drink at greengrocers and off licences rose 42% last month, even more than the 25% rise in supermarket spending and second only to spending on digital content and subscriptions.

CHANGING TASTES

The big unknown is whether customers will want to visit pubs and restaurants, stay in hotels, or go to the cinema or bowling when the UK’s coronavirus ‘R’ or reproduction rate has tipped back over one in some regions and the death toll – the second-highest in the world after the US – continues to rise.

In a recent survey of shoppers by retail consultant Springboard, more than 30% of people said they were ‘nervous’ about shopping again compared to just 14% who were ‘excited’.

In the US, where the hospitality sector has been open for some time, 30% of people surveyed said they had been out to eat once in the last fortnight compared with 80% who would normally visit a bar or restaurant for a meal at least once every two weeks pre-Covid. The main reason for not going out was ‘not feeling safe’.

For many of us, the idea of mixing with people outside of our own close circle in an enclosed space like a pub, restaurant or cinema for an extended period may be a step too far given the pandemic is still raging.

In the same way that we have become used to shopping from home, we have got used to cooking at home and saving money, so while we may go to a pub or a restaurant for a ‘treat’, or go to the cinema or bowling, we probably won’t go as often as we did and we make the conscious decision not spend as much as would have previously.

In the short-term, getting hospitality/leisure staff back from furlough is also going to be a big effort as many individuals may not feel comfortable returning to work unless they are happy it is going to be a safe environment.

ONE METRE OR TWO?

For many in the hospitality business, survival comes down to the two-metre social distancing rule.

The UK’s Special Advisory Group for Emergencies recommends that people keep a minimum distance of two metres away from each other to halt the spread of coronavirus.

However, the World Health Organisation recommends a distance of ‘at least one metre’, advice which many countries including Denmark, France, Germany and the Netherlands have taken as their official policy.

As far as the hospitality sector is concerned, the general wisdom repeated by people such as Luke Johnson, founder of Pizza Express, and others, is that if customers have to distance by two metres more than two thirds of bars and restaurants will have to close, whereas at one metre more than two thirds stand a chance of surviving.

The UK Government says the 2 metre rule will be relaxed to ‘1 metre plus’ from 4 July.

WINING AND DINING

While high-end restaurants and bars may still attract those for whom money is no object, mid-priced casual-dining venues and food-led pubs will have to be more competitive on price if they are going to attract customers.

With 9 million people furloughed in total, and the number of job centre claimants reaching 2.8 million since the start of lockdown – an increase of 126%, the most in 100 years – value for money will be key when it comes to going out.

The problem then becomes one of scale. If food-led pubs, bars and restaurants have to lower their prices, how do they get enough customers in to cover their costs, which are no longer being met by the Government once they reopen and which will have risen significantly due to enhanced hygiene regimes?

HOTELS AND MOTELS

The hotel industry may be on a better footing than pubs, bars and restaurants as it is much easier to separate guests from each other and from staff.

For example, adding a dining table and chairs to each room means that guests can order room service, with hotel staff leaving meals and drinks outside the door much as an Uber or Deliveroo driver does now.

Also, there isn’t the need to repeatedly clean down surfaces as there is in pubs or restaurants, and guests can check out by simply leaving their keys in a designated place and receiving their bill via email.

The sector also has the benefit of a unique tailwind in that, with the Government enforcing a two week quarantine on anyone re-entering the country after a holiday abroad, more people are likely to choose to travel within the UK and take a ‘staycation’.

SCENARIO PLANNING

Many hospitality firms have taken the view that a worst-case scenario would see their businesses operating below maximum capacity for at least a year. They have taken action to reduce monthly cash burn and increase available liquidity to meet that challenge.

The British Beer & Pub Association says pub and brewery businesses are burning through £100 million every month in cash while they remain closed.

While many hope to reopen in July, even optimists such as JD Wetherspoon’s (JDW) chairman Tim Martin admit the move back to normality will likely be gradual.

Survival is paramount, but the stronger firms also have one eye on making sure they exit lockdown with enough firepower to take advantage of what is likely to be a hollowed-out hospitality sector.

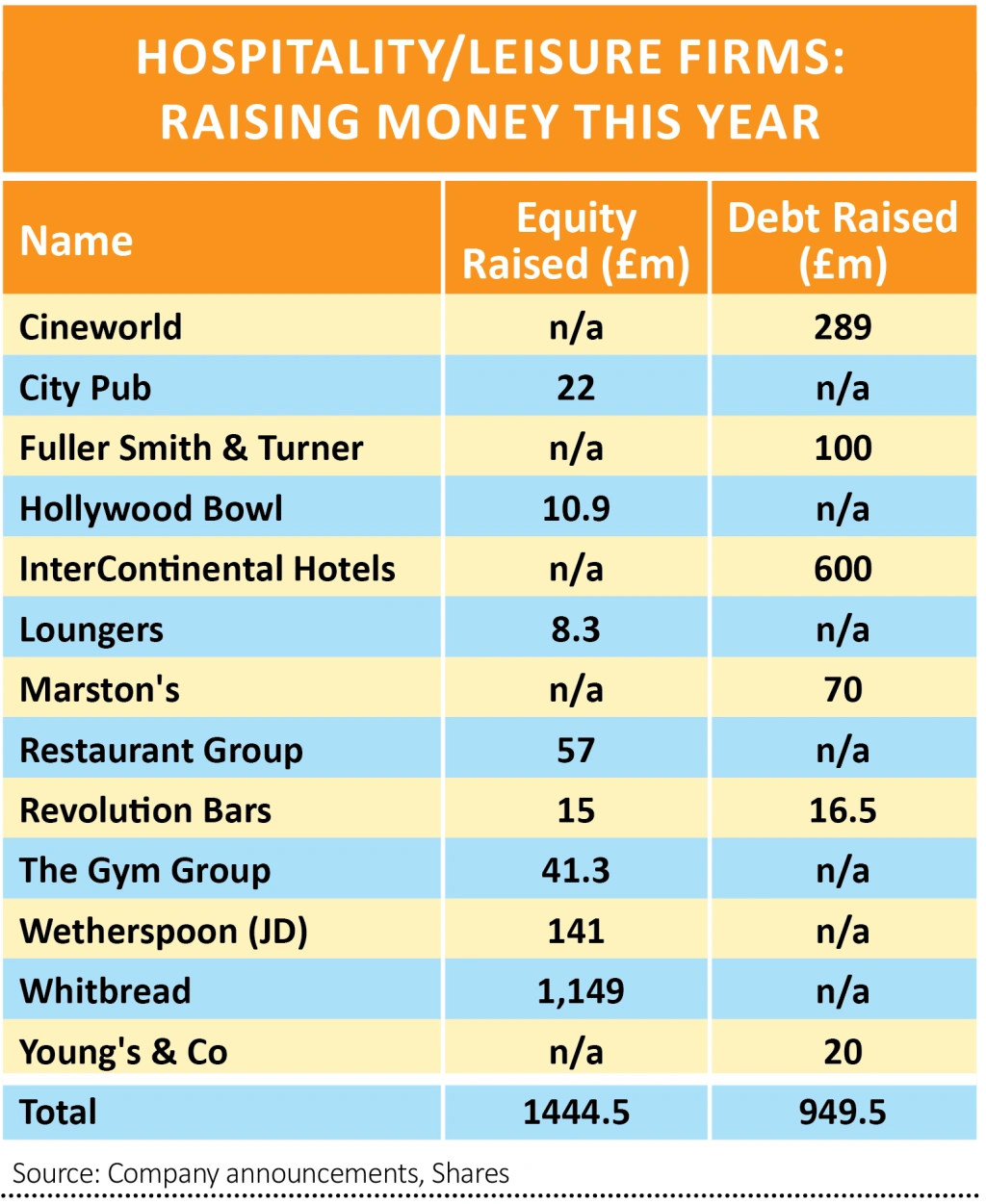

In total, the companies in the table have issued around £1.4 billion worth of new shares while debt facilities have increased by roughly £950 million.

Companies with significant property assets such as Young’s (YNGA:AIM) and Fuller, Smith & Turner (FSTA) have been able to extend their existing banking facilities which are secured on their assets.

Pub and brewing group Marston’s (MARS) found a more creative way of raising cash, merging its brewing assets into a joint venture with Carlsberg’s UK division in exchange for £273 million in cash and a 40% stake in the new company, Carlsberg Marston’s Brewing.

Surprisingly, given its highly geared balance sheet, cinema group Cineworld (CINE) didn’t try to raise fresh equity. Instead it raised $360 million of additional debt while its lenders waived leverage covenant testing for June 2020 and relaxed the terms of the December test to an eye-popping 9.5 times net debt to EBITDA (earnings before interest, tax, depreciation and amortisation) from 5.5 times.

Other firms have tapped shareholders for cash, with some needing to offer big discounts to attract funds while others were able to sell new shares at a premium.

Revolution Bars (RBG) had to offer shares at a 34% discount to raise around £15 million, while all-day bar restaurant group Loungers (LGRS:AIM) asked shareholders for £8.3 million and was able to raise the cash at a 16% premium.

WINNERS & LOSERS

Shares has selected four hospitality/leisure stocks which we think are well placed to survive, if not thrive, once lockdown measures are relaxed.

Our selections are based on the companies’ financial strength, their ability to manage social distancing along with the increased costs of enhanced hygiene requirements, and market position.

We have also identified one stock which we think investors should avoid for the time being given its high level of financial and operational gearing and the challenges facing its business.

FOUR STOCKS TO BUY

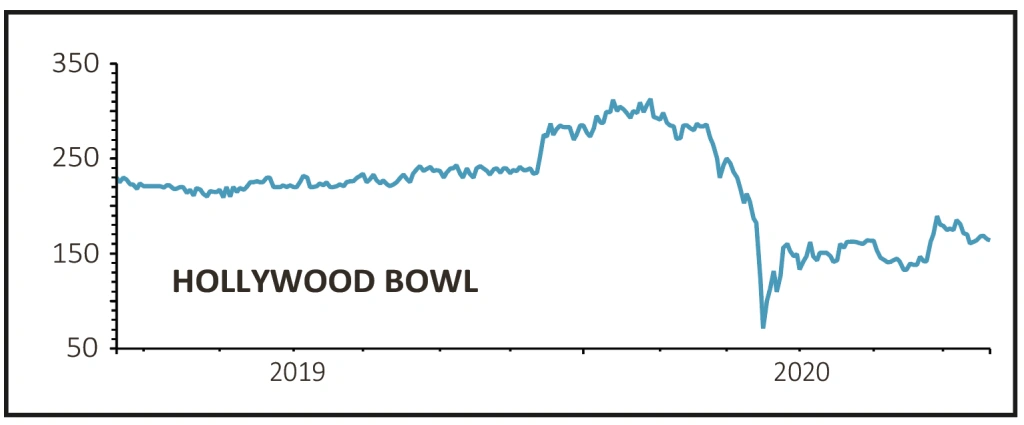

Hollywood Bowl (BOWL)

Price: 165p – Market Cap: £265 million

We believe for families seeking a value for money experience in a relatively safe environment, tenpin bowling operator Hollywood Bowl (BOWL) will continue to be a popular destination.

The company’s large sites, typically over 28,000 square feet, mean it is relatively easy for it to operate profitably while respecting social distancing measures.

Sites have been reconfigured with alternate lane usage and more space between bar and dining tables as well as amusement machines to help customers feel that they are in a safe environment.

The food and drink menus have been reduced to simplify the delivery of the food service and protect customers and staff.

Finally, the company believes it has enough liquidity to operate with only 20% of normal revenues for the next year.

Disappointingly the Government said bowling alleys wouldn’t reopen on 4 July, meaning Hollywood Bowl will lag pubs and hotels with a revival in earnings. However, we do believe it won’t be long before it does get the green light to open its doors again.

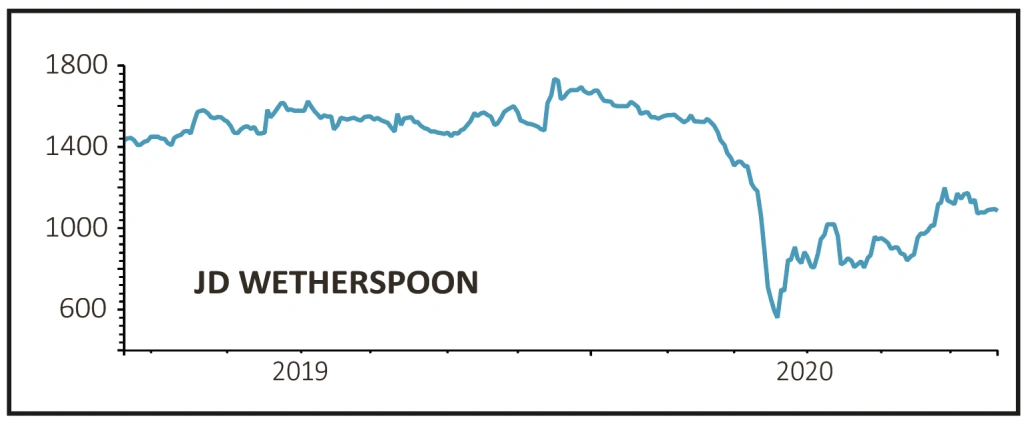

JD Wetherspoon (JDW) BUY

Price: £10.88 – Market Cap: £1.3 billion

We think JD Wetherspoon (JDW) will be another winner post-pandemic as it has several advantages over other pub companies.

First, its well-understood value for money proposition should be attractive to cash-strapped drinkers and diners looking to treat themselves.

Also, it operates from large venues meaning it can serve more customers while operating within social distancing rules.

Many of its venues have access to a beer garden which will not only allow it to operate at higher capacity but also increase the perception of safety as the likelihood of virus transmission is lower in outdoor spaces.

Its use of technology could also be a positive factor with customers using an app on their phone to order food and drink from their tables and away from the bar.

Finally, even if business remains slower than usual on reopening, the company believes it can remain cash flow neutral even with a 50% fall in like-for-like revenues.

Loungers (LGRS: AIM) BUY

Price: 130p – Market Cap: £133 million

Hybrid café/bar operator Loungers (LGRS:AIM) has a unique business model which gives it several advantages.

Unlike bars and restaurants where customers tend to conjugate at set times of the day, Loungers’ traffic is spread more evenly throughout the day.

With more people able to work from home, the brand’s strong ‘community’ identity is a favourable factor when customers are looking for somewhere to visit.

Loungers has been very active across social media, engaging with its loyal customer base. In a company survey only 2% of 6,000 respondents said they wouldn’t feel comfortable resuming their normal visits, an encouraging sign for demand after reopening.

Layouts have been revised and surplus furniture stored to accommodate social distancing. Should the two-metre rule remain in place, management has identified a handful of sites which would have to remain closed.

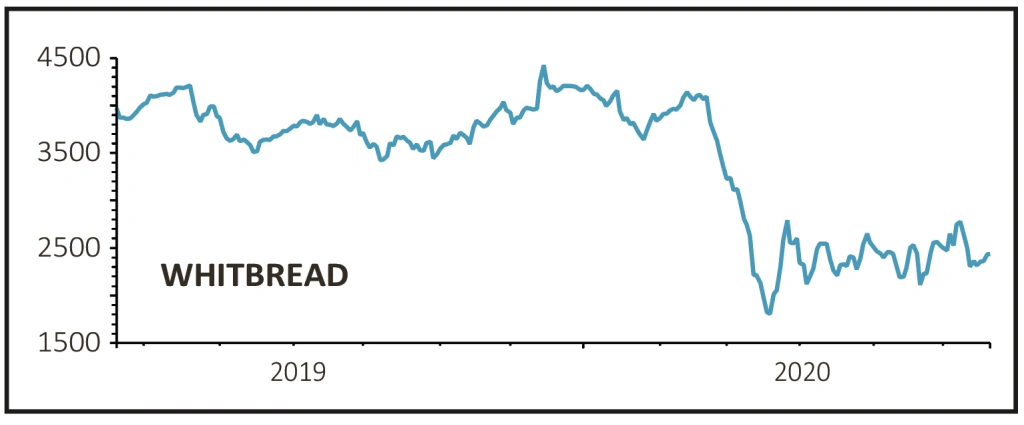

Whitbread (WTB)

Price: £24.38 – Market Cap: £4.8 billion

As the UK’s largest hotel operator, with over 1,200 Premier Inns serving more than 5 million customers a month pre-Covid, Whitbread (WTB) is in a prime position to benefit from the easing of lockdown restrictions.

Its trusted value proposition and the quality of the offering – its hotels have the same standards and décor from Land’s End to John O’Groats – are strong drivers when people are choosing where to stay.

Strict social distancing and enhanced hygiene standards have been rigorously employed throughout the estate, and the firm has ‘done the right thing’ during the crisis by keeping 39 of its hotels near hospitals open for use by NHS staff and other frontline key workers.

The firm recently raised £1bn of equity financing putting it in an extremely strong position to continue investing in the business as we come out of the crisis.

ONE TO AVOID

Cineworld (CINE)

Price: 76.9p – Market Cap: £1.1 billion

Cineworld intends to reopen in the UK on 10 July having updated its booking system and schedules in order to limit queues and avoid crowds in the lobbies, while enhanced sanitation measures have been implemented.

However, the configuration of cinemas and theatre halls presents significant problems for adhering to social distancing measures, and we question whether people will feel comfortable sitting indoors close to strangers for hours at a time.

Consumers’ shift to streaming content during lockdown may have permanently altered their preferences for watching films, while pressure is also coming from the supply side with Universal Studios having streamed new films directly to homes.

Furthermore, cinema operators like Cineworld face a big problem in that so many potential blockbuster films have had their release delayed until late 2020 or pushed back to summer 2021. That could leave cinemas reliant on old titles to get people through the doors this year.

In normal times, the success of a mainstream cinema chain is heavily dependent on the film slate and there is nothing Cineworld can do to overcome the current dearth of new releases for the coming months.

Cineworld’s monthly cash burn during lockdown has been reduced to £1.2 million. Pulling out of the Cineplex acquisition may give it a handful of extra months’ liquidity according to one broker, but the firm’s heavily geared balance sheet remains a major worry. This is definitely the wrong time to be owning its shares.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Premier Foods is in a sweet spot as it breathes new life into the business

- Lam Research is a best in class stock you need to own

- Buy Touchstone now as it gears up for a big increase in production

- Microsoft shares hit new all-time high as it sees little coronavirus impact

- Fresh pork-to-poultry supplier Cranswick continues to sizzle

- Polar Capital’s shares are up 10% since we said to buy a week ago