Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineMore reasons to be positive on ITV as viewing figures rise

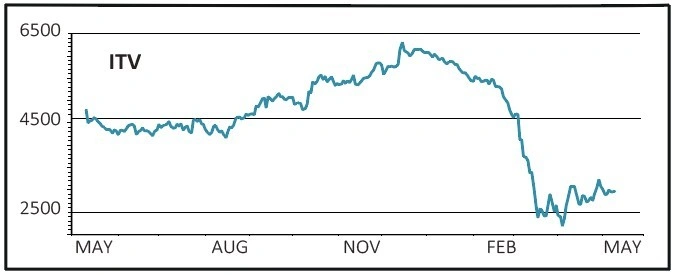

ITV (ITV) 72.6p

Loss to date: 4.5%

Original entry point: Buy at 76p, 30 April 2020.

Free-to-air broadcaster ITV (ITV) may have lost some of the momentum gained in the wake of a first quarter trading update (6 May) but we continue to see reasons to be encouraged by the announcement.

The coronavirus pandemic both hurt demand for advertising in the first quarter of the year and continued into April with advertising down 42% for the month. Its ITV Studios production business is effectively on pause.

For the three months to 31 March, total external revenue was down 7% at £694m year-on-year, with ITV Studios’ revenue down 11% at £342m, broadcast revenue up 2% at £500m and ITV total advertising up 2% as originally guided, with online revenues up 26%.

ITV total viewing was up 2% with ‘very strong’ growth in online viewing up 75%, simulcast viewing up 112% and reach up 40% on the ITV Hub.

Its main channel’s share of viewing hit 17.9%, its best quarter since 2009, and the company flagged growth for its BritBox venture with the BBC in the form of free trial starts and subscriptions.

Shore Capital analyst Roddy Davidson says: ‘We believe that ITV should be a significant beneficiary of a recovery in advertising spend as Covid-19 lockdown measures are relaxed.’

SHARES SAYS: ITV remains an attractive way to play a rebound in advertising spend.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Exchange-Traded Funds

Feature

First-time Investor

Great Ideas

- Genus remains well positioned for further growth

- Civitas targets above-inflation dividend growth

- More reasons to be positive on ITV as viewing figures rise

- Buy this ETF to profit from the healthcare revolution

- Boris’ return to work by car message could boost shares in Motorpoint

- Ocado shares hit another new all-time high on surging grocery sales